Country resident. Tax resident of the Russian Federation: who is it

Formation tax base occurs only after the employees of the relevant structures find out who a resident and non-resident are, whether it is possible to change the status and how to do it. The volume of payments seriously depends on a person's belonging to one or another category. Therefore, having knowledge on this issue will not be superfluous even for an ordinary citizen.

Who is a resident in simple words?

Any person who is completely subject to the legislative system of any state is, from the point of view of the authorities, a resident.

The presence or absence of a resident status determines the set of rights an individual has:

- The right to vote in elections at various levels;

- The right to be elected;

- Free access to public services;

- Interest rate of mandatory payments.

IN Russian Federation The term is used mainly in the field of finance. According to federal law"ABOUT currency regulation and currency control, residents are considered:

- Citizens who have not left the country for at least a year;

- Labor migrants and other foreigners who have a document confirming the right to permanent residence in Russia;

- Companies founded in accordance with the letter of the law of Russia and their subsidiaries;

- Embassies and consulates of the country abroad;

- Regions of Russia and the federation itself as a single entity.

Among all the political films of the Soviet Union, Veniamin Dorman's series of four psychological dramas "Resident" stands apart. A captivating script and a wonderful play of actors ensured an unprecedented success for the film.

The tetralogy tells about the adventures of intelligence officer Mikhail Tuliev:

- In the first film, viewers are introduced to the figure of Tuliev, who is presented as a German spy who decided to take revenge on the Communists for his White Guard parents. Shpik is opposed by an experienced Chekist nicknamed Bekas, who easily bypasses the enemy;

- The second tape opens the hero Georgy Zhzhenov from a new side. He recognizes Russia in the USSR and goes over to the side of the former enemy;

- After the recruitment, Tuliev is sent back to the camp of the Germans, where he manages to get valuable information for the newly found homeland;

- The final film of the series tells about the realities of the Cold War. Someone by the name of Brikman is given the task of "removing" an eminent Soviet nuclear physicist. The already familiar descendant of the White Guards will oppose him.

What is a tax resident?

Any state is very scrupulous about the collection of mandatory payments from its citizens. In Russia, there are no such draconian penalties for non-payment as in the United States, but tax legislation in our country is given no less attention.

The cornerstone in the system of state fees is the concept of a resident, which is disclosed by law as follows:

- To obtain this status, it is necessary not to leave the territory of the Russian Federation for 183 days during the year;

- Traveling abroad for short trips (for several months) does not affect the current status in any way;

- In most cases, Russians are unaware of their position. Confirmation may be needed only in special situations. For example, to avoid the need to pay taxes to several states at once;

- Anyone who is in a resident position must answer to the state for income from activities both in Russia and in other countries;

- A non-resident, by contrast, does not have to account for overseas business. Thus, this rule of law is potentially corrupt. Through simple "tricks" with documents, former servants of the people can launder large capitals abroad.

In relation to the Comedy Club project

The most scandalous comedy show on Russian television has always been at odds with the Russian language. One name Comedy Club is worth something. But the founders decided not to stop there and introduced another tongue-tied word - resident. That is the name of those who entered into a long-term contract with the project and is actually a permanent participant in the performance.

The total number of "contract workers" exceeds 25 people, but the following names are widely known to the public:

- Garik Martirosyan- one of the founding fathers of the program. Differs in intelligence and ingenuity, and at the same time a penchant for lively improvisation;

- Pavel Volya- a nugget from Penza, a stand-up comedian who dreamed of conquering Moscow and realized his plan. By education, he is a teacher of the Russian language and literature, which cannot but affect the specifics of his speeches;

- Alexander Revva - acts as a brutal male Arthur Pirozhkov. Came to the program from KVN;

- Semyon Slepakov - responsible for musical numbers. His songs are known not only on TV, but also on the Internet;

- Vadim Galygin is a native of Belarus who left the ranks of Comedy, but returned to his native land a few years later.

Residents of which countries are eligible for deferred payment?

Yandex, like any other search engine, lives off income from contextual advertising. The interface through which advertisers can place their ad is called Direct.

Service features include:

- Evaluation of user requests based on open statistics;

- It is possible to choose those search phrases that you want to display with advertising;

- Writing a selling text;

- Geographical localization (subjects of the federation).

