Presentation on the topic of personal property tax. Presentation on the topic “Local taxes How tax is calculated when inheriting real estate

To view a presentation with pictures, design, and slides, download its file and open it in PowerPoint on your computer.

Text content of presentation slides: Topic: " Local taxes»Savina I.A. Lecturer at the Tomsk College of Railway Transport - a branch of SGUPS payment in the territories of the respective municipalities 2 Local taxes3 Local taxesLocal taxes apply throughout the territory Russian Federation. Local taxes include: land tax; property tax individuals.4 Land tax5 Taxpayers6 Organizations and individuals owning land plots recognized as an object of taxation: on the right of ownership; on the right of permanent (perpetual) use; on the right of lifetime inheritable possession. Evidence of registered rights is an entry in the Unified State Register of Rights to Real Estate and Transactions with It (EGRP). This provision is enshrined in Art. 2 of the Federal Law of July 21, 1997 No. 122-FZ "On state registration of rights to real estate and transactions with it." The entry made in the register is certified by a certificate of state registration of rights. Organizations and individuals are not recognized as taxpayers in relation to land plots: located by them on the right of gratuitous fixed-term use; transferred to them under a lease agreement. Object of taxationLand plots located within the boundaries of the municipality on whose territory the tax has been introduced. The land plot must be formed and put on the cadastral register. Objects of taxation are land plots acquired in the ownership of citizens and legal entities, including land plots that are in common fractional ownership; land plots provided for permanent (unlimited) use by the state and municipal institutions, state-owned enterprises, centers of historical heritage of the presidents of the Russian Federation who have ceased to exercise their powers, as well as bodies state power and local self-government bodies; land plots owned by the right of lifetime inheritable possession of individuals. Not recognized as an object of taxation Tax base cadastral value land plots recognized as an object of taxation as of January 1 of the year that is tax period.In respect of shares in the right of common ownership of a land plot, in respect of which different persons are recognized as taxpayers or different tax rates are established, the tax base is determined separately for each share. The tax base common property In relation to land plots in common shared ownership, the tax base is determined for each of the taxpayers who are the owners of this land plot in proportion to its share in the common shared ownership. With regard to land plots located in the common joint ownership, the tax base is determined for each of the taxpayers who are the owners of this land plot, in equal shares. Definition tax base The tax base is determined on the basis of information from the state real estate cadastre. Legal entities determine the tax base independently. For individuals, the tax authorities determine the tax base. Reducing the tax baseIn accordance with paragraph 5 of Article 391 tax code Russian Federation, the tax base is reduced by 10,000 rubles for the following categories of individuals: - Heroes of the Soviet Union, Heroes of the Russian Federation, full holders of the Order of Glory; - disabled people of groups I - II; disabled since childhood; - veterans and invalids of the Great Patriotic War and military operations; - individuals entitled to receive social support in connection with exposure to radiation; those who took a direct part in the testing of nuclear and thermonuclear weapons, the liquidation of accidents at nuclear installations at weapons and military facilities; who received or suffered radiation sickness as a result of work related to any kind of nuclear installations, including nuclear weapons and space technology. Tax and reporting periods The tax period is a calendar year. Reporting periods established only for legal entities and individual entrepreneurs- first quarter, second quarter and third quarter of the calendar year. Tax rates Tax rates are established by regulatory legal acts of the representative bodies of municipalities and cannot exceed the values determined by Art. 394 of the Tax Code of the Russian Federation Tax rates highways general use; religious organizations; all-Russian public organizations of the disabled; organizations authorized capital which consists entirely of the contributions of the indicated all-Russian public organizations of the disabled; Exempted from payment are individuals belonging to the indigenous peoples of the North, Siberia and Far East Russian Federation, as well as communities of such peoples; organizations of folk art crafts; organizations - residents of the special economic zone; organizations recognized as management companies in accordance with federal law About the Skolkovo Innovation Center. Tax calculation procedure The tax is calculated as the corresponding tax rate percentage of the tax base according to the formula: Calculation of advance payments The amount of advance payments after the first, second and third quarters is determined by the formula: Calculation for an incomplete tax period The procedure and terms of payment for legal entities pay advance payments in equal shares, in the following terms: for the first quarter - not later than May 5 for the second quarter - no later than August 5 for the third quarter - no later than November 05 Upon expiration of the tax period, the tax is paid no later than February 1 of the year following the expired tax period. The procedure and terms of payment for individuals The tax is paid before November 15 of the year following the expired tax period on the basis of a notice issued by tax authorities. A tax notice may be sent for no more than three tax periods preceding the calendar year in which it was sent. Personal property tax Taxpayers Object of taxation Tax base Tax rates Tax benefitsHeroes of the Soviet Union and Heroes of the Russian Federation, as well as persons awarded the Order of Glory of three degrees; disabled people of groups I and II, disabled from childhood; participants in the Civil and Great Patriotic Wars, other military operations to protect the USSR; persons of the civilian staff of the Soviet Army, Navy, internal affairs bodies and state security who held full-time positions in military units, headquarters and institutions that were part of the active army during the Great Patriotic War; Tax benefits persons eligible to receive social support in connection with exposure to radiation due to the disaster at the Chernobyl nuclear power plant, the accident at the Mayak production association and the discharge of radioactive waste into the Techa River; military personnel, as well as citizens discharged from military service upon reaching the age limit for military service, for health reasons or in connection with organizational and staff measures, having a total duration of military service of 20 years or more; Tax benefits Members of the families of military personnel who have lost their breadwinner; pensioners receiving pensions assigned in the manner prescribed by pension legislation; citizens who were discharged from military service or called up for military training, who performed international duty in Afghanistan and other countries in which hostilities were fought; parents and spouses of military personnel and civil servants who died in the line of duty; other categories of individuals. Calculation and payment procedureThe tax is calculated by the tax authorities on the basis of inventory value data as of January 01 of each year. For new buildings, premises and structures, tax is paid from the beginning of the year following their erection or acquisition. Procedure for Calculation and Payment For a structure, premises and structures that have been inherited, tax is levied from the heirs from the moment the inheritance is opened. Terms of payment and recalculation Tax payment is made no later than November 1 of the year following the year for which the tax was calculated. Tax notices on the payment of tax on property of individuals are handed over to payers by the tax authorities no later than 30 days before the due date of payment. Recalculation of the amount of tax in respect of persons who are obliged to pay tax on the basis of a tax notice is allowed no more than three years preceding the calendar year of sending tax notice in connection with the recalculation of the amount of tax.

