Kbk in the tax. Kbk tax service

What CBCs for taxes and insurance premiums apply in 2018? What tax on which CBCs to transfer? Where to pay penalties and fines? Are special CSCs used for IP? Were any new codes for personal income tax and USN introduced? Any accountant faces similar questions in the course of work. In this article, we will provide a table of KBK with decoding. You can also read the comments on the procedure for filling out payment orders and the indications in them of the CCC in 2018. You may want to bookmark this article in your browser as it can serve as your guide to CCC (including past payments). If you have any further questions, please contact free consultation to our accounting.

Purpose of budget classification codes in 2018

The code budget classification(KBK) - a combination of numbers known to accountants, as well as employees of banking and budget institutions. Characterizes a certain money transaction and is a convenient way to group expenses / incomes paid to the budget. Created on the basis Budget Code RF.

The CSC directory changes and improves quite often: in 2018, new codes are introduced, the old ones are corrected. If you are interested in the question specifically about the new CSCs in 2018, then we recommend that you read a special article on this subject. Cm. " ".

What do these numbers actually mean?

In accordance with the order of the Ministry of Finance No. 65n, the budget classification code consists of 20 digits. Conventionally, they can be divided into several groups, consisting of 1-5 characters:

- №1-3 - a code indicating the addressee for whom the cash receipts are intended (territorial Federal Tax Service, insurance and pension funds). For example, to pay the BCC for personal income tax in 2018, the number "182" is put, for insurance premiums in Pension Fund- "392";

- № 4 - show the group cash receipts.

- №5-6 - reflects the tax code. For example, for insurance premiums, the value "02" is indicated, excises and insurance premiums are characterized by the number "03", payment of state duty - "08".

- № 7-11 – elements that reveal the item and subitem of income.

- No. 12 and 13- reflect the level of the budget in which it is planned to receive Money. The federal code is "01", the regional one is "02". Municipal institutions the numbers "03", "04" or "05" are allotted. The remaining figures characterize the budget and insurance funds.

- №14-17 - indicate the reason for the execution financial transaction: making the main payment - "1000", accruing a penalty fee - "2100", paying a fine - "3000", deduction of interest - "2200".

- №18 – 20 - reflects the category of income received by the government department. For example, funds intended to pay tax are reflected in the code "110", and gratuitous receipts - "150".

In 2018 (KBK) is reflected in a separate field of payment orders intended for the deduction of taxes, insurance premiums, penalties and fines, as well as a number of other payments to the budget. This field in 2018 is 104 (as before).

If you make a mistake in the CBC

In 2018, a payment order is one of the methods of cashless payments in the territory Russian Federation. Payments must be made according to established forms, and all their sections should be completed in strict accordance with the instructions of the Ministry of Finance. For settlements with the budget, field 104 is mandatory.

When filling out the document, it is important to correctly indicate the combination of numbers, because the mistake made entails the need to clarify the payments made. However, it should be noted that in some cases, incorrectly filling in column 104 of the payment order in the form of an erroneous budget classification code cannot lead to such negative consequences for payers. For example, the Ministry of Finance, in its Letter No. 03-02-08/31 dated March 29, 2012, noted that an incorrect indication of the CCC does not entail an unequivocal recognition of the unfulfilled obligation to pay taxes transferred to the incorrect CCC.

The above is true for taxes. If an erroneous code is indicated, for example, in a payment for the payment of the state fee, then the enterprise may be denied the provision of the relevant services due to the erroneous filling of field 104 in payment order.

Note that when filling out payment orders in 2018, companies and individual entrepreneurs who fill them out in in electronic format with the help of special accounting services. In them, the BCC is affixed automatically and the probability of error is practically eliminated. If you do not want to use tables, then you can. Select the required tax or contributions, and the correct CCC will appear automatically.

Next, we present the KBK guide for 2018 on basic taxes, insurance premiums, excises, state duty etc. The directory is presented in the form of a table with a breakdown by purpose of payment, penalties and fines. The guide can be useful to organizations and individual entrepreneurs.

| Purpose | Mandatory payment | penalties | Fine | |

VAT |

||||

| from sales in Russia | 182 1 03 01000 01 1000 110 | 182 1 03 01000 01 2100 110 | 182 1 03 01000 01 3000 110 | |

| when importing goods from member countries Customs Union- through the tax office | 182 1 04 01000 01 1000 110 | 182 1 04 01000 01 2100 110 | 182 1 04 01000 01 3000 110 | |

| when importing goods - at customs | 153 1 04 01000 01 1000 110 | 153 1 04 01000 01 2100 110 | 153 1 04 01000 01 3000 110 | |

excises |

||||

Excises on goods produced in Russia |

||||

| 182 1 03 02011 01 1000 110 | 182 1 03 02011 01 2100 110 | 182 1 03 02011 01 3000 110 | ||

| 182 1 03 02012 01 1000 110 | 182 1 03 02012 01 2100 110 | 182 1 03 02012 01 3000 110 | ||

| wine, grape, fruit, cognac, calvados, whiskey distillates | 182 1 03 02013 01 1000 110 | 182 1 03 02013 01 2100 110 | 182 1 03 02013 01 3000 110 | |

| alcohol-containing products | 182 1 03 02020 01 1000 110 | 182 1 03 02020 01 2100 110 | 182 1 03 02020 01 3000 110 | |

| tobacco products | 182 1 03 02030 01 1000 110 | 182 1 03 02030 01 2100 110 | 182 1 03 02030 01 3000 110 | |

| 182 1 03 02360 01 1000 110 | 182 1 03 02360 01 2100 110 | 182 1 03 02360 01 3000 110 | ||

| nicotine liquids | 182 1 03 02370 01 1000 110 | 182 1 03 02370 01 2100 110 | 182 1 03 02370 01 3000 110 | |

| 182 1 03 02380 01 1000 110 | 182 1 03 02380 01 2100 110 | 182 1 03 02380 01 3000 110 | ||

| motor gasoline | 182 1 03 02041 01 1000 110 | 182 1 03 02041 01 2100 110 | 182 1 03 02041 01 3000 110 | |

| straight-run gasoline | 182 1 03 02042 01 1000 110 | 182 1 03 02042 01 2100 110 | 182 1 03 02042 01 3000 110 | |

| cars and motorcycles | 182 1 03 02060 01 1000 110 | 182 1 03 02060 01 2100 110 | 182 1 03 02060 01 3000 110 | |

| diesel fuel | 182 1 03 02070 01 1000 110 | 182 1 03 02070 01 2100 110 | 182 1 03 02070 01 3000 110 | |

| 182 1 03 02080 01 1000 110 | 182 1 03 02080 01 2100 110 | 182 1 03 02080 01 3000 110 | ||

| 182 1 03 02090 01 1000 110 | 182 1 03 02090 01 2100 110 | 182 1 03 02090 01 3000 110 | ||

| beer | 182 1 03 02100 01 1000 110 | 182 1 03 02100 01 2100 110 | 182 1 03 02100 01 3000 110 | |

| 182 1 03 02141 01 1000 110 | 182 1 03 02141 01 2100 110 | 182 1 03 02141 01 3000 110 | ||

| 182 1 03 02142 01 1000 110 | 182 1 03 02142 01 2100 110 | 182 1 03 02142 01 3000 110 | ||

| cider, poiret, mead | 182 1 03 02120 01 1000 110 | 182 1 03 02120 01 2100 110 | 182 1 03 02120 01 3000 110 | |

| benzene, paraxylene, orthoxylene | 182 1 03 02300 01 1000 110 | 182 1 03 02300 01 2100 110 | 182 1 03 02300 01 3000 110 | |

| aviation kerosene | 182 1 03 02310 01 1000 110 | 182 1 03 02310 01 2100 110 | 182 1 03 02310 01 3000 110 | |

| middle distillates | 182 1 03 02330 01 1000 110 | 182 1 03 02330 01 2100 110 | 182 1 03 02330 01 3000 110 | |

| wines with a protected geographical indication, with a protected designation of origin, other than sparkling wines (champagne) | 182 1 03 02340 01 1000 110 | 182 1 03 02340 01 2100 110 | 182 1 03 02340 01 3000 110 | |

| sparkling wines (champagne) with a protected geographical indication, with a protected designation of origin | 182 1 03 02350 01 1000 110 | 182 1 03 02350 01 2100 110 | 182 1 03 02350 01 3000 110 | |