The service is constantly updated in order to meet the needs of customers as much as possible. So, in 2014, the possibility of deferred payment appeared. Now regular users of Direct, who donated at least 20,000 rubles to the system, can submit a request for the provision of a service for half a month before paying for it.

You can activate this function in the payment mechanism selection window. A form will open with a notification where you need to confirm agreement with the terms of the contract.

Residents can take advantage of the new functionality both Russia and Ukraine.

Representatives of different professions and ages can give completely unexpected answers to the question of who a non-resident and a resident are. Teenagers will outline the image of Garik Martirosyan. Pensioners will wipe away a nostalgic tear in their memories of the cult film by Veniamin Dorman. Tax authorities will take an interest in the duration of stay in the country.

Video: how to get a certificate of a resident of the Russian Federation

In this video, lawyer Leonid Orlov will tell you how to get a certificate from a Russian resident and why it may be needed:

- Accounts of legal entities

- Accounts of individuals

- Accounts (deposits) of non-residents

- Calculation of residency by example

- Sources and links

- Sources of texts, pictures and videos

- Links to internet services

- Links to application programs

- Article Creator

Expand content A resident and a non-resident is, definition A resident is an individual who has a permanent registration of the country, as well as permanently residing in this country, as applied Russian legislation, within 183 calendar days during the last 12 months, or it is a legal entity, or an organization that does not have the status of a legal entity, or a diplomatic or other official representative office established in accordance with the legislation of the Russian Federation, located on its territory or outside.

Legal entity in the Russian Federation: how to determine its status - resident or non-resident

For the correct calculation of taxes and the avoidance of double taxation, it is necessary to establish residency. Therefore, the question of how to determine whether a legal entity is a resident or non-resident in Russia in 2018 has an important practical meaning.

Content

- 1 Residency - what is it

- 2 What is the difference between tax statuses in the Russian Federation

- 2.1 Is it possible to determine residency by bank account number

- 2.2 Is it possible to determine residency by TIN

- 2.3 Will the CPT help determine tax status

- 2.4 How to find out the residence of a legal entity on the website of the Federal Tax Service of the Russian Federation

- 3 Types of legal entities - concept, functions, examples: Video

Residency - what it is In a broad sense, the residence of a legal entity is understood as its belonging to tax system a certain state, being registered and paying taxes.

Who is a resident and non-resident of the Russian Federation

Federal Tax Service of Russia dated May 25, 2011 No. AS-3-3/1855. Situation: how, when determining the tax status (resident or non-resident), for the purposes of calculating personal income tax, how to take into account the days spent on business trips and holidays abroad? When a person travels abroad, he leaves the territory of Russia. When determining the tax status (resident or non-resident), only the days of a person's actual stay in Russia are taken into account.

Attention

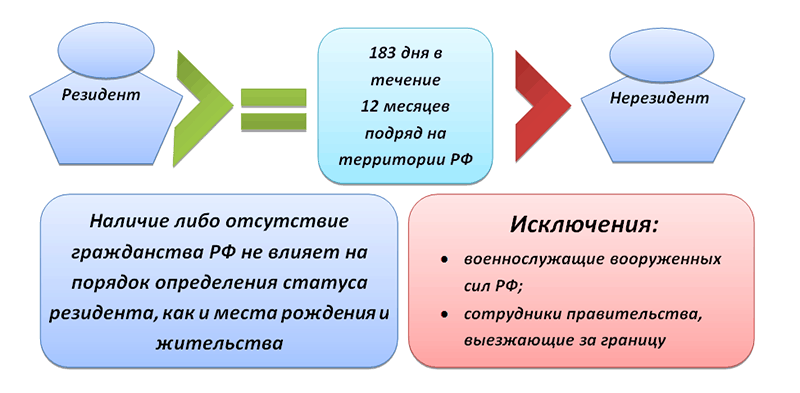

If during 12 consecutive months a person has been in Russia for 183 calendar days or more, he is recognized tax resident. If during 12 consecutive months a person has been in Russia for less than 183 calendar days, he is a non-resident.

This is stated in paragraph 2 of article 207 tax code RF. At the same time, the period of stay in Russia (less than or more than 183 days) includes both the day of arrival (entry) to Russia and the day of departure (departure) from it.