Attached files

slide 1

slide 2

Who is recognized as a payer of personal property tax? Individual property tax payers are citizens who own residential houses, apartments, dachas, garages and other buildings, premises and structures. At the same time, if the property is in the common shared ownership of several individuals, each of these individuals is recognized as a taxpayer in relation to this property in proportion to its share in this property.

Who is recognized as a payer of personal property tax? Individual property tax payers are citizens who own residential houses, apartments, dachas, garages and other buildings, premises and structures. At the same time, if the property is in the common shared ownership of several individuals, each of these individuals is recognized as a taxpayer in relation to this property in proportion to its share in this property.

slide 3

Object of taxation the following types property: -residential houses -apartments -dachas -garages -other buildings, premises and structures.

Object of taxation the following types property: -residential houses -apartments -dachas -garages -other buildings, premises and structures.

slide 4

Tax rates Since the tax on the property of individuals is a local tax, tax rates for buildings, premises, structures are established by regulatory legal acts of representative bodies of local self-government. Tax rates are set depending on the total inventory value of the property.

Tax rates Since the tax on the property of individuals is a local tax, tax rates for buildings, premises, structures are established by regulatory legal acts of representative bodies of local self-government. Tax rates are set depending on the total inventory value of the property.

slide 5

Tax Rates Representative bodies of local self-government may determine the differentiation of rates in established limits depending on: 1) total inventory value; 2) type of use; 3) other criteria. Rates can be set depending on whether the premises are residential or non-residential, used for household or commercial needs, brick, block or built of wood, etc. Taxes are credited to local budget at the location of the object of taxation.

Tax Rates Representative bodies of local self-government may determine the differentiation of rates in established limits depending on: 1) total inventory value; 2) type of use; 3) other criteria. Rates can be set depending on whether the premises are residential or non-residential, used for household or commercial needs, brick, block or built of wood, etc. Taxes are credited to local budget at the location of the object of taxation.

slide 6

Tax base 1. The tax base for a tax is defined as inventory value objects real estate recognized as an object of taxation in accordance with Article 388 of this Code. 2. The methodology for determining the inventory value of real estate objects is approved in the manner determined by the Government of the Russian Federation.

Tax base 1. The tax base for a tax is defined as inventory value objects real estate recognized as an object of taxation in accordance with Article 388 of this Code. 2. The methodology for determining the inventory value of real estate objects is approved in the manner determined by the Government of the Russian Federation.

Slide 7

Tax benefits The following categories of citizens are exempted from paying property tax on individuals: 1) Heroes of the Soviet Union and Heroes of the Russian Federation, as well as persons awarded the Order of Glory of 3 degrees 2) Disabled people of groups 1 and 2, disabled since childhood 3) participants in the civil and the Great Patriotic War, other military operations. 4) civilians of the Soviet Army, Navy, internal affairs and state security agencies, who held full-time positions in military units, headquarters and institutions that were part of the active army during the Great Patriotic War. 5) citizens exposed to radiation as a result of the disaster at the Chernobyl nuclear power plant 7) members of the families of servicemen who have lost their breadwinner.

Tax benefits The following categories of citizens are exempted from paying property tax on individuals: 1) Heroes of the Soviet Union and Heroes of the Russian Federation, as well as persons awarded the Order of Glory of 3 degrees 2) Disabled people of groups 1 and 2, disabled since childhood 3) participants in the civil and the Great Patriotic War, other military operations. 4) civilians of the Soviet Army, Navy, internal affairs and state security agencies, who held full-time positions in military units, headquarters and institutions that were part of the active army during the Great Patriotic War. 5) citizens exposed to radiation as a result of the disaster at the Chernobyl nuclear power plant 7) members of the families of servicemen who have lost their breadwinner.