Excises on goods imported from the member states of the Customs Union (payment of excise through tax inspections) |

||||

| ethyl alcohol from food raw materials. In addition to distillates of wine, grape, fruit, cognac, Calvados, whiskey | 182 1 04 02011 01 1000 110 | 182 1 04 02011 01 2100 110 | 182 1 04 02011 01 3000 110 | |

| 182 1 04 02012 01 1000 110 | 182 1 04 02012 01 2100 110 | 182 1 04 02012 01 3000 110 | ||

| cider, poiret, mead | 182 1 04 02120 01 1000 110 | 182 1 04 02120 01 2100 110 | 182 1 04 02120 01 3000 110 | |

| ethyl alcohol from non-food raw materials | 182 1 04 02013 01 1000 110 | 182 1 04 02013 01 2100 110 | 182 1 04 02013 01 3000 110 | |

| alcohol-containing products | 182 1 04 02020 01 1000 110 | 182 1 04 02020 01 2100 110 | 182 1 04 02020 01 3000 110 | |

| tobacco products | 182 1 04 02030 01 1000 110 | 182 1 04 02030 01 2100 110 | 182 1 04 02030 01 3000 110 | |

| electronic nicotine delivery systems | 182 1 04 02180 01 1000 110 | 182 1 04 02180 01 2100 110 | 182 1 04 02180 01 3000 110 | |

| nicotine liquids | 182 1 04 02190 01 1000 110 | 182 1 04 02190 01 2100 110 | 182 1 04 02190 01 3000 110 | |

| tobacco and tobacco products intended for consumption by heating | 182 1 04 02200 01 1000 110 | 182 1 04 02200 01 2100 110 | 182 1 04 02200 01 3000 110 | |

| motor gasoline | 182 1 04 02040 01 1000 110 | 182 1 04 02040 01 2100 110 | 182 1 04 02040 01 3000 110 | |

| 182 1 04 02060 01 1000 110 | 182 1 04 02060 01 2100 110 | 182 1 04 02060 01 3000 110 | ||

| diesel fuel | 182 1 04 02070 01 1000 110 | 182 1 04 02070 01 2100 110 | 182 1 04 02070 01 3000 110 | |

| engine oils for diesel, carburetor (injector) engines | 182 1 04 02080 01 1000 110 | 182 1 04 02080 01 2100 110 | 182 1 04 02080 01 3000 110 | |

| fruit, sparkling (champagne) and other wines, wine drinks, without rectified ethyl alcohol | 182 1 04 02090 01 1000 110 | 182 1 04 02090 01 2100 110 | 182 1 04 02090 01 3000 110 | |

| beer | 182 1 04 02100 01 1000 110 | 182 1 04 02100 01 2100 110 | 182 1 04 02100 01 3000 110 | |

| alcoholic products with a volume fraction of ethyl alcohol over 9 percent. Except beer, wine, wine drinks, without rectified ethyl alcohol | 182 1 04 02141 01 1000 110 | 182 1 04 02141 01 2100 110 | 182 1 04 02141 01 3000 110 | |

| alcoholic products with a volume fraction of ethyl alcohol up to 9 percent. Except beer, wine, wine drinks, without rectified ethyl alcohol | 182 1 04 02142 01 1000 110 | 182 1 04 02142 01 2100 110 | 182 1 04 02142 01 3000 110 | |

| straight-run gasoline | 182 1 04 02140 01 1000 110 | 182 1 04 02140 01 2100 110 | 182 1 04 02140 01 3000 110 | |

| middle distillates | 182 1 04 02170 01 1000 110 | 182 1 04 02170 01 2100 110 | 182 1 04 02170 01 3000 110 | |

Excises on goods imported from other countries (payment of excise at customs) |

||||

| ethyl alcohol from food raw materials. In addition to distillates of wine, grape, fruit, cognac, Calvados, whiskey | 153 1 04 02011 01 1000 110 | 153 1 04 02011 01 2100 110 | 153 1 04 02011 01 3000 110 | |

| distillates - wine, grape, fruit, cognac, calvados, whiskey | 153 1 04 02012 01 1000 110 | 153 1 04 02012 01 2100 110 | 153 1 04 02012 01 3000 110 | |

| cider, poiret, mead | 153 1 04 02120 01 1000 110 | 153 1 04 02120 01 2100 110 | 153 1 04 02120 01 3000 110 | |

| ethyl alcohol from non-food raw materials | 153 1 04 02013 01 1000 110 | 153 1 04 02013 01 2100 110 | 153 1 04 02013 01 3000 110 | |

| alcohol-containing products | 153 1 04 02020 01 1000 110 | 153 1 04 02020 01 2100 110 | 153 1 04 02020 01 3000 110 | |

| tobacco products | 153 1 04 02030 01 1000 110 | 153 1 04 02030 01 2100 110 | 153 1 04 02030 01 3000 110 | |

| electronic nicotine delivery systems | 153 1 04 02180 01 1000 110 | 153 1 04 02180 01 2100 110 | 153 1 04 02180 01 3000 110 | |

| nicotine liquids | 153 1 04 02190 01 1000 110 | 153 1 04 02190 01 2100 110 | 153 1 04 02190 01 3000 110 | |

| tobacco and tobacco products intended for consumption by heating | 153 1 04 02200 01 1000 110 | 153 1 04 02200 01 2100 110 | 153 1 04 02200 01 3000 110 | |

| motor gasoline | 153 1 04 02040 01 1000 110 | 153 1 04 02040 01 2100 110 | 153 1 04 02040 01 3000 110 | |

| cars and motorcycles | 153 1 04 02060 01 1000 110 | 153 1 04 02060 01 2100 110 | 153 1 04 02060 01 3000 110 | |

| diesel fuel | 153 1 04 02070 01 1000 110 | 153 1 04 02070 01 2100 110 | 153 1 04 02070 01 3000 110 | |

| engine oils for diesel, carburetor (injector) engines | 153 1 04 02080 01 1000 110 | 153 1 04 02080 01 2100 110 | 153 1 04 02080 01 3000 110 | |

| fruit, sparkling (champagne) and other wines, wine drinks, without rectified ethyl alcohol | 153 1 04 02090 01 1000 110 | 153 1 04 02090 01 2100 110 | 153 1 04 02090 01 3000 110 | |

| beer | 153 1 04 02100 01 1000 110 | 153 1 04 02100 01 2100 110 | 153 1 04 02100 01 3000 110 | |

| alcoholic products with a volume fraction of ethyl alcohol over 9 percent. Except beer, wine, wine drinks, without rectified ethyl alcohol | 153 1 04 02141 01 1000 110 | 153 1 04 02141 01 2100 110 | 153 1 04 02141 01 3000 110 | |

| alcoholic products with a volume fraction of ethyl alcohol up to 9 percent. Except beer, wine, wine drinks, without rectified ethyl alcohol | 153 1 04 02142 01 1000 110 | 153 1 04 02142 01 2100 110 | 153 1 04 02142 01 3000 110 | |

| straight-run gasoline | 153 1 04 02140 01 1000 110 | 153 1 04 02140 01 2100 110 | 153 1 04 02140 01 3000 110 | |

| middle distillates | 153 1 04 02170 01 1000 110 | 153 1 04 02170 01 2100 110 | 153 1 04 02170 01 3000 110 | |

personal income tax(regardless of tax rate) |

||||

| payable by the withholding agent | 182 1 01 02010 01 1000 110 | 182 1 01 02010 01 2100 110 | 182 1 01 02010 01 3000 110 | |

| paid by entrepreneurs and persons engaged in private practice, including notaries and lawyers (Article 227 of the Tax Code of the Russian Federation) | 182 1 01 02020 01 1000 110 | 182 1 01 02020 01 2100 110 | 182 1 01 02020 01 3000 110 | |

| paid by the resident independently, including from income from the sale of personal property | 182 1 01 02030 01 1000 110 | 182 1 01 02030 01 2100 110 | 182 1 01 02030 01 3000 110 | |

| in the form of fixed advance payments from the income of foreigners who work on the basis of a patent | 182 1 01 02040 01 1000 110 | – | – | |

income tax |

||||

| v federal budget(except for consolidated groups of taxpayers) | 182 1 01 01011 01 1000 110 | 182 1 01 01011 01 2100 110 | 182 1 01 01011 01 3000 110 | |

| to the budgets of the constituent entities of the Russian Federation (except for consolidated groups of taxpayers) | 182 1 01 01012 02 1000 110 | 182 1 01 01012 02 2100 110 | 182 1 01 01012 02 3000 110 | |

| to the federal budget (for consolidated groups of taxpayers) | 182 1 01 01013 01 1000 110 | 182 1 01 01013 01 2100 110 | 182 1 01 01013 01 3000 110 | |

| to the budgets of the constituent entities of the Russian Federation (for consolidated groups of taxpayers) | 182 1 01 01014 02 1000 110 | 182 1 01 01014 02 2100 110 | 182 1 01 01014 02 3000 110 | |

| when fulfilling production sharing agreements concluded before October 21, 2011 (before the entry into force of the Law of December 30, 1995 No. 225-FZ) | 182 1 01 01020 01 1000 110 | 182 1 01 01020 01 2100 110 | 182 1 01 01020 01 3000 110 | |

| from income foreign organizations not related to activities in Russia through a permanent establishment | 182 1 01 01030 01 1000 110 | 182 1 01 01030 01 2100 110 | 182 1 01 01030 01 3000 110 | |

| from income Russian organizations in the form of dividends from Russian organizations | 182 1 01 01040 01 1000 110 | 182 1 01 01040 01 2100 110 | 182 1 01 01040 01 3000 110 | |

| from income of foreign organizations in the form of dividends from Russian organizations | 182 1 01 01050 01 1000 110 | 182 1 01 01050 01 2100 110 | 182 1 01 01050 01 3000 110 | |

| from dividends from foreign organizations | 182 1 01 01060 01 1000 110 | 182 1 01 01060 01 2100 110 | 182 1 01 01060 01 3000 110 | |

| from interest on state and municipal securities | 182 1 01 01070 01 1000 110 | 182 1 01 01070 01 2100 110 | 182 1 01 01070 01 3000 110 | |

| from interest on bonds of Russian organizations | 182 1 01 01090 01 1000 110 | 1 01 01090 01 2100 110 | 1 01 01090 01 3000 110 | |

| from profits of controlled foreign companies | 182 1 01 01080 01 1000 110 | 182 1 01 01080 01 2100 110 | 182 1 01 01080 01 3000 110 | |