Resident and non-resident

Info

The Tax Code regulates various lists of taxable income depending on the residence status of a citizen. Read also the article: → "Payers of personal income tax in 2018: tax residents and non-residents."

Important

According to the current legislation, the right to a tax deduction is granted only to residents of the Russian Federation. Therefore, when assigning and calculating the amount of tax compensation, the employer must have comprehensive information about the residence status of the employee.

How to determine residency Contrary to popular belief, residency status does not directly depend on the presence or absence of a person's citizenship of the Russian Federation. That is, a citizen of another country and a stateless person (with dual citizenship) can be a resident of the Russian Federation, and vice versa, a citizen of the Russian Federation can have the status of a non-resident.

Criteria for establishing resident status Main criterion, allowing to establish the status of residence, - the period of stay of a person in the territory of the Russian Federation.

Resident and non-resident (resident and non-resident) is

So, a company that is foreign by code may turn out to be a resident of the Russian Federation. Therefore, the data must be additionally checked against other sources.

back to table of contents Will the CPT help determine the tax status of the CPT - an additional nine-digit code received by legal entities in tax office upon registration. This applies to both residents and non-residents of the Russian Federation. Its main purpose is to show the reason why this organization was registered with a certain tax office.

A legal entity may have several such checkpoints and they may change over time: for example, when changing the address. The first two digits of the checkpoint represent the region of the Russian Federation, the third and fourth - the number of the tax office.

How to determine a resident or non-resident

In the above cases, the following should be taken into account:

- the period of study / treatment should be short-term (no more than six months);

- the reason for being abroad must be documented (contract with a medical institution / educational institution, payment documents, etc.).

In case of violation of the above conditions, the period of stay abroad in the calculation of 183 days is not taken into account. Foreign business trips of new employees Currently, many companies send their employees on business trips abroad. How, in this case, to determine the period of stay of an employee in the Russian Federation and establish the status of residency? If during the billing period the employee was abroad for the purpose of a business trip, then the determination of residency for him is carried out in the general manner.

Resident (right)

Determining the status of a resident and non-resident of the Russian Federation An economic entity is a resident of the country where its main place of residence is located, regardless of its citizenship. Content A resident is a legal or physical entity. a person registered in a given country who is fully subject to national law. A non-resident is a legal, natural person operating in one state, but permanently registered and residing in another.

It can also be organizations and organizations that are not legal entities. persons established in accordance with the legislation of foreign states, or foreign diplomatic and other official representations located in the country, as well as international organizations, their branches and representative offices. As a rule, the term is used in relation to the rights and obligations of persons in financial and tax legal relations.

Obligations of a resident But, as elsewhere, in addition to rights, there are obligations, they are also established by this law: - to represent authorities and agents currency control documents and information, if necessary; provision of information - to keep records and draw up reports on their foreign exchange transactions in accordance with the established procedure, ensuring the safety of relevant documents and materials for at least three years from the date of the relevant foreign exchange transaction, but not earlier than the date of execution of the contract; reporting - to comply with the instructions of the currency control authorities to eliminate the identified violations of the acts of the currency legislation of the Russian Federation and the acts of the currency regulation authorities.

Resident or non-resident how to determine a legal entity

Documents confirming a short-term stay abroad Documents confirming a person's stay outside Russia for short-term treatment or education include:

- contracts with medical (educational) institutions for treatment (training);

- certificates issued by medical (educational) institutions, indicating the treatment (training) with an indication of its time;

- copies of passport pages with special visas and border control marks on crossing the border.

At the same time, restrictions on age, types educational institutions and studied disciplines, medical institutions and diseases, there is no list of countries in which training or treatment takes place. This is stated in the letters of the Ministry of Finance of Russia dated June 26, 2008 No. 03-04-06-01 / 182, the Federal Tax Service of Russia dated October 15, 2015 No. OA-3-17 / 3850 and dated July 20, 2012

So, the dates of entry into and exit from Russia can be established according to the marks of the Russian border service:

- in the passport;

- in a diplomatic passport;

- in the official passport;

- in the migration card;

Marks made in the documents by the border services of foreign states (including the participating states Customs Union), are not taken into account when determining tax status: they cannot confirm the duration of a person’s stay in Russia (letter of the Ministry of Finance of Russia dated April 26, 2012 No. 03-04-05 / 6-557).