Slide 8

Are minor children subject to personal property tax? Yes, they are. Property tax for their minor child must be paid by his parents, adoptive parents or guardians, since in accordance with clause 2 of Article 27 of the Tax Code of the Russian Federation, his legal representatives bear property responsibility for transactions of a minor.

Are minor children subject to personal property tax? Yes, they are. Property tax for their minor child must be paid by his parents, adoptive parents or guardians, since in accordance with clause 2 of Article 27 of the Tax Code of the Russian Federation, his legal representatives bear property responsibility for transactions of a minor.

Slide 9

The procedure for calculating taxes on property of individuals The tax is calculated by the tax authority at the location of the objects of taxation. In the case when an individual does not live at the location of the property recognized as an object of taxation, tax notice for the payment of the calculated tax is sent to the taxpayer by registered mail at the address of his place of residence. The tax is calculated on the basis of data on their inventory value as of January 1 of each year.

The procedure for calculating taxes on property of individuals The tax is calculated by the tax authority at the location of the objects of taxation. In the case when an individual does not live at the location of the property recognized as an object of taxation, tax notice for the payment of the calculated tax is sent to the taxpayer by registered mail at the address of his place of residence. The tax is calculated on the basis of data on their inventory value as of January 1 of each year.

PRESENTATION ON THE TOPIC: TAX ON PROPERTY OF INDIVIDUALS Complied with Art. group 22 PS -305: Pasynkova Yu. V. Checked by: Belova I. A.

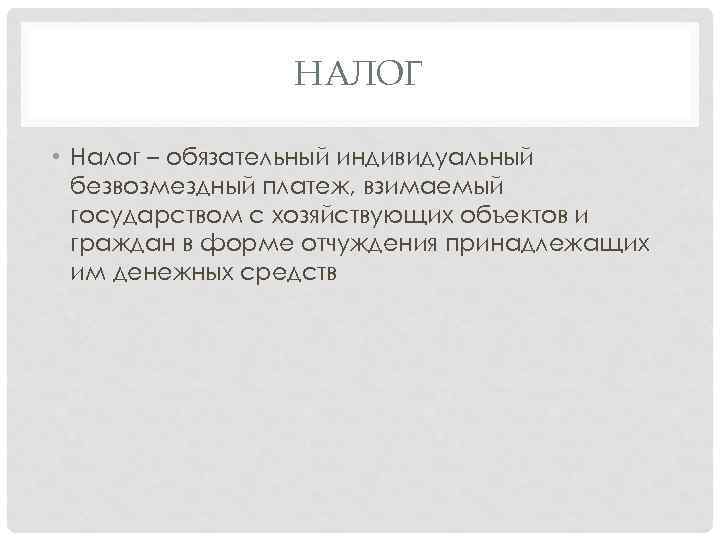

TAX Tax is a mandatory individual gratuitous payment levied by the state from economic objects and citizens in the form of alienation of their property. Money

TAX Tax is a mandatory individual gratuitous payment levied by the state from economic objects and citizens in the form of alienation of their property. Money

If the property recognized as an object of taxation is in the common joint ownership of several individuals, they bear equal responsibility for the execution tax liability. In this case, the payer of the tax may be one of these persons, determined by agreement between them.

If the property recognized as an object of taxation is in the common joint ownership of several individuals, they bear equal responsibility for the execution tax liability. In this case, the payer of the tax may be one of these persons, determined by agreement between them.

The following types of property are recognized as objects of taxation: a residential house, apartment, room, cottage, garage, other building, premises and structure, a share in the right of common ownership in the above types of property, which are owned by individuals.

The following types of property are recognized as objects of taxation: a residential house, apartment, room, cottage, garage, other building, premises and structure, a share in the right of common ownership in the above types of property, which are owned by individuals.

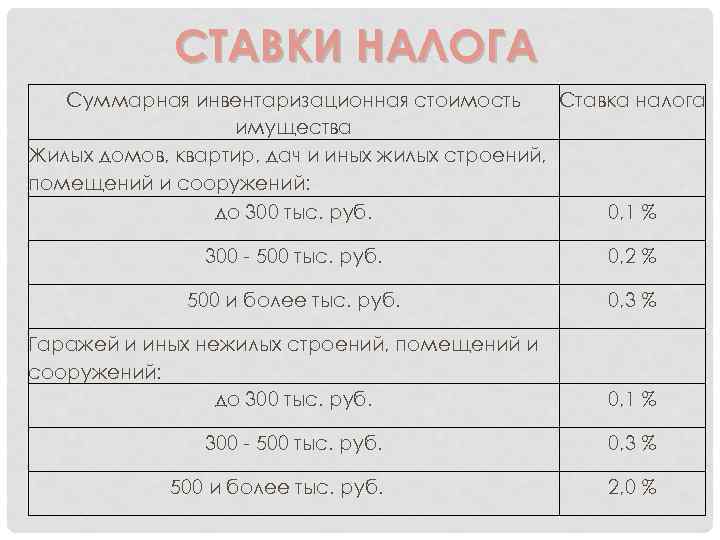

TAX RATES Total inventory value Property tax rate Residential buildings, apartments, summer cottages and other residential buildings, premises and structures: up to 300 thousand rubles. 0.1% 300 - 500 thousand rubles. 0.2% 500 and more thousand rubles. 0.3% Garages and other non-residential buildings, premises and structures: up to 300 thousand rubles. 0.1% 300 - 500 thousand rubles. 0.3% 500 and more thousand rubles. twenty %