Fee for the use of objects of aquatic biological resources |

||||

| except for inland water bodies | 182 1 07 04020 01 1000 110 | 182 1 07 04020 01 2100 110 | 182 1 07 04020 01 3000 110 | |

| only for internal water bodies | 182 1 07 04030 01 1000 110 | 182 1 07 04030 01 2100 110 | 182 1 07 04030 01 3000 110 | |

| Fee for the use of wildlife objects | 182 1 07 04010 01 1000 110 | 182 1 07 04010 01 2100 110 | 182 1 07 04010 01 3000 110 | |

water tax |

||||

| water tax | 182 1 07 03000 01 1000 110 | 182 1 07 03000 01 2100 110 | 182 1 07 03000 01 3000 110 | |

NDPI |

||||

| oil | 182 1 07 01011 01 1000 110 | 182 1 07 01011 01 2100 110 | 182 1 07 01011 01 3000 110 | |

| combustible natural gas from all types of hydrocarbon deposits | 182 1 07 01012 01 1000 110 | 182 1 07 01012 01 2100 110 | 182 1 07 01012 01 3000 110 | |

| gas condensate from all types of hydrocarbon deposits | 182 1 07 01013 01 1000 110 | 182 1 07 01013 01 2100 110 | 182 1 07 01013 01 3000 110 | |

| common minerals | 182 1 07 01020 01 1000 110 | 182 1 07 01020 01 2100 110 | 182 1 07 01020 01 3000 110 | |

| other minerals. In addition to natural diamonds | 182 1 07 01030 01 1000 110 | 182 1 07 01030 01 2100 110 | 182 1 07 01030 01 3000 110 | |

| minerals mined on the continental shelf or in the exclusive economic zone Russian Federation or from subsoil outside the territory of the Russian Federation | 182 1 07 01040 01 1000 110 | 182 1 07 01040 01 2100 110 | 182 1 07 01040 01 3000 110 | |

| natural diamonds | 182 1 07 01050 01 1000 110 | 182 1 07 01050 01 2100 110 | 182 1 07 01050 01 3000 110 | |

| coal | 182 1 07 01060 01 1000 110 | 182 1 07 01060 01 2100 110 | 182 1 07 01060 01 3000 110 | |

ESHN |

||||

| ESHN | 182 1 05 03010 01 1000 110 | 182 1 05 03010 01 2100 110 | 182 1 05 03010 01 3000 110 | |

Single tax with simplification (STS) |

||||

| from income (6%) | 182 1 05 01011 01 1000 110 | 182 1 05 01011 01 2100 110 | 182 1 05 01011 01 3000 110 | |

| on income less expenses (15%), including minimum tax | 182 1 05 01021 01 1000 110 | 182 1 05 01021 01 2100 110 | 182 1 05 01021 01 3000 110 | |

UTII |

||||

| UTII | 182 1 05 02010 02 1000 110 | 182 1 05 02010 02 2100 110 | 182 1 05 02010 02 3000 110 | |

Patent |

||||

| tax to the budgets of city districts | 182 1 05 04010 02 1000 110 | 182 1 05 04010 02 2100 110 | 182 1 05 04010 02 3000 110 | |

| tax to the budgets of municipal districts | 182 1 05 04020 02 1000 110 | 182 1 05 04020 02 2100 110 | 182 1 05 04020 02 3000 110 | |

| tax to the budgets of Moscow, St. Petersburg and Sevastopol | 182 1 05 04030 02 1000 110 | 182 1 05 04030 02 2100 110 | 182 1 05 04030 02 3000 110 | |

| tax to the budgets of urban districts with intracity division | 182 1 05 04040 02 1000 110 | 182 1 05 04040 02 2100 110 | 182 1 05 04040 02 3000 110 | |

| to the budgets of intracity districts | 182 1 05 04050 02 1000 110 | 182 1 05 04050 02 2100 110 | 182 1 05 04050 02 3000 110 | |

Transport tax |

||||

| from organizations | 182 1 06 04011 02 1000 110 | 182 1 06 04011 02 2100 110 | 182 1 06 04011 02 3000 110 | |

| from individuals | 182 1 06 04012 02 1000 110 | 182 1 06 04012 02 2100 110 | 182 1 06 04012 02 3000 110 | |

Gambling business tax |

||||

| Gambling business tax | 182 1 06 05000 02 1000 110 | 182 1 06 05000 02 2100 110 | 182 1 06 05000 02 3000 110 | |

Corporate property tax |

||||

| on property not included in the Unified Gas Supply System | 182 1 06 02010 02 1000 110 | 182 1 06 02010 02 2100 110 | 182 1 06 02010 02 3000 110 | |

| on property included in the Unified Gas Supply System | 182 1 06 02020 02 1000 110 | 182 1 06 02020 02 2100 110 | 182 1 06 02020 02 3000 110 | |

Personal property tax |

||||

| in Moscow, St. Petersburg and Sevastopol | 182 1 06 01010 03 1000 110 | 182 1 06 01010 03 2100 110 | 182 1 06 01010 03 3000 110 | |

| within urban districts | 182 1 06 01020 04 1000 110 | 182 1 06 01020 04 2100 110 | 182 1 06 01020 04 3000 110 | |

| 182 1 06 01020 11 1000 110 | 182 1 06 01020 11 2100 110 | 182 1 06 01020 11 3000 110 | ||

| 182 1 06 01020 12 1000 110 | 182 1 06 01020 12 2100 110 | 182 1 06 01020 12 3000 110 | ||

| 182 1 06 01030 05 1000 110 | 182 1 06 01030 05 2100 110 | 182 1 06 01030 05 3000 110 | ||

| 182 1 06 01030 10 1000 110 | 182 1 06 01030 10 2100 110 | 182 1 06 01030 10 3000 110 | ||

| 182 1 06 01030 13 1000 110 | 182 1 06 01030 13 2100 110 | 182 1 06 01030 13 3000 110 | ||

Land tax (for organizations) |

||||

| 182 1 06 06031 03 1000 110 | 182 1 06 06031 03 2100 110 | 182 1 06 06031 03 3000 110 | ||

| within urban districts | 182 1 06 06032 04 1000 110 | 182 1 06 06032 04 2100 110 | 182 1 06 06032 04 3000 110 | |

| within the boundaries of urban districts with intracity division | 182 1 06 06032 11 1000 110 | 182 1 06 06032 11 2100 110 | 182 1 06 06032 11 3000 110 | |

| within the boundaries of urban areas | 182 1 06 06032 12 1000 110 | 182 1 06 06032 12 2100 110 | 182 1 06 06032 12 3000 110 | |

| within the boundaries of inter-settlement territories | 182 1 06 06033 05 1000 110 | 182 1 06 06033 05 2100 110 | 182 1 06 06033 05 3000 110 | |

| within the boundaries of rural settlements | 182 1 06 06033 10 1000 110 | 182 1 06 06033 10 2100 110 | 182 1 06 06033 10 3000 110 | |

| within the boundaries of urban settlements | 182 1 06 06033 13 1000 110 | 182 1 06 06033 13 2100 110 | 182 1 06 06033 13 3000 110 | |

Land tax (for individuals) |

||||

| within the boundaries of Moscow, St. Petersburg and Sevastopol | 182 1 06 06041 03 1000 110 | 182 1 06 06041 03 2100 110 | 182 1 06 06041 03 3000 110 | |

| within urban districts | 182 1 06 06042 04 1000 110 | 182 1 06 06042 04 2100 110 | 182 1 06 06042 04 3000 110 | |

| within the boundaries of urban districts with intracity division | 182 1 06 06042 11 1000 110 | 182 1 06 06042 11 2100 110 | 182 1 06 06042 11 3000 110 | |

| within the boundaries of urban areas | 182 1 06 06042 12 1000 110 | 182 1 06 06042 12 2100 110 | 182 1 06 06042 12 3000 110 | |

| within the boundaries of inter-settlement territories | 182 1 06 06043 05 1000 110 | 182 1 06 06043 05 2100 110 | 182 1 06 06043 05 3000 110 | |

| within the boundaries of rural settlements | 182 1 06 06043 10 1000 110 | 182 1 06 06043 10 2100 110 | 182 1 06 06043 10 3000 110 | |

| within the boundaries of urban settlements | 182 1 06 06043 13 1000 110 | 182 1 06 06043 13 2100 110 | 182 1 06 06043 13 3000 110 | |

Trading fee |

||||

| Sales tax paid in the territories of federal cities | 182 1 05 05010 02 1000 110 | 182 1 05 05010 02 2100 110 | 182 1 05 05010 02 3000 110 | |

Recycling collection |

||||

| Recycling fee for wheeled vehicles (chassis) and their trailers imported into Russia from any country except Belarus | 153 1 12 08000 01 1000 120 | 153 1 12 08000 01 1010 120 | – | |

| Utilization fee for wheeled vehicles (chassis) and their trailers imported into Russia from Belarus | 153 1 12 08000 01 3000 120 | 153 1 12 08000 01 3010 120 | – | |

| Utilization fee for wheeled vehicles (chassis) and their trailers produced in Russia | 182 1 12 08000 01 2000 120 | – | – | |

| Utilization fee for self-propelled vehicles and trailers for them imported into Russia from any country except Belarus | 153 1 12 08000 01 5000 120 | – | – | |

| Recycling fee for self-propelled vehicles and trailers imported into Russia from Belarus | 153 1 12 08000 01 7000 120 | – | – | |

| Utilization fee for self-propelled machines and trailers for them produced in Russia | 182 1 12 08000 01 6000 120 | – | – | |