How to recognize a resident or non-resident legal entity

So, the dates of entry into and departure from Russia can be set by the marks:

- in the passport;

- in a diplomatic passport;

- in the official passport;

- in the sailor's passport (sailor's identity card);

- in the migration card;

- in the refugee's travel document, etc.

If there is no mark in the passport (for example, a person came from Ukraine or the Republic of Belarus), then other documents may be proof of their stay in Russia. For example, documents on registration at the place of residence, receipts for accommodation in a hotel.

For working people - timesheets or certificates from the place of work, issued on the basis of these timesheets. For students - a certificate from the place of study, which confirms the actual attendance of the educational institution.

This follows from the letters of the Ministry of Finance of Russia dated January 13, 2015 No.

Russian Federation with individuals located outside the territory of the Russian Federation - residents, as well as branches, representative offices and other divisions of legal entities established in accordance with the legislation of the Russian Federation, and individuals - non-residents under contracts for the carriage of passengers, as well as settlements in foreign currency and the currency of the Russian Federation with resident individuals and non-resident individuals located outside the territory of the Russian Federation under contracts for the carriage of goods transported by individuals for personal, family, household and other needs not related to entrepreneurial activities.

A few years ago, after graduating from college with a degree in finance and credit, I got a job as an accountant. I didn’t have much experience in this area, therefore, the mistakes and inaccuracies that I made from time to time were quite serious.

There were also plenty of gaps in knowledge, and one of the essential points was the ignorance of who are residents and non-residents in tax legislation. I had to carefully understand this issue and today I will tell you already from own experience how to determine the status of a taxpayer, what are the differences between these concepts and how the choice of one of them can affect the registration tax reporting and formation of obligatory payments.

The above terms are well known to many Russians and citizens of other countries, however, they can be used in different areas. It's about about these areas:

- tax area, where the status of a tax resident or non-resident indicates the source of income: in the state or outside the country. Taking into account this characteristic, tax rates are determined in the future;

- currency sphere, where it comes to establishing control over ongoing operations. Residents, in this case, are required to obey certain rules and submit relevant reports within the framework of the current regulations;

It should also be noted that the terminology is also present in other areas, for example, when resolving issues of inheritance of property. In this regard, in order to be able to interpret these concepts in the right way, it is necessary to clearly understand what is the difference between the concepts of "resident of the Russian Federation" and "non-resident".

What is the difference between the concepts?

What thoughts visit a person who first encountered the indicated terms, and is far from the legal, tax or financial spheres? A quite natural question arises: what is it and by what principle should the two concepts be distinguished.

At the first consideration of the concept, one might get the impression that a resident of a country is just a resident with an official civil status, but a non-resident is a foreigner. Of course, there is some truth in this, however, in fact, such an interpretation is not entirely correct. First of all, the main criterion for evaluating the term is the period of a citizen's stay inside the Russian Federation and outside the country.

If you turn to monetary sphere, then the group of residents includes persons with the status of:

- citizens of the Russian Federation who permanently reside in the country;

- foreigners and persons without civil status who are permanently within state borders.

All other members of various currency transactions will be considered non-residents. In the tax sphere, everything happens in a similar way. If a person lives in the country for at least 183 days during the year, then he receives the status of a resident. Business trips of military personnel or civil servants for any period of time outside the state are not the reason for the loss of this status. All other persons are included in the group of non-residents.

How to determine what status a particular person has?

It is worth noting that even one month is enough for the taxpayer status to change. To do this, it is enough to leave the state or return back to the country. However, there are no indications in the current legislation regarding the need to send a notification to the IFTS about a change in status.

An important point is also the fact that citizenship does not affect the determination of this status. In some cases, however, it is provided that even if a citizen left the country for a long time, this period is not taken into account. It is about the following points:

- a person left the Russian Federation for a period of not more than six months to undergo a treatment course;

- a citizen was trained for six months in another state;

- the taxpayer was listed as seconded for oil and gas production outside his country.