TAX RATES Total inventory value Property tax rate Residential buildings, apartments, summer cottages and other residential buildings, premises and structures: up to 300 thousand rubles. 0.1% 300 - 500 thousand rubles. 0.2% 500 and more thousand rubles. 0.3% Garages and other non-residential buildings, premises and structures: up to 300 thousand rubles. 0.1% 300 - 500 thousand rubles. 0.3% 500 and more thousand rubles. twenty %

TAX RATES Residential houses, apartments, dachas and other residential buildings, premises and structures: q up to 300 thousand rubles. 0.1% q 300 -500 t. 0.2% q 500 t. And more than 0.3% Garages and other non-residential buildings, premises and structures: q up to 300 thousand rubles. q 300 -500 t. q 500 t. And more 0.1% 0.3% 2.0%

TAX RATES Residential houses, apartments, dachas and other residential buildings, premises and structures: q up to 300 thousand rubles. 0.1% q 300 -500 t. 0.2% q 500 t. And more than 0.3% Garages and other non-residential buildings, premises and structures: q up to 300 thousand rubles. q 300 -500 t. q 500 t. And more 0.1% 0.3% 2.0%

EXPLANATION Each municipality has its own tax rates. Municipalities are given the right to differentiate rates in established by law limits depending on the total inventory value, type of use and other criteria. On the basis of paragraph 2 of Article 5 of the Law for buildings, premises and structures that are in common shared ownership of several individuals, the tax is paid by each owner in proportion to his share in these buildings, premises and structures. The inventory value of a share in the right of common shared ownership is determined as the product of the inventory value of the property and the corresponding share.

EXPLANATION Each municipality has its own tax rates. Municipalities are given the right to differentiate rates in established by law limits depending on the total inventory value, type of use and other criteria. On the basis of paragraph 2 of Article 5 of the Law for buildings, premises and structures that are in common shared ownership of several individuals, the tax is paid by each owner in proportion to his share in these buildings, premises and structures. The inventory value of a share in the right of common shared ownership is determined as the product of the inventory value of the property and the corresponding share.

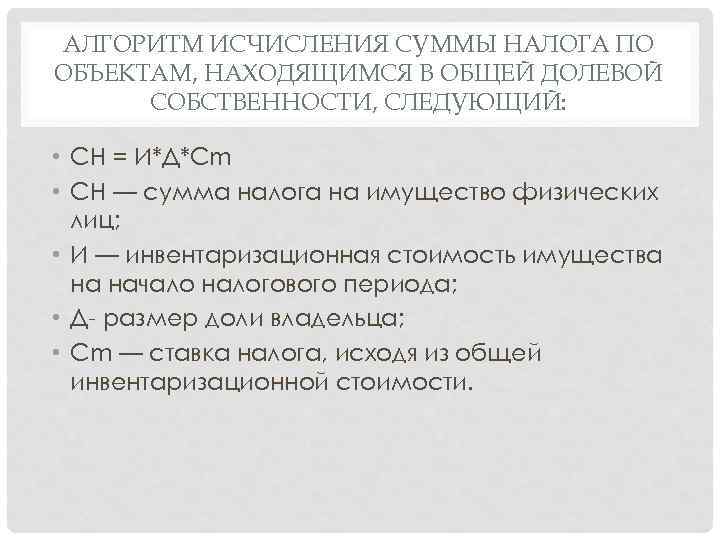

THE ALGORITHM FOR CALCULATION OF THE AMOUNT OF TAX FOR OBJECTS IN COMMON SHARED OWNERSHIP, THE FOLLOWING: SN = I*D*Cm SN - the amount of tax on the property of individuals; I - the inventory value of the property at the beginning of the tax period; D - the size of the share of the owner; Cm - tax rate based on the total inventory value.

THE ALGORITHM FOR CALCULATION OF THE AMOUNT OF TAX FOR OBJECTS IN COMMON SHARED OWNERSHIP, THE FOLLOWING: SN = I*D*Cm SN - the amount of tax on the property of individuals; I - the inventory value of the property at the beginning of the tax period; D - the size of the share of the owner; Cm - tax rate based on the total inventory value.

THE ALGORITHM FOR CALCULATION OF THE AMOUNT OF TAX FOR OBJECTS IN COMMON JOINT OWNERSHIP, THE FOLLOWING: SN = I/K*Cm SN - the amount of tax on the property of individuals; I - the inventory value of the property at the beginning of the tax period; K - the number of owners; Cm - tax rate based on the total inventory value.

THE ALGORITHM FOR CALCULATION OF THE AMOUNT OF TAX FOR OBJECTS IN COMMON JOINT OWNERSHIP, THE FOLLOWING: SN = I/K*Cm SN - the amount of tax on the property of individuals; I - the inventory value of the property at the beginning of the tax period; K - the number of owners; Cm - tax rate based on the total inventory value.