Ecological fee |

||||

| Ecological fee | 048 1 12 08010 01 6000 120 | – | – | |

Insurance premiums (payment to the Federal Tax Service) |

||||

| for the insurance pension for the periods from January 1, 2017 (in 2018 we pay for 2017–2018) | 182 1 02 02010 06 1010 160 | 182 1 02 02010 06 2110 160 | 182 1 02 02010 06 3010 160 | |

| for a funded pension | 182 1 02 02020 06 1000 160 | 182 1 02 02020 06 2100 160 | 182 1 02 02020 06 3000 160 | |

| for additional payment to pension for members of flight crews of civil aviation aircraft | 182 1 02 02080 06 1000 160 | 182 1 02 02080 06 2100 160 | 182 1 02 02080 06 3000 160 | |

| for additional payment to pensions for employees of organizations of the coal industry | 182 1 02 02120 06 1000 160 | 182 1 02 02120 06 2100 160 | 182 1 02 02120 06 3000 160 | |

| in a fixed amount for an insurance pension (from incomes within and over 300,000 rubles) for periods from January 1, 2017 (in 2018 we pay for 2017–2018) | 182 1 02 02140 06 1110 160 | 182 1 02 02140 06 2110 160 | 182 1 02 02140 06 3010 160 | |

| on the insurance part labor pension at an additional rate for employees under list 1 (in 2018 we pay for 2017–2018) | 182 1 02 02131 06 2100 160 | 182 1 02 02131 06 3000 160 | ||

| for the insurance part of the labor pension at an additional rate for employees under list 2 (in 2018 we pay for 2017–2018) | 182 1 02 02132 06 2100 160 | 182 1 02 02132 06 3000 160 | ||

| in case of temporary disability and in connection with motherhood for the periods from January 1, 2017 (in 2018 we pay for 2017-2018) | 182 1 02 02090 07 1010 160 | 182 1 02 02090 07 2110 160 | 182 1 02 02090 07 3010 160 | |

| in FFOMS for the periods from January 1, 2017 (in 2018 we pay for 2017-2018) | 182 1 02 02101 08 1013 160 | 182 1 02 02101 08 2013 160 | 182 1 02 02101 08 3013 160 | |

| in the FFOMS in a fixed amount for the periods from January 1, 2017 (in 2018 we pay for 2017–2018) | 182 1 02 02103 08 1013 160 | 182 1 02 02103 08 2013 160 | 182 1 02 02103 08 3013 160 | |

Insurance premiums (payment to the FSS) |

||||

| for insurance against accidents at work and occupational diseases | 393 1 02 02050 07 1000 160 | 393 1 02 02050 07 2100 160 | 393 1 02 02050 07 3000 160 | |

Insurance premiums (payment to the Pension Fund) |

||||

| additional contributions to the funded pension (at the request of an employee participating in the state co-financing program) | 392 1 02 02041 06 1100 160 | – | – | |

| employer's contributions in favor of insured persons for funded pension (from the employer's funds) | 392 1 02 02041 06 1200 160 | – | – | |

Government duty |

||||

| litigation in arbitration courts | 182 1 08 01000 01 1000 110 | |||

| on proceedings in the Constitutional Court of the Russian Federation | 182 1 08 02010 01 1000 110 | |||

| on proceedings in the constitutional (charter) courts of the constituent entities of the Russian Federation | 182 1 08 02020 01 1000 110 | |||

| on proceedings in courts of general jurisdiction, justices of the peace. In addition to the Supreme Court of the Russian Federation | 182 1 08 03010 01 1000 110 | |||

| in proceedings before the Supreme Court of the Russian Federation | 182 1 08 03020 01 1000 110 | |||

| for state registration: – organizations; - entrepreneurs; - changes made to founding documents; – liquidation of the organization and other legally significant actions |

182 1 08 07010 01 1000 110 4 | |||

| for accreditation of branches, representative offices of foreign organizations established in Russia | 182 1 08 07200 01 0040 110 | |||

| for state registration of rights, restrictions on rights to real estate and transactions with it - sale, lease and others | 321 1 08 07020 01 1000 110 4 | |||

| for the right to use the names "Russia", "Russian Federation" and words and phrases formed on their basis in the names of organizations | 182 1 08 07030 01 1000 110 | |||

| for the performance of actions related to licensing, with the certification provided for by the legislation of the Russian Federation, credited to the federal budget | 000 5 1 08 07081 01 1000 110 | |||

| for registration Vehicle and other legally significant actions related to changes and issuance of documents for vehicles, registration plates, driver's licenses | 188 1 08 07141 01 1000 110 | |||

| for conducting state technical inspection, registration of tractors, self-propelled and other machines and for issuing tractor driver certificates | 000 5 1 08 07142 01 1000 110 | |||

| for consideration of applications for concluding or amending the pricing agreement | 182 1 08 07320 01 1000 110 | |||

| for obtaining information from the Unified State Register of Legal Entities and the EGRIP (including for urgent receipt) | 182 1 13 01020 01 6000 130 4 | |||

| for actions related to the acquisition of citizenship of the Russian Federation (when applying through the MFC) | 188 1 08 06000 01 8003 110 | |||

| for state registration of mass media or making changes to the registration record, the products of which are intended for the territory of a constituent entity of the Russian Federation or a municipality (payment amount) | 096 1 08 07130 01 1000 110 | |||

| for state registration of mass media or making changes to the registration record, the products of which are intended for the territory of a constituent entity of the Russian Federation or a municipality (other revenues) | 096 1 08 07130 01 4000 110 | |||

| for state registration of mass media or making changes to the registration record, the products of which are intended for the territory of a constituent entity of the Russian Federation or a municipality (payment of interest on the amount of overcharged payments) | 096 1 08 07130 01 5000 110 | |||

Payments for the use of subsoil |

||||

| regular (rentals) for the use of subsoil on the territory of the Russian Federation | 182 1 12 02030 01 1000 120 | – | 182 1 12 02030 01 3000 120 | |

| regular (rentals) for the use of subsoil on the continental shelf, in the exclusive economic zone of the Russian Federation or in territories under the jurisdiction of the Russian Federation | 182 1 12 02080 01 1000 120 | – | 182 1 12 02080 01 3000 120 | |

| regular (royalties) when fulfilling production sharing agreements - combustible natural gas | 182 1 07 02010 01 1000 110 | 182 1 07 02010 01 2100 110 | 182 1 07 02010 01 3000 110 | |

| regular (royalties) when fulfilling production sharing agreements - hydrocarbon raw materials. In addition to combustible natural gas | 182 1 07 02020 01 1000 110 | 182 1 07 02020 01 2100 110 | 182 1 07 02020 01 3000 110 | |

| regular (royalties) for the extraction of minerals on the continental shelf or the exclusive economic zone of the Russian Federation or outside it in the performance of production sharing agreements | 182 1 07 02030 01 1000 110 | 182 1 07 02030 01 2100 110 | 182 1 07 02030 01 3000 110 | |

| one-time | 049 1 12 02060 01 0000 120 | – | – | |

Payments for the use of natural resources |

||||

| Payment Description | CCC for payment transfer | |||

| for air emissions from stationary facilities | 048 1 12 01010 01 6000 120

048 1 12 01010 01 7000 120 (if the payment administrator is a federal government agency) |

|||

| for emissions into the atmosphere by mobile objects | 048 1 12 01020 01 6000 120

048 1 12 01020 01 7000 120 (if the payment administrator is a federal government institution) |

|||

| for emissions into water bodies | 048 1 12 01030 01 6000 120

048 1 12 01030 01 7000 120 (if the payment administrator is a federal government institution) |

|||

| for the disposal of production and consumption waste | 048 1 12 01040 01 6000 120

048 1 12 01040 01 7000 120 (if the payment administrator is a federal government agency) |

|||

| for other types of negative impact on environment | 048 1 12 01050 01 6000 120

048 1 12 01050 01 7000 120 (if the payment administrator is a federal government institution) |

|||

| for the use of aquatic biological resources under intergovernmental agreements | 076 1 12 03000 01 6000 120

076 1 12 03000 01 7000 120 (if the payment administrator is a federal government agency) |

|||

| for the use of water bodies in federal ownership | 052 1 12 05010 01 6000 120

052 1 12 05010 01 7000 120 (if the payment administrator is a federal government agency) |

|||

| for the provision of a fishing area from the winner of the tender for the right to conclude such an agreement | 076 1 12 06010 01 6000 120

076 1 12 06010 01 7000 120 (if the payment administrator is a federal government institution) |

|||

| for the provision of a fish-breeding site for use from the winner of the auction (competitions, auctions) for the right to conclude such an agreement | 076 1 12 06030 01 6000 120

076 1 12 06030 01 7000 120 (if the payment administrator is a federal government agency) |

|||

| for granting the right to conclude an agreement on fixing shares of quotas for the extraction (catch) of aquatic biological resources or an agreement on the use of aquatic biological resources in federal ownership | 076 1 12 07010 01 6000 120