Some nuances in determining status may arise when a person wants to emigrate from Russia and sells his own property. In fact, such persons are no longer residents, although formally they continue to be considered as such. They will need to pay personal income tax and here the amount of the fee depends on the status. The fact is that residents pay at a rate of 13%, but non-residents pay at a rate of 30%.

Why do I need to confirm the status and how does it happen?

Confirmation of the official status of a taxpayer is not prerequisite, however, providing required documents can become the basis for a significant reduction in the tax burden. The opportunity provided is especially relevant in the case when a citizen is a taxpayer in several countries at once.

The confirmation procedure is quite simple and requires the preparation of documentation confirming the fact that for 183 days a year, a person lived on the territory of the state. All documents are transferred to the IFTS.

Conclusion

Concepts such as "resident" and "non-resident" have a serious impact on determining the level of the tax rate. For the first group of taxpayers, such indicators are significantly reduced, but holders of the second status are required to pay assessed contributions and taxes at higher rates.

tax resident- any person who, under the laws of a State, is liable to tax therein on the basis of his domicile, his permanent residence, his place of incorporation as a legal entity, the location of his governing body, or other similar criterion.

For tax residents of their country, states establish one taxation rules, and for non-residents, somewhat different ones.

In the Russian Federation, tax residents are recognized individuals and organizations.

Russian tax resident -

For the purpose of calculating personal income tax, tax residents are citizens who actually stay in the Russian Federation for at least 183 calendar days within 12 consecutive months.

If a citizen went abroad for short-term (less than six months) treatment or training, as well as for the performance of labor or other duties related to the performance of work (provision of services) at offshore hydrocarbon deposits, then the period of his stay in the Russian Federation is not interrupted.

Also, regardless of the actual time spent in the Russian Federation, Russian military personnel serving abroad, and employees of state authorities and local self-government, seconded to work outside the Russian Federation, are recognized as tax residents.

The countdown of 183 days starts from the date of crossing the border of the Russian Federation.

Consequently, persons who stay in the territory of the Russian Federation for less than 183 calendar days within 12 consecutive months are not tax residents of the Russian Federation. These can be, for example, foreign tourists who come to Russia for recreation and excursions, students who come to study, people who come to work in the Russian Federation, etc. At the same time, the presence or absence of Russian citizenship in an individual does not matter when determining his status as a tax resident of the Russian Federation.

In other words, both a foreign citizen and a stateless person can be recognized as tax residents of the Russian Federation.

In turn, a Russian citizen may not be a tax resident of the Russian Federation.

Confirmation of the status of a tax resident of the Russian Federation

The tax legislation of the Russian Federation does not establish any rules for confirming the actual time spent by a citizen in the Russian Federation and does not provide for special order determining its tax status.

Documents confirming the actual presence of citizens on the territory of the Russian Federation are:

information from the time sheet;

copies of the pages of the passport with the marks of the border control authorities on crossing the border;

data of migration cards;

documents on registration at the place of residence (stay), drawn up in the manner prescribed by the legislation of the Russian Federation.

The status of a tax resident of the Russian Federation for the purposes of paying personal income tax

Assigning to each taxpayer the status of a resident (non-resident) establishes his obligations to pay tax to the budget from his income, affects the types and methods of deductions.

In general, the income of individuals, regardless of their size, is taxed at a rate of 13%.

Income from sources in the Russian Federation received by an individual who is not recognized as a tax resident of the Russian Federation is subject to taxation at a rate of 30%.

For dividend income from equity participation in the activities of Russian organizations received by such an individual is applied at a rate of 15%.

For income for which other tax rates when determining the tax base than 13%, tax deductions, including standard deductions, do not apply. That is, the income of an individual who is not recognized as a tax resident of the Russian Federation is taxed according to increased rate and is not tax deductible.

Tax resident of the Russian Federation - organization

For the purposes of paying income tax, the following organizations are recognized as tax residents of the Russian Federation:

Russian organizations;

foreign organizations recognized as tax residents of the Russian Federation in accordance with an international treaty on taxation - for the purposes of applying this international treaty;

foreign organizations, the place of actual management of which is the Russian Federation, unless otherwise provided by an international treaty on taxation.

Wherein, Russian organizations recognized - legal entities formed in accordance with the legislation of the Russian Federation.