PRIVILEGES. EXEMPTIONED FROM PAYING TAX: Heroes of the Soviet Union and Heroes of the Russian Federation, participants in the Civil and Great Patriotic Wars, other military operations to defend the USSR; persons exposed to radiation as a result of the disaster at the Chernobyl nuclear power plant and the accident in 1957 at the Mayak production association; military personnel, as well as citizens dismissed from military service upon reaching the age limit for military service, for health reasons or in connection with organizational and staff measures, having a total duration of military service of 20 years or more; persons who were directly involved in the special risk units in the testing of nuclear and thermonuclear weapons, the elimination of accidents of nuclear installations at weapons and military facilities; family members of servicemen who have lost their breadwinner; pensioners receiving Russian pensions; citizens discharged from military service or called up for military training, performing international duty in Afghanistan and other countries in which hostilities were fought; parents and spouses of military and civil servants who died in the line of duty.

PRIVILEGES. EXEMPTIONED FROM PAYING TAX: Heroes of the Soviet Union and Heroes of the Russian Federation, participants in the Civil and Great Patriotic Wars, other military operations to defend the USSR; persons exposed to radiation as a result of the disaster at the Chernobyl nuclear power plant and the accident in 1957 at the Mayak production association; military personnel, as well as citizens dismissed from military service upon reaching the age limit for military service, for health reasons or in connection with organizational and staff measures, having a total duration of military service of 20 years or more; persons who were directly involved in the special risk units in the testing of nuclear and thermonuclear weapons, the elimination of accidents of nuclear installations at weapons and military facilities; family members of servicemen who have lost their breadwinner; pensioners receiving Russian pensions; citizens discharged from military service or called up for military training, performing international duty in Afghanistan and other countries in which hostilities were fought; parents and spouses of military and civil servants who died in the line of duty.

THERE ARE BENEFITS PROVIDED BASED ON THE TYPE OF PROPERTY. from specially equipped structures, buildings, premises (including housing) owned by cultural figures, artists and craftsmen on the right of ownership and used exclusively as creative workshops, ateliers, studios, as well as from living space used to organize non-state museums open to the public , galleries, libraries and other cultural organizations - for the period of their use; from located on plots in horticultural and country non-profit associations of citizens of a residential building with a living area of up to 50 square meters. m. and outbuildings and facilities with a total area of up to 50 sq. m.

THERE ARE BENEFITS PROVIDED BASED ON THE TYPE OF PROPERTY. from specially equipped structures, buildings, premises (including housing) owned by cultural figures, artists and craftsmen on the right of ownership and used exclusively as creative workshops, ateliers, studios, as well as from living space used to organize non-state museums open to the public , galleries, libraries and other cultural organizations - for the period of their use; from located on plots in horticultural and country non-profit associations of citizens of a residential building with a living area of up to 50 square meters. m. and outbuildings and facilities with a total area of up to 50 sq. m.

TAX PERIOD OF TAX ON PROPERTY OF INDIVIDUALS Tax period is a calendar year. There are no reporting periods. The tax is calculated by the tax authorities on the basis of information submitted to the tax authorities that carry out cadastral registration, maintenance of the state real estate cadastre and state registration rights to real estate and transactions with it, as well as bodies technical inventory, as of January 1 current year. Information must be provided annually no later than March 1.

TAX PERIOD OF TAX ON PROPERTY OF INDIVIDUALS Tax period is a calendar year. There are no reporting periods. The tax is calculated by the tax authorities on the basis of information submitted to the tax authorities that carry out cadastral registration, maintenance of the state real estate cadastre and state registration rights to real estate and transactions with it, as well as bodies technical inventory, as of January 1 current year. Information must be provided annually no later than March 1.

TERMS OF PAYMENT The procedure and terms of tax payment are established by the decision of the local self-government body on the tax.

TERMS OF PAYMENT The procedure and terms of tax payment are established by the decision of the local self-government body on the tax.

"Introduction of a tax on the property of individuals based on the cadastral value of real estate objects" Administration of the rural settlement Kurumoch municipal district Volzhsky, Samara region

Real estate tax has changed in Russia In Russia, the rules for calculating real estate tax have changed, now it is calculated taking into account the cadastral value of the object. From January 1, 2015, the Tax Code of the Russian Federation was replenished with Chapter 32 “Tax on real estate of individuals”. One of the main changes introduced by the new chapter of the Tax Code of the Russian Federation is the transition to the calculation of property tax based on its cadastral value, and not inventory, as it was before.