076 1 12 07010 01 7000 120 (if the payment administrator is a federal government agency) |

|||

Sanctions |

||||

| for violations of the legislation on taxes and fees provided for in Articles 116, 119.1, 119.2, paragraphs 1 and 2 of Article 120, Articles 125, 126, 126.1, 128, 129, 129.1, 129.4, 132, 133, 134, 135, 135.1, 135.2 tax code RF | 182 1 16 03010 01 6000 140 | |||

| for violations of the legislation on taxes and fees, provided for in Articles 129.3 and 129.4 of the Tax Code of the Russian Federation | 182 1 16 90010 01 6000 140 | |||

| for violation of the procedure for registering gambling business objects, provided for in Article 129.2 of the Tax Code of the Russian Federation | 182 1 16 03020 02 6000 140 | |||

| per administrative offenses in the field of taxes and fees, provided for by the Code of the Russian Federation on Administrative Offenses | 182 1 16 03030 01 6000 140 | |||

| for violating the order of application of the CCP. For example, for violation of the rules for the maintenance of cash registers | 182 1 16 06000 01 6000 140 | |||

| capitalized payments to the FSS of Russia upon liquidation in accordance with the Law of July 24, 1998 No. 125-FZ | 393 1 17 04000 01 6000 180 | |||

| for administrative offenses in the field of state regulation of the production and circulation of ethyl alcohol, alcohol, alcohol-containing and tobacco products | 141 1 16 08000 01 6000 140 (if the payment administrator is Rospotrebnadzor) 160 1 16 08010 01 6000 140 (if the payment administrator is Rosalkogolregulirovanie) 188 1 16 08000 01 6000 140 (if the payment administrator is the Ministry of Internal Affairs of Russia) |

|||

| for violation of the procedure for working with cash, maintaining cash transactions and failure to fulfill obligations to monitor compliance with the rules for conducting cash transactions | 182 1 16 31000 01 6000 140 | |||

| for violation of the legislation on state registration legal entities and individual entrepreneurs, provided for in Article 14.25 of the Code of the Russian Federation on Administrative Offenses | 182 1 16 36000 01 6000 140 | |||

| for evading the execution of an administrative penalty, provided for in Article 20.25 of the Code of the Russian Federation on Administrative Offenses | 182 1 16 43000 01 6000 140 | |||

Bankruptcy |

||||

| Receipts of capitalized payments of organizations in case of bankruptcy | 182 1 17 04100 01 6000 180 | |||

BCC for the transfer of debts for previous years

| Payment Description | CBC for tax transfer (fee, other mandatory payment) | CBC for the transfer of interest on tax (collection, other mandatory payment) | CSC for the transfer of a tax penalty (collection, other mandatory payment) |

Single tax with simplification for periods expired before January 1, 2016 |

|||

| minimum tax | 182 1 05 01050 01 1000 110 | 182 1 05 01050 01 2100 110 | 182 1 05 01050 01 3000 110 |

Taxes and fees in the Republic of Crimea and the city of Sevastopol |

|||

| debts on taxes, fees and other obligatory payments, formed before the organization was re-registered according to Russian legislation credited to the budget of the Republic of Crimea | 182 1 09 90010 02 1000 110 | 182 1 09 90010 02 2100 110 | 182 1 09 90010 02 3000 110 |

| debt on taxes, dues and other obligatory payments, formed before the organization was re-registered under Russian law, credited to the budget of the city of Sevastopol | 182 1 09 90020 02 1000 110 | 182 1 09 90020 02 2100 110 | 182 1 09 90020 02 3000 110 |

| debt on taxes, fees and other obligatory payments formed after the organization was re-registered under Russian law, credited to the budget of the Republic of Crimea | 182 1 09 90030 02 1000 110 | 182 1 09 90030 02 2100 110 | 182 1 09 90030 02 3000 110 |

| debt on taxes, dues and other obligatory payments formed after the organization was re-registered under Russian law, credited to the budget of the city of Sevastopol | 182 1 09 90040 02 1000 110 | 182 1 09 90040 02 2100 110 | 182 1 09 90040 02 3000 110 |

Insurance premiums for periods up to 2017 paid in 2018 |

|||

| for an insurance pension for periods up to January 1, 2017 (for example, in 2018 we pay for 2016) | 182 1 02 02010 06 1000 160 | 182 1 02 02010 06 2100 160 | 182 1 02 02010 06 3000 160 |

| in a fixed amount for an insurance pension (from income not more than limit value) for periods up to January 1, 2017 (for example, in 2018 we pay for 2016) | 182 1 02 02140 06 1100 160 | 182 1 02 02140 06 2100 160 | 182 1 02 02140 06 3000 160 |

| in a fixed amount for an insurance pension (from income above the limit) for periods up to January 1, 2017 (for example, in 2018 we pay for 2016) | 182 1 02 02140 06 1200 160 | 182 1 02 02140 06 2100 160 | 182 1 02 02140 06 3000 160 |

| for the insurance part of the labor pension at an additional rate for employees on list 1 (for example, in 2018 we pay for 2016) | 182 1 02 02131 06 1010 160 if the tariff does not depend on the special assessment; 182 1 02 02131 06 1020 160 if the tariff depends on the special valuation |

182 1 02 02131 06 2100 160 | 182 1 02 02131 06 3000 160 |

| for the insurance part of the labor pension at an additional rate for employees under list 2 (for example, in 2018 we pay for 2016) | 182 1 02 02132 06 1010 160, if the tariff does not depend on the special assessment; 182 1 02 02132 06 1020 160 if the tariff depends on the special valuation |

182 1 02 02132 06 2100 160 | 182 1 02 02132 06 3000 160 |

| in case of temporary disability and in connection with motherhood for periods before January 1, 2017 (for example, in 2018 we pay for 2016) | 182 1 02 02090 07 1000 160 | 182 1 02 02090 07 2100 160 | 182 1 02 02090 07 3000 160 |

| in FFOMS for periods up to January 1, 2017 (for example, in 2018 we pay for 2016) | 182 1 02 02101 08 1011 160 | 182 1 02 02101 08 2011 160 | 182 1 02 02101 08 3011 160 |

| in the FFOMS in a fixed amount for periods up to January 1, 2017 (for example, in 2018 we pay for 2016) | 182 1 02 02103 08 1011 160 | 182 1 02 02103 08 2011 160 | 182 1 02 02103 08 3011 160 |

BSC is a budget classification code. KBK codes for various taxes, including for 3-personal income tax, can be found on the official website of the Federal Tax Service of Russia.

Method number 1. How to find out the BCC tax on the site nalog.ru

A list of CSC codes can be found in the "Individual income tax" section or directly via the link https://www.nalog.ru/rn01/taxation/kbk/fl/ndfl/.

Method number 2. How to find out the CCC tax using an online service

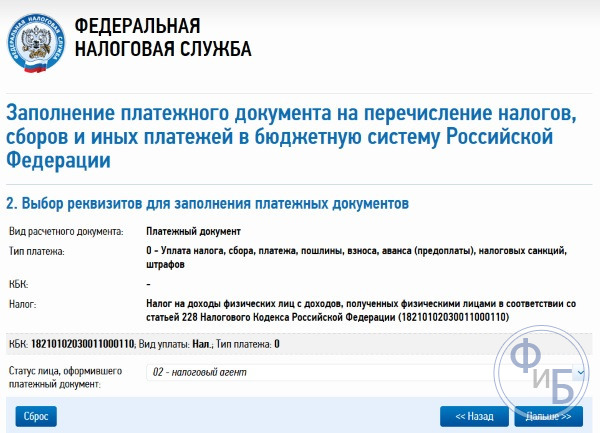

The KBK code can be found using the service https://service.nalog.ru/ This special service was developed on the nalog.ru website, with which you can generate and print a receipt for tax payment. Since now it is necessary to indicate the KBK in tax receipts, using this service you can not only prepare a receipt, but also find out the KBK code, as well as the IFTS code and OKTMO code of the tax office you are interested in.

On the first page of the service, you will be prompted to enter information about the type of payer and the type of payment document. Then click the "Next" button.

The payer can be an individual, an individual entrepreneur, the head of a peasant farm or an individual engaged in private practice or a legal entity. The payment document can be used for cash payments when printed and submitted to the bank or for non-cash payments by electronic payment. The payment order can only be used for non-cash payments when it is printed out and submitted to the bank.

Next, you need to select the type of payment. Since we do not know the CCC, and just want to know it, we do not fill in this field, but first select the type and name of the payment, and then, if necessary, specify the type of payment. After that, the BCC will appear in the corresponding field automatically.

If the task is only to find out the KBK code, then, as can be seen from the figure above, we have learned it. If there is a need to fill out a receipt, then you need to continue. As a result, you will be able to print a receipt for cash payment at the bank or immediately pay the tax in a non-cash way through various electronic services.

Classification codes of the Federal Tax Service in 2018 for personal income tax (PIT)

182 1 01 02030 01 1000 110Personal income tax on income received by individuals in accordance with Article 228 of the Tax Code of the Russian Federation (payment amount (recalculations, arrears and debts on the corresponding payment, including the canceled one)

182 1 01 02030 01 2100 110Personal income tax on income received by individuals in accordance with Article 228 of the Tax Code of the Russian Federation (penalty interest on the relevant payment)

182 1 01 02030 01 2200 110Personal income tax on income received by individuals in accordance with Article 228 of the Tax Code of the Russian Federation (interest on the relevant payment)

182 1 01 02030 01 3000 110Personal income tax on income received by individuals in accordance with Article 228 of the Tax Code of the Russian Federation (the amount of monetary penalties (fines) for the relevant payment in accordance with the legislation of the Russian Federation)

182 1 01 02040 01 1000 110Personal income tax in the form of fixed advance payments on income received by individuals who are foreign citizens employed on the basis of a patent in accordance with Article 2271 of the Tax Code of the Russian Federation (amount of payment (recalculations, arrears and arrears on the corresponding payment, including canceled)

182 1 01 02040 01 2100 110Personal income tax in the form of fixed advance payments from income received by individuals who are foreign citizens engaged in employment based on a patent in accordance with Article 2271 of the Tax Code of the Russian Federation (penalty interest on the relevant payment)

182 1 01 02040 01 2200 110Personal income tax in the form of fixed advance payments from income received by individuals who are foreign citizens engaged in employment based on a patent in accordance with Article 2271 of the Tax Code of the Russian Federation (interest on the corresponding payment)

182 1 01 02040 01 3000 110Tax on personal income in the form of fixed advance payments from income received by individuals who are foreign citizens engaged in employment on the basis of a patent in accordance with Article 2271 of the Tax Code of the Russian Federation (the amount of monetary penalties (fines) for the relevant payment in accordance with the law Russian Federation)

BCC change in 2019

Despite the fact that the BCC-2019 was approved by a new document, the CCC on basic taxes and contributions remained unchanged, that is, the same as in 2018. In this regard, bring BSC changes in 2019 in comparative table it just doesn't make sense. But in the tables below you will find the CBCs that will be valid in 2019.