Foreign organizations are recognized - foreign legal entities, companies and other corporate entities with civil legal capacity, established in accordance with the laws of foreign states, international organizations, branches and representative offices of these foreign persons And international organizations created on the territory of the Russian Federation.

At the same time, tax residents - organizations are calculated on the basis of profits received not only in Russia, but also in foreign countries.

Still have questions about accounting and taxes? Ask them on the accounting forum.

Tax resident: details for an accountant

- Personal income tax in 2018: clarifications of the Ministry of Finance of Russia

A citizen of the Republic of Belarus, recognized as a tax resident of the Russian Federation, has the right to claim ... possessed by an individual who is a tax resident of the Russian Federation, of a Russian tax ... nature, an individual who is a tax resident of the Russian Federation, is produced by ... an individual, not recognized as a tax resident of the Russian Federation are subject to taxation... foreign country, who is not a tax resident of the Russian Federation, in the form of ...

- General and special income tax rates

Income received by foreign organizations recognized as tax residents of the Russian Federation in the manner prescribed by Art. ... foreign organizations that independently recognized themselves as tax residents of the Russian Federation in the manner provided for by the paragraph ... except for bonds of foreign organizations recognized as tax residents of the Russian Federation), which on the relevant dates ...

- A guide to tax amendments for medium-sized businesses. Winter 2019

For individuals who have lost the status of a tax resident of the Russian Federation. After all, upon receipt ... upon the sale of property Sale by a foreign tax resident of property that he owned ... in Cyprus, then you are not a tax resident of the Russian Federation. This carries a lot ... in relation to CFCs that recognized themselves as tax residents of the Russian Federation It was previously fixed ... in the Russian Federation that independently recognized themselves as tax residents of the Russian Federation can apply 0% ... ®: foreign company, who recognized herself as a tax resident of the Russian Federation due to being in ...

- Non-resident employee: personal income tax calculation

The actual time spent in the Russian Federation, tax residents of the Russian Federation are Russian military personnel passing ... From the above provisions, it follows that tax residents are any people who ... are received by individuals who are not tax residents of the Russian Federation. What is the procedure for determining the time ... received by individuals who are not tax residents of the Russian Federation, with the exception of income received ... if these citizens are recognized as tax residents of the Russian Federation in accordance with the provisions ...

- Legal Status of Cryptocurrency

Income received by individuals who are tax residents of the Russian Federation from the sale of other property...

- Review of letters from the Ministry of Finance of the Russian Federation for January 2019

The donee individual has the status of a tax resident of the Russian Federation. Income of an individual ... - a citizen of a foreign state who is not a tax resident of the Russian Federation, in the form of the cost ... by an individual of the status of a tax resident of the Russian Federation and the acquisition of the status of a US tax resident taxation ...

- income tax in 2017. Clarifications of the Ministry of Finance of Russia

Federation with the foreign state of which the branch is a tax resident foreign bank... /2/75684 In the event that a tax resident of the Russian Federation pays income to a foreign ... such income (part of it), which is a tax resident of the Russian Federation, if there is in ... such income (part of it), is a tax resident Russian Federation, paying income to a foreign...

- International holding companies: features of taxation

And foreign organizations recognized as tax residents of the Russian Federation; tax rates ... and foreign organizations recognized as tax residents of the Russian Federation are determined in a new ... foreign organizations (FO) recognized as tax residents of the Russian Federation form the value of property (property ... or foreign organization recognized as a tax resident of the Russian Federation. With regard to the value of property ... companies and foreign organizations recognized as tax residents of the Russian Federation, the period starting ...

- New reporting on personal income and personal income tax amounts

Digit: - 1 - if the taxpayer is a tax resident of the Russian Federation (except for taxpayers engaged in labor ... is a tax resident of the Russian Federation; - 3 - if the taxpayer is a highly qualified specialist is not a tax resident of the Russian Federation ... living abroad, is not a tax resident Russian Federation; - 5 - if the taxpayer is a foreign ... in the territory of the Russian Federation, is not a tax resident of the Russian Federation; - 6 - if the taxpayer is a foreign ...

- Introducing a new personal income tax reporting form: 3-personal income tax

...) __% To be completed only by taxpayers who are tax residents of the Russian Federation; the amount of income from... the Russian Federation is indicated To be completed by individuals who are tax residents of