Changes in tax legislation in terms of tax on property of individuals Law of the Russian Federation of 04.10.2014 No. 284-FZ “On Amending Articles 12 and 85 of Part One and Part Two of the Tax Code of the Russian Federation and Recognizing the Law of the Russian Federation “On Taxes on Property of Individuals” as invalid » Chapter 32 of the Tax Code of the Russian Federation "Tax on property of individuals" based on the cadastral value based on the inventory value Implementation: Law of the Samara Region dated November 10, 2014 No. tax on property of individuals based on the cadastral value of objects of taxation” (not earlier than January 01, 2016). Implementation: Adopt and publish in each municipality legal act on the imposition of a tax. until 28.11.2014

The range of taxable real estate has expanded. In addition to owned residential buildings, apartments, rooms in residential premises, garages and buildings on summer cottages, freehold parking spaces (parking space) and construction in progress, not yet taxed, which will affect the interests of people who purchase apartments during the construction phase, including investment buyers.

Objects, rates and benefits for the property tax of individuals

Property Maximum rate, % Apartments, rooms, residential buildings, garages, parking space, buildings in suburban areas 0, 1 Administrative, business and shopping centers, objects whose cadastral value exceeds 300 million rubles 2 Other objects subject to taxation 0, 5 The cadastral valuation will take into account the location, area and year of construction of the property, so it will be close to the value of housing on the market. Data on the cadastral value of real estate can be found on the Rosreestr website. The new chapter of the Tax Code provides for the right of the owner to a tax deduction, that is, from total area real estate tax inspectors will have to deduct the non-taxable part: 20 sq.m. - from the area of the apartment, 10 sq.m. - from the area of \u200b\u200bthe room, 50 sq. m. - from a residential building.

When calculating the tax based on the cadastral value, the cadastral value of the object specified in the state cadastre real estate as of January 1 of the year that is the tax period. It is reduced by the following tax deductions: - for an apartment - by the cost of 20 sq. m of its total area; - per room - for the cost of 10 sq. m of its total area; - on residential building- for the cost of 50 sq. m of its total area; - for a single real estate complex, which includes at least one residential building (residential building) - by 1 million rubles.

For example, if a citizen is the owner of an apartment with an area of 80 sq.m, the deduction for the apartment is 20 sq.m, you will have to pay tax from an area of 60 sq.m. For a residential building with an area of 120 sq.m, the tax will be calculated from 70 sq.m of the house. On the territory of the Samara Region, differentiated tax rates have been established for residential properties, depending on their cadastral value and type. If an apartment or residential building has a cadastral value of up to 4 million rubles, then the rate will be 0.1%; if from 4 million rubles to 7, then the rate is 0.15%; over 7 and up to 10 million rubles inclusive - the rate is 0.18%; at a cost of more than 10 million rubles - the rate is 0.2%. In relation to objects of construction in progress, if the designed purpose of such objects is a residential building, the tax rate is set at 0.3%. At a rate of 0.1%, a tax rate will be applied for garages and parking spaces, as well as utility buildings or structures, the area of each of which does not exceed 50 square meters. m located on land plots provided for personal subsidiary, dacha farming, gardening, horticulture or individual housing construction. For other objects of non-residential taxation, the tax rate is set at 0.5%. Such objects can be a commercial premises or a hairdressing salon.

Please note that during the first four years from the date of the introduction of the tax, a gradual increase is provided tax burden by applying reduction factors: - for 2015 - 0.2; - for 2016 - 0.4; - for 2017 - 0.6; - for 2018 - 0.8 (clause 8, article 408, chapter 32 of the Tax Code of the Russian Federation). To calculate the tax from the cadastral value, the following formula will be applied: H = (H1-H2)*K+H2, where H is the amount of tax payable; H1 - the amount of tax, based on the cadastral value; H2 - the amount of tax, based on the inventory value; K is the reduction factor for the respective year. From 2019, the tax on the cadastral value will be paid in full. For example, in an apartment with an area of 41.6 sq. m tax will change as follows: - 2014 - 183 rubles (based on inventory value); - 2015 - 376 rubles (based on the cadastral value); - 2016 - 570 rubles; - 2017 - 763 rubles; - 2018 - 956 rubles; - 2019 - 1,149 rubles.

You can now make a preliminary calculation of the future property tax based on the cadastral value that Samara residents will have to pay in 2016 on the website of the Federal Tax Service in the “Personal Property Tax 2016” section. Here you will find detailed information about the features of the new procedure for taxing the property of individuals, tax rates, as well as the ability to calculate the amount of future tax. The online calculator for calculating real estate tax "Preliminary calculation of personal property tax based on the cadastral value" will help you easily calculate the tax according to the new rules that came into force on January 1, 2015. It must be remembered that the transition to new system taxation will be phased and with the application of a reduction factor. Payment of the new tax will begin in 2016, and citizens will have to pay its full amount from 2020. Moreover, when calculating the tax based on the cadastral value, it is provided for the application tax deductions- reduction of the cadastral value by the cadastral value of 10 sq.m. in relation to rooms, 20 sq.m. for apartments, 50 sq. m. in relation to residential buildings.

For example, a pensioner - a disabled person of the second group (a beneficiary for two reasons - a disabled person and a pensioner) is the owner of an apartment, room, cottage, garage and parking space. Let's say a pensioner decided to apply the benefit to a garage, an apartment and a summer house. So, a garage and a car - a place belong to the same type of taxation objects, an apartment and a room - also one type. He will have to pay tax for a room and a car - a place. Tax on the property of individuals for 2015, calculated on the basis of the cadastral value, is payable no later than October 1, 2016. In 2015, the tax on the property of individuals will be paid for 2014 based on the inventory value of the property.