KBK-2019

BCC for paying taxes for organizations and individual entrepreneurs on DOS

CBC for paying taxes for organizations and individual entrepreneurs on special regimes

BCC for insurance premiums

| View insurance premium | KBK |

|---|---|

| Insurance premiums for OPS | 182 1 02 02010 06 1010 160 |

| Insurance premiums for VNiM | 182 1 02 02090 07 1010 160 |

| Insurance premiums for CHI | 182 1 02 02101 08 1013 160 |

| Insurance premiums for OPS in a fixed amount(incl. 1% contributions) | 182 1 02 02140 06 1110 160 |

| Insurance premiums for CHI in a fixed amount | 182 1 02 02103 08 1013 160 |

| 182 1 02 02131 06 1010 160 |

| 182 1 02 02131 06 1020 160 |

| 182 1 02 02132 06 1010 160 |

| 182 1 02 02132 06 1020 160 |

| Injury insurance premiums | 393 1 02 02050 07 1000 160 |

CBC for payment of other taxes for all organizations and individual entrepreneurs

| Name of tax, fee, payment | KBK |

|---|---|

| Personal income tax on income, the source of which is a tax agent | 182 1 01 02010 01 1000 110 |

| VAT (as tax agent) | 182 1 03 01000 01 1000 110 |

| VAT on imports from Belarus and Kazakhstan | 182 1 04 01000 01 1000 110 |

| Income tax on payment of dividends: | |

| 182 1 01 01040 01 1000 110 |

| 182 1 01 01050 01 1000 110 |

| Income tax upon payment of income to foreign organizations (except for dividends and interest on state and municipal securities) | 182 1 01 01030 01 1000 110 |

| Income tax on income from state and municipal securities | 182 1 01 01070 01 1000 110 |

| Income tax on dividends received from foreign organizations | 182 1 01 01060 01 1000 110 |

| Transport tax | 182 1 06 04011 02 1000 110 |

| Land tax | 182 1 06 0603x xx 1000 110 where xxx depends on the location of the land |

| Fee for the use of aquatic biological resources: | |

| 182 1 07 04030 01 1000 110 |

| 182 1 07 04020 01 1000 110 |

| water tax | 182 1 07 03000 01 1000 110 |

| Payment for negative environmental impact | 048 1 12 010х0 01 6000 120 where x depends on the type of environmental pollution |

| Regular payments for the use of subsoil, which are used: | |

| 182 1 12 02030 01 1000 120 |

| 182 1 12 02080 01 1000 120 |

| NDPI | 182 1 07 010xx 01 1000 110 where хх depends on the type of extracted mineral |

| Corporate income tax on income in the form of profits of controlled foreign companies | 182 1 01 01080 01 1000 110 |

CBC for the payment of penalties

By general rule when paying a fine in the 14th-17th category, they take the value "2100". However, there is an exception to this rule:

| Type of insurance premium | KBK |

|---|---|

| Insurance premiums for OPS | 182 1 02 02010 06 2110 160 |

| Insurance premiums for VNiM | 182 1 02 02090 07 2110 160 |

| Insurance premiums for CHI | 182 1 02 02101 08 2013 160 |

| (incl. 1% contributions) | 182 1 02 02140 06 2110 160 |

| 182 1 02 02103 08 2013 160 | |

| Additional insurance premiums for compulsory pension insurance for employees* who work in conditions that give the right to early retirement, including: | |

| 182 1 02 02131 06 2110 160 |

| 182 1 02 02132 06 2110 160 |

CBC for payment of fines

When paying a fine, as a rule, the 14th-17th digits take on the value "3000". But here we should not forget about exceptional cases:

| Type of insurance premium | KBK |

|---|---|

| Insurance premiums for OPS | 182 1 02 02010 06 3010 160 |

| Insurance premiums for VNiM | 182 1 02 02090 07 3010 160 |

| Insurance premiums for CHI | 182 1 02 02101 08 3013 160 |

| Insurance premiums for OPS in a fixed amount paid by individual entrepreneurs for themselves(incl. 1% contributions) | 182 1 02 02140 06 3010 160 |

| Insurance premiums for CHI in a fixed amount paid by individual entrepreneurs for themselves | 182 1 02 02103 08 3013 160 |

| Additional insurance premiums for compulsory pension insurance for employees who work in conditions that give the right to early retirement, including: | |

|

How to find out the budget classification code is a topical issue, primarily because budget codes are used very often. They are needed when preparing tax returns, paying state duties, taxes, fines, contributions, etc. Recall that each payer must indicate the CCC in payment receipts to pay off their payment obligations to the state, since this code indicates the type of payment being made and its recipient. In the declarations, it is needed for the further correct processing of your documents by the tax service.

In addition, budget codes are needed for the accurate and uninterrupted functioning of the budget system. The financial flows of revenues and expenditures of the state budget are huge. Therefore, all types of cash receipts and their spending in state budgets of various levels are encoded using a special classifier BCC, which is annually approved by the Ministry of Finance of the Russian Federation. The classification of sections and subsections of the KBK reference book is uniform throughout the Russian Federation.

The coding structure provides maximum detail and specification of budget revenue and expenditure items.

Despite the rather large number of codes used, the general classifier is written in such a way that it is easy to navigate in it. Thanks to the well-thought-out structure of the classifier sections, it is quite easy to find the right code for each specific case.

Although the BCC has a twenty-digit numerical designation, we still note that it is quite possible to understand the meaning and purpose of its parts, and therefore learn how to correctly apply budget codes.

Today we will try to understand the structure of such codes, how they are used and where to find them.

BCC is a twenty-digit code, the numbers of which indicate the type and purpose of the payment. These codes are used to account for the receipt of income and the correct functioning of each expenditure item of the budget at various levels.

On a national scale, targeted cash flows are very large, so such codings have been introduced to ensure their identification, transparency and control. The classifier provides maximum specification of budget items.

Commercial organizations and individual entrepreneurs, individuals, usually use that part of the classifier that contains the coding of sections devoted to budget revenues. Since, all payments paid by business entities and individuals are transferred to the income of budgets of various levels.

The Tax Service keeps records of cash receipts from taxpayers in full accordance with the current classifier.

Therefore, when paying current payments to taxpayers, legal entities and individuals, you must also strictly observe the correctness of the CBC encodings, in order to avoid that your payments do not reach the desired “addressee”, and the tax debt will remain with you. Recall that in case of non-payment of tax debts on time, penalties will be charged and fines will be issued.

In addition, the CSC ensure the targeting of budget revenues and targeted spending of state budget funds.

CBC also take into account the fact that some taxes are distributed to the federal budget, some - to the territorial budgets of the constituent entities of the Russian Federation, others go to local municipal budgets. There are also taxes that go to the budgets of all three levels at once, since their volumes are the most significant. This applies to corporate income tax and VAT. Moreover, the percentages distributed among the budgets differ depending on the region of our country. And exactly CSC codes, ensure the accuracy and transparency of cash flow.

We also note that almost every year some changes are made to the CSC classifier, codes may be excluded, and new codes may be added. This is due to the constant updating of budget items, the emergence of new areas of economic activity and the development of the state as a whole.

Therefore, periodically you need to refer to the current classifier to recheck the CSC.

The current version of the classifier can always be viewed and downloaded on the official website of the IFTS.

The main meaning of the CBC structure:

- payment source designation

- payment form designation

- designation of the recipient of payment

- designation of the item of expenditure of funds from the state budget.

The very structure of the twenty-digit CBC consists of several parts:

- The first three digits of the CSC code indicate the recipient of funds, who controls the timeliness and is responsible for the receipt of funds to his settlement accounts. These recipients are: tax office, off-budget funds, municipalities, etc.

- The fourth digit of the code - indicates the type of income, i.e. payment of taxes, various fees, state duties, etc.

- . The fifth and sixth digits of the CCC - indicate the code of the tax or fee. For example, code 01 is income tax, 02 is social security fees, 03 is VAT on goods and services on Russian territory, 05 - UTII, etc.

- The seventh and eighth digits of the CSC are tax items, the ninth to eleventh digits are tax sub-items.

- The ranks of the CSC from the twelfth to the thirteenth - denote regional or local state budget recipients.

- So, if the funds are sent to the federal budget - code 01, to the budget of the territorial subject of the Russian Federation - 02, to the local municipal budget- code 03, and if, for example, to the Pension Fund - then code 06.

- Under the fourteenth number of the CSC - the type of receipt of funds is indicated, so taxes - 1, penalties - 2, fines - 3.

- The fifteenth and sixteenth digits are always 0.

- The last three digits of the BCC are the classification of items of state income: tax income- code 110, compulsory collections - code 140, etc.

- Before transferring funds to taxes and fees, it is always better to check the current classifier and select the correct code from it. CSC classifiers are periodically updated, in 2017 the classifier that was in 2016 will be valid. Up-to-date information can be obtained on the website of the tax inspectorate, where CBC are indicated in sections for legal entities, individuals and individual entrepreneurs.

Main Functions of CSC Codes

As noted above, the CSC classifier is primarily needed to streamline the receipt of funds in the state budget and control their spending.

Its other most important function is that with the help of the CBC, the primary grouping of funds occurs, upon receipt from taxes, insurance premiums, etc., and their further redistribution.

CBC also perform a number of other important functions:

- are used for drawing up budgets of various levels;

- execution and control of various budgets;

- with their help comparability of necessary indicators is provided.

With the help of cash flow coding, it is easy to collect statistical information about financial flows at all levels of the economy. Thus, the codes serve as a tool for collecting and analyzing data on financial flows throughout our country. These codes allow you to see how money transfers for taxes and other obligatory payments from a particular business entity or just an individual enter the state treasury. Then, using the coding, the consumption of the funds received is also controlled.

CBC must be affixed to the following documents:

- on payment documents, when transferring taxes, penalties, fines, state duties, etc.

- on tax returns

- when compiling tax reporting

- other documents providing for the indication of targeted budget items.

It is important to note that only one BCC is always indicated in payment documents. If you need to make several payments - fill in several payment documents.

You probably already had to fill out tax returns containing BCC: declarations for personal income tax, VAT, income tax, transport tax, insurance premium calculations, etc.

How to determine the budget classification code

Let's figure out how to determine the number of the required tax payment according to the budget classification directory.

In order to find out the required CSC in this particular case, it is most convenient to go to the official website of the Federal Tax Service:

- We open the IFTS website nalog.ru

- Select the tab "Taxation in the Russian Federation"

- The page “Classification codes for revenues of budgets of the Russian Federation administered by the Federal Tax Service” will open.

- We select one of the sections we need "Legal entity", "Individual" or "IP"

- Next, a list of transfers of taxes, fines, etc. will open, select the item we need, and then the sub-item of our payment.

- In the table that opens, select the twenty-digit BCC we need, based on its description.

As you can see, finding KBK on the Internet is quite simple. For the convenience of users, the IFTS website provides a meaningful transition to the links with the selection of the desired section. So it's easy to navigate there.

You can also use the usual paper reference books, if you prefer. You can use other information resources. The main thing is that you use the latest up-to-date data.

Let's look at a few common cases.

Let's analyze the example of the BCC when paying tax by vehicle owners - 182 1 05 04012 03 1000 010.

As noted earlier, the CSC has several informative blocks:

- administrative;

- profitable;

- program;

- classifying.

Administrative block- the first three digits "182" designate the funds administrator. In other words, the purpose of the payment is a tax collection.

Income block- it contains several subsections of information:

- view - tax "1"

- income subgroup - tax on total income "05"

- article - target deduction "04"

- subentry - "012"

- income budget - local budget"03"

Program block- payment type of four digits - taxes and fees "1000"

classifying block- the last three digits indicate the type of economic activity - tax income "010".

As you can see, the CSC has a rather complex structure, which is due to the various areas and types of activities of organizations, the territorial division of our big country, various legal forms business entities. When specifying codes, it is important to use the latest current version of the KBK directory so that when filling out payment documents, you do not accidentally send your payment to a “no longer existing address”. And again, despite the complexity of the CSC structure, the directory allows users to easily select the CSC they need in a given situation.

Paying income tax is also a very common situation.

Personal income tax is one of the most capacious articles of the budget revenue, we will analyze it in more detail. BCC for filling out the payment in this case - 182 1 01 02010 01 1000 110.

Consider a detailed decoding of the CSC:

- tax administrator - budget "182"

- type of payment - tax "1"

- purpose of payment - personal income tax "01"

- article -"02"

- subentry - "010"

- payment type - taxes and fees "1000"

- tax receipt - "110".

CBC for entrepreneurs on the simplified tax system:

Considering the changes that took place in 2016, for entrepreneurs using the simplified taxation system, the CBC for transferring tax payments the following:

- for tax regime“income only”, 6% of income is paid, CBC - 182 1 05 01011 01 1000 110.

- for the tax regime "income minus expenses" the tax rate is 15%, BCC - 182 1 05 01021 01 1000 110.

- for mode minimum tax on the "simplified" KBK - 182 1 05 01050 01 1000 110.

Well, we've covered a few of the most common cases. We hope that now the use of the budget encoding has become clearer.

Understanding the structure of the CCC will help you independently determine the purpose of the payment and avoid inaccuracies when filling out tax returns and various reports, as well as in compiling payment documents. Errors or inaccuracies in the instructions of the CCC lead to the transfer of funds "to the wrong address." Note that the process of returning funds from the relevant budget is very lengthy and often requires a lot of effort.

Conclusion

To ensure the controllability and transparency of the movement of funds on settlement accounts of state budgets of all levels in Russia, a special system coding. The decoding of codes is contained in a special classifier of budget encodings. It indicates all types of cash receipts to the state budgets of all levels of government: federal, territorial and local. These codes designate all characteristics of payments of business entities and individuals. They indicate the type of tax or fee transferred, penalties, fines, state duty, contributions to various funds social insurance etc.

BCC must always be correctly indicated in payment documents, transferring your payments to the state budget. Be sure to CBC must also be indicated when filling out the relevant tax returns for their correct processing in the Federal Tax Service.

To facilitate the completion of tax receipts for individuals, the tax office usually sends taxpayers individual receipts, where everything necessary details already filled. And legal entities and individual entrepreneurs must often choose the CBC themselves, and it is important to be able to do this correctly. After all, correctly completed tax returns and payment documents are a guarantee of fulfillment tax liabilities on time, without misunderstandings and fines. Note that in the event of a dispute, the law will be on the side of the tax authorities.

When specifying CSC codes, it is important to use the latest current version of the CSC classifier, since it changes quite often and is constantly updated with new sections, due to ongoing changes in the economy of the state as a whole.

So we examined the essence, structure and purpose of budget codes. Despite their apparent bulkiness, they are quite convenient to use. They are intended mainly to provide a systematic and accurate processing of information on financial flows in all state structures. This coding system ensures uninterrupted and targeted execution of all budget payments made. It is also used by all payers of state payments, whether it be taxes, fines, state duties and much more.

For employees

CBC for paying personal income tax for employees

CBC for paying personal income tax penalties for employees

CBC for payment of personal income tax for individual entrepreneurs

CBC for payment of interest on personal income tax for individual entrepreneurs

For individuals

CBC for payment of personal income tax for individuals

CBC for payment of interest on personal income tax for individuals

With dividends and working under a patent

CBC for the payment of personal income tax from dividends

CBC for the payment of personal income tax for citizens working on the basis of a patent

FILES

Some clarifications on the BCC for income tax

Personal income tax is calculated by subtracting from the amount of income of individuals documented confirmed expenses and taking a certain percentage of this value (tax rate). Separately, personal income tax is charged to residents and non-residents of the Russian Federation, but this does not apply to employees. Some of the income listed in legislative act, are not subject to taxation (for example, inheritance, sale of real estate older than 3 years, gifts from close relatives, etc.) Declaration of income entitles individuals to certain tax deductions.

In a situation where income is salary, the state takes the tax from it not from the employee after accrual, but from tax agent- an employer who will give the employee a salary with taxes already deducted to the budget.

personal income tax on employee income

Paid by the tax agent monthly on the day of salary, maximum the next day. In the case of payment of sick leave and vacation benefits, the tax is transferred by the tax agent no later than the end of the month of their payment. It does not matter who the tax agent is - a legal entity or an individual, an LLC or an individual entrepreneur.

Vacation payments are also subject to personal income tax, because this is the same wage only for the rest period. The tax must be paid before the end of the month in which the employee received his vacation pay.

NOTE! No income tax is charged on the advance. An employer is prohibited from paying personal income tax from its own funds.

How is VAT calculated

All taxes are calculated using the formula: tax base multiplied by the tax rate. The differences are what is taken as the base, and what is the interest rate.

For personal income tax, it matters whether employee Russian resident or not. If during the year he stayed in the country for more than 182 days, then personal income tax will be charged at the resident rate - 13%. Non-residents have to pay at a rate almost three times higher - they have an indicator of 30%.

Current CSCs

CBC for tax transferred by a tax agent - 182 1 01 02010 01 1000 110.

If there is a delay, you will have to pay interest on BCC 182 1 01 02010 01 2100 110.

The imposed fine must be paid according to the BCC 182 1 01 02010 01 3000 110.

Interest on this type of personal income tax is paid according to BCC 182 1 01 02010 01 2200 110.

income tax on dividends

If an individual makes a profit from participation in organizations, it is necessary to pay tax on it, which will be withheld by the tax agent (organization). An individual will transfer personal income tax independently if, being a resident of the Russian Federation, he receives dividends from abroad.

CBC when deducted by a tax agent will be the same as for salary personal income tax: 182 1 01 02010 01 1000 110.

An individual must use BCC 182 1 01 02030 01 1000 110 for this purpose.

Some CBCs indicated by entrepreneurs when transferring taxes and insurance premiums are the same for all individual entrepreneurs, regardless of the applicable taxation regime. And some budget classification codes are “intended” for a specific regime.

CCC: IP-2019 contributions

CBCs for insurance premiums represent the largest group of codes that are necessary for entrepreneurs of absolutely all taxation regimes.