Everything existing benefits for the payment of personal property tax are saved. Meanwhile, these benefits will be provided in respect of one real estate object of each type, which must be chosen by the taxpayer. The declarative nature of benefits for the choice of property implies that the beneficiary-owner of several real estate objects will independently send information about his choice to the tax authority annually before November 1, otherwise, the tax authority will choose the "preferential" object on its own. larger amount calculated tax. If the taxpayer has previously submitted an application to the tax authority for the provision of benefits, re-submission of the application is not required. Apart from electronic service A convenient guide for taxpayers will be the informational video material "Tax on property of individuals 2016" developed by the Federal Tax Service of Russia.

In order to increase the collection of tax on personal income, the local government needs to: 1. Control the completeness and timeliness of payment of tax by organizations 2. Work with employers who pay wages workers below living wage and below the industry average by type of economic activity. 3. Send information about employers who refused to take measures to increase wages to the ministries of financial management of the Samara region. 4. Carry out work (monitoring) to identify organizations and their structural divisions who do not pay personal income tax and attract these payers to pay tax. 5. On the basis of information (reports on declaring the income of individuals) provided by the tax authorities, work with organizations on the timely and full payment of personal income tax.

The main areas of work on planning the income of the budget of the rural settlement Kurumoch of the Volzhsky municipal district of the Samara region for 2015-2017 1. Apply the forecast of the socio-economic development of the municipality of the rural settlement Kurumoch tax revenue based on data from large taxpayers, in cooperation with the main administrators of revenues 3. Make calculations on tax and non-tax revenues, taking into account changes in legislation: cadastral valuation of land (since 01.01.2015) 4. Establish by decisions on the budget of the settlement the list of the main incomes of the local self-government body of the settlement

Areas of work of the local self-government body of the rural settlement Kurumoch to provide the budget of the settlement with its own income 1. Development of the tax potential of the territory of the settlement 2. Ensuring 100% collection of taxes and other payments 3. Taking measures to pay off the existing debt on payments to the budget 4. Carrying out explanatory work with taxpayers 5. Use in the work of the Law of the Samara Region dated November 10, 2014 No. 107-GD “On establishing a single date for the start of application in the territory of the Samara Region of the procedure for determining the tax base for the property tax of individuals based on the cadastral value of objects of taxation” 6. Identification of the facts of the use of land plots without title documents 7. Carrying out work with land users to involve them in paperwork

Financial assistance to the budget of the settlement Non-targeted financial aid: Targeted financial assistance from the regional budget: From the regional budget From the district budget Grant to equalize the budgetary security of the settlement Other interbudgetary transfers from the budget of the municipal district Subsidies Subventions

The main stages of the budget process Preparation of the draft budget Consideration of the draft budget Approval of the budget Execution of the budget, preparation of a report on execution and approval No later than December 31 of the current financial year 190 BC RF) Budget control

Ensuring openness and transparency of the budget of the rural settlement Kurumoch Formation of mechanisms for public control over the efficiency and effectiveness of local self-government activities

Requirements Budget Code RF when determining the amount of subsidies to settlements Equalization criterion financial opportunities settlements The volume and distribution of subsidies for equalizing the budgetary security of settlements from the budget of the municipal district are approved by the decision of the representative body of the municipal district on the budget of the municipal district for the next fiscal year(next financial year and planning period Subsidies for equalizing the budgetary security of settlements from the budget of the municipal district, with the exception of subsidies, are provided to rural settlements, the estimated budgetary security of which does not exceed the level established as a criterion for equalizing the estimated budgetary security. Procedure for determining the volume of regional funds for financial support of settlements and distribution of subsidies for equalizing the budgetary security of settlements from the budget of the municipal district is established by the law of the constituent entity of the Russian Federation in accordance with the requirements of this Code. budget device and budget process in the Samara region"

Redistribution of issues of local importance from 01.01.2015 Issues of local importance of rural settlements in accordance with 136-FZ (13 issues out of 39 left) - Budget, local taxes, property; - Providing residents with communication services, Catering, trade and consumer services; - Leisure and culture; - Physical culture and mass sports, - Archival funds; - Activities to work with children and youth; - Assistance in the development of agricultural production, creation of conditions for the development of small and medium-sized businesses; - Approval of the rules for the improvement of the territory, organization of the improvement of the territory; - Naming streets, etc.; - Primary fire safety measures; - Creation of conditions for the activities of voluntary formations of the population for the protection of public order; Issues of local importance of rural settlements in accordance with the Law of the Samara Region dated 03.10.2014 No. 86-GDO assigning issues of local importance to rural settlements Samara region (+12 questions out of 39) Road activities and road safety; Organization of fuel supply to the population; - Providing housing for those in need poor citizens residential premises, organization of construction and maintenance of municipal housing stock; - Organization of collection and removal of household waste and garbage; - Providing support to socially oriented non-profit organizations; - Organization of mass recreation for residents of the settlement; - Organization of funeral services and maintenance of burial sites; - Implementation of the powers of the owner of water bodies, informing the population about the restrictions on their use; - Implementation of anti-corruption measures; - Participation in the prevention and elimination of the consequences of emergencies; - Provision of premises for work and living quarters to precinct officers;

Tax on property of individuals, established by the Tax Code of the Russian Federation and

normative

legal

acts

representative

bodies

municipalities.