Individual entrepreneurs, when filling out payments for insurance premiums in 2019, must indicate the following BCC:

| Contribution type | KBK |

|---|---|

| Insurance premiums for OPS | 182 1 02 02010 06 1010 160 |

| Insurance premiums for CHI | 182 1 02 02101 08 1013 160 |

| Insurance premiums for VNiM | 182 1 02 02090 07 1010 160 |

| Injury insurance premiums | 393 1 02 02050 07 1000 160 |

| Additional insurance premiums for compulsory pension insurance for employees who work in conditions that give the right to early retirement, including: | |

| 182 1 02 02131 06 1010 160 | |

| 182 1 02 02131 06 1020 160 | |

| ) (additional tariff does not depend on the results of the special assessment) | 182 1 02 02132 06 1010 160 |

| - for those employed in work with difficult working conditions (paragraphs 2-18, part 1, article 30 federal law dated December 28, 2013 No. 400-FZ) (additional tariff depends on the results of the special assessment) | 182 1 02 02132 06 1020 160 |

KBC: IP contributions for yourself

BCCs for IP contributions for themselves are also the same for everyone, regardless of the applied regime.

BCC for IP on DOS in 2019

General business entrepreneurs are payers of personal income tax in terms of their income and VAT payers:

BCC for individual entrepreneurs in special modes in 2019

Each special regime tax has its own CSC.

). In our tables you will find all the budget classification codes necessary for the correct filling of payments in 2017. Codes that have changed since 2016, as well as new BCC-2017, are in italics and marked with an asterisk.

BCC-2017 for paying taxes for organizations and individual entrepreneurs on DOS

BCC-2017 for paying taxes for organizations and individual entrepreneurs on special regimes

Organizations and individual entrepreneurs on the simplified tax system need to pay attention to the fact that a separate CCC has been canceled for transferring the minimum tax. Since 2017, the minimum tax is credited to the same budget classification code as the STS tax paid in the usual way. Read about the consequences of indicating the old CBC in the payment when paying the minimum tax in the Civil Code, 2017, No. 1, p.63.

KBK: insurance premiums-2017

BCC for all contributions controlled by the Federal Tax Service since 2017 have become new.

Please note that for contributions for periods prior to 2017 there will be one CCF, and for contributions for periods starting in 2017 there will be others. That is, if, for example, you transfer contributions for December 2016 in January 2017, then they are paid to the CCC intended for contributions for periods that have expired before 2017.

CSC for contributions for periods expired before 01/01/2017

| Type of insurance premium | BCC (field 104 of the payment order) |

|---|---|

| 182 1 02 02010 06 1000 160* | |

| 182 1 02 02090 07 1000 160* | |

| 182 1 02 02101 08 1011 160* | |

| 182 1 02 02140 06 1100 160* | |

| (1% contributions) | 182 1 02 02140 06 1200 160* |

| 182 1 02 02103 08 1011 160* | |

| No. 400-FZ | 182 1 02 02131 06 1010 160* |

| - for those employed in jobs with harmful working conditions (clause 1, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ | 182 1 02 02131 06 1020 160* |

| No. 400-FZ) (additional tariff does not depend on the results of the special assessment) | 182 1 02 02132 06 1010 160* |

| 182 1 02 02132 06 1020 160* | |

| 393 1 02 02050 07 1000 160 |

CSC for contributions for periods starting from 01/01/2017

| Type of insurance premium | BCC (field 104 of the payment order) |

|---|---|

| 182 1 02 02010 06 1010 160* | |

| 182 1 02 02090 07 1010 160* | |

| 182 1 02 02101 08 1013 160* | |

| Insurance premiums for OPS in a fixed amount paid by individual entrepreneurs for themselves to the IFTS | 182 1 02 02140 06 1110 160* |

| 182 1 02 02103 08 1013 160* | |

| Additional insurance premiums for OPS for employees who work in conditions that give the right to early retirement, including (paid to the IFTS): | |

| - for those employed in jobs with harmful working conditions (clause 1, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ) (the additional tariff does not depend on the results of the special assessment) | 182 1 02 02131 06 1010 160* |

| - for those employed in jobs with harmful working conditions (clause 1, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ) (additional tariff depends on the results of the special assessment) | 182 1 02 02131 06 1020 160* |

| - for those employed in jobs with difficult working conditions (paragraphs 2-18, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ) (the additional tariff does not depend on the results of the special assessment) | 182 1 02 02132 06 1010 160* |

| - for those employed in jobs with difficult working conditions (clauses 2-18, part 1, article 30 of the Federal Law of December 28, 2013 No. 400-FZ) (additional tariff depends on the results of the special assessment) | 182 1 02 02132 06 1020 160* |

| Insurance premiums "for injuries" paid to the FSS | 393 1 02 02050 07 1000 160 |

BCC-2017 for the payment of other taxes for all organizations and individual entrepreneurs

| Name of tax, fee, payment | BCC (field 104 of the payment order) |

|---|---|

| Personal income tax on income, the source of which is a tax agent | 182 1 01 02010 01 1000 110 |

| VAT (as tax agent) | 182 1 03 01000 01 1000 110 |

| VAT on imports from the EAEU countries | 182 1 04 01000 01 1000 110 |

| Income tax on payment of dividends: | |

| - Russian organizations | 182 1 01 01040 01 1000 110 |

| - foreign organizations | 182 1 01 01050 01 1000 110 |

| Income tax upon payment of income to foreign organizations (except for dividends and interest on state and municipal securities) | 182 1 01 01030 01 1000 110 |

| Income tax on income from state and municipal securities | 182 1 01 01070 01 1000 110 |

| Income tax on dividends received from foreign organizations | 182 1 01 01060 01 1000 110 |

| Transport tax | 182 1 06 04011 02 1000 110 |

| Land tax | 182 1 06 0603x xx 1000 110 where xxx depends on the location of the land |

| Fee for the use of aquatic biological resources: | |

| - for inland water bodies | 182 1 07 04030 01 1000 110 |

| - for other water bodies | 182 1 07 04020 01 1000 110 |

| water tax | 182 1 07 03000 01 1000 110 |

| Payment for negative environmental impact | 048 1 12 010х0 01 6000 120 where x depends on the type of environmental pollution |

| Regular payments for the use of subsoil, which are used: | |

| - on the territory of the Russian Federation | 182 1 12 02030 01 1000 120 |

| - on the continental shelf of the Russian Federation, in the exclusive economic zone of the Russian Federation and outside the Russian Federation in territories under the jurisdiction of the Russian Federation | 182 1 12 02080 01 1000 120 |

| NDPI | 182 1 07 010xx 01 1000 110 where хх depends on the type of extracted mineral |

| Corporate income tax on income in the form of profits of controlled foreign companies | 182 1 01 01080 01 1000 110* |

Indication of the CBC when paying penalties and fines

As a general rule, when paying a fine in the 14-17th category of the CCC, they take the value "2100", and when paying a fine - "3000". However, when transferring penalties and fines for certain types of insurance premiums, this rule does not work:

| Type of insurance premium | CBC when paying a penalty | CBC when paying a fine |

|---|---|---|

| For contributions for periods expired before 01/01/2017 | ||

| Insurance premiums for CHI paid to the IFTS | 182 1 02 02101 08 2011 160 | 182 1 02 02101 08 3011 160 |

| Insurance premiums for CHI in a fixed amount paid by individual entrepreneurs for themselves to the Federal Tax Service | 182 1 02 02103 08 2011 160 | 182 1 02 02103 08 3011 160 |

| For contributions for periods starting from 01/01/2017 | ||

| Insurance premiums for OPS paid to the IFTS | 182 1 02 02010 06 2110 160 | 182 1 02 02010 06 3010 160 |

| Insurance premiums in case of temporary disability and in connection with motherhood, paid to the IFTS | 182 1 02 02090 07 2110 160 | 182 1 02 02090 07 3010 160 |

| Insurance premiums for CHI paid to the IFTS | 182 1 02 02101 08 2013 160 | 182 1 02 02101 08 3013 160 |

| Insurance premiums for OPS in a fixed amount paid by individual entrepreneurs for themselves to the IFTS | 182 1 02 02140 06 2110 160 | 182 1 02 02140 06 3010 160 |

| Insurance premiums for CHI in a fixed amount paid by individual entrepreneurs for themselves to the Federal Tax Service | 182 1 02 02103 08 2013 160 | 182 1 02 02103 08 3013 160 |

CBC for income tax in 2018-2019 are applied in 3 types: for the payment of tax, penalties and fines. Since 2018, new codes have been added to them. We will tell about the BCC for income tax in 2018-2019 in our material.

Income tax payers

All legal entities are the entities whose duties include the accrual and payment of tax on the resulting profit. The exception is enterprises on preferential taxation regimes, such as UTII, ESHN, STS, as well as organizations exempt from tax on the basis of paragraphs. 2 and 4 Art. 246 and Art. 246.1 of the Tax Code of the Russian Federation. The combination of taxation regimes, for example, OSNO and UTII, involves the calculation of tax only as part of the profit received on OSNO.

The tax rate is set for commercial organizations in the amount of 20%. The exception is some educational and medical institutions, agricultural institutions, participants in regional investment projects, etc. in accordance with Art. 284 of the Tax Code of the Russian Federation.

More information about tax rates see material "St. 284 of the Tax Code of the Russian Federation (2018): questions and answers” .

Tax payments must be made monthly or quarterly. The frequency of accruals depends on the total revenue of the organization or its status (Article 286 of the Tax Code of the Russian Federation).

For more information on tax calculation and frequency of payments, see the material "Advance income tax payments: who pays and how to calculate?".

The tax advance payment deadline is the next month after the reporting period, no later than the 28th. Final annual amount for income tax must be transferred to the budget no later than March 28.

On our forum, you can discuss any question that you have about the calculation and payment of certain taxes, as well as the formation of reports on them, including income tax. In, for example, we are discussing innovations in the calculation of income tax.

CCC of income tax in 2018-2019 for legal entities