By imposing the tax, the representative bodies of the municipalities

formations

(legislative

(representative)

bodies

state authorities determine the tax rate within the limits,

established by this chapter, the procedure and terms for paying tax.

TAX PAYERS

Taxpayers are natural persons who have

ownership of property recognized as an object

taxation.

The object of taxation is located within

municipality the following property:

1) residential building;

2) living quarters (apartment, room);

3) garage, parking place;

4) a single immovable complex;

5) an object of construction in progress;

6) other building, structure, structure, premises.

THE TAX BASE IS DETERMINED IN TWO WAYS:

1. Based on their cadastral value,

tax

base

determined

v

relation

everyone

object

taxation as its cadastral value indicated in

state real estate cadastre as of January 1,

being a tax period.

With regard to the object of taxation formed during the tax

period, the tax base in a given tax period is determined as its

cadastral value on the date of setting such an object for

state cadastral registration.

2. Based on their inventory value,

The tax base is determined for each object of taxation

as its inventory value, calculated taking into account the deflator coefficient based on the latest data on the inventory

the value submitted in accordance with the established procedure to the tax authorities before

March 1, 2013. TAX ON PROPERTY OF INDIVIDUALS

The tax period is a calendar year.

Tax rates are established by regulatory legal acts

representative bodies of municipalities, depending on

the applicable procedure for determining the tax base

In the case of determining the tax base based on the cadastral value

object of taxation, tax rates do not exceed:

1) 0.1 percent in relation to:

residential buildings, residential premises;

objects of construction in progress in the event that the projected

the purpose of such objects is a residential building;

unified immovable complexes, which include at least one

residential premises (residential building);

garages and parking spaces;

economic buildings or structures, the area of each of which

does not exceed 50 square meters and which are located on land

plots provided for personal subsidiary;

2) 2 percent in relation to objects of taxation cadastral

the cost of each of which exceeds 300 million rubles;

3) 0.5 percent in relation to other objects of taxation. TAX ON PROPERTY OF INDIVIDUALS

In the case of determining the tax base based on the inventory

cost tax rates are set based on multiplied by

deflator coefficient of the total inventory value of objects

taxation,

owned

on the

law

property

taxpayer:

Total inventory value of objects

tax multiplied by the deflator coefficient

tax rate

Up to 300,000 rubles inclusive

Up to 0.1 percent

inclusive

Over 300,000 to 500,000 rubles inclusive

Over 0.1 to

0.3 percent

inclusive

Over 500,000 rubles

Over 0.3 to

2.0 percent

inclusive

5TAX ON PROPERTY OF INDIVIDUALS

TAX BENEFITS

1) Heroes of the Soviet Union and Heroes of the Russian Federation, as well as persons awarded

the Order of Glory of three degrees;

2) disabled people of I and II disability groups;

3) disabled since childhood;

4) participants in the Civil War and the Great Patriotic War, other combat

operations to protect the USSR, as well as combat veterans;

5) military personnel, as well as citizens dismissed from military service upon reaching

age limit for military service, health status, having

the total duration of military service is 20 years or more;

6) family members of servicemen who have lost their breadwinner;

10) pensioners receiving pensions appointed in the manner prescribed by

pension legislation, as well as persons who have reached the age of 60 and 55 years

(respectively men and women);

11) parents and spouses of military personnel and civil servants who died during

performance of official duties;

15) individuals - in relation to economic buildings or structures, the area

each of which does not exceed 50 square meters and which are located on

land plots provided for the maintenance of personal subsidiary, dacha

economy, gardening, gardening or individual housing

construction. TAX ON PROPERTY OF INDIVIDUALS

Tax relief is provided for one object

taxation of each type at the choice of the taxpayer outside

depending on the number of grounds for applying tax benefits.

Tax relief is provided for the following types

objects of taxation:

1) apartment or room;

2) residential building;

3) the premises or structure specified in paragraphs. 14 p. 1 art. 407 of the Tax Code of the Russian Federation;

4) economic building or structure specified in paragraphs. 15 p. 1 art.

407 of the Tax Code of the Russian Federation;

5) garage or parking place.

A person entitled to a tax benefit submits to the tax

authority application for benefits and documents confirming

the taxpayer's right to a tax benefit.

Notification of the selected objects of taxation, in relation to

which is provided tax credit, submitted before 1 November of the year,

which is the tax period from which, in respect of

the specified objects the tax privilege is applied. TAX ON PROPERTY OF INDIVIDUALS

PROCEDURE FOR CALCULATION OF THE AMOUNT OF TAX:

The amount of tax is calculated by the tax authorities after the end of the tax

period separately for each object of taxation as

percentage of the tax base corresponding to the tax rate.

The tax is payable by taxpayers no later than October 1

year following the expired tax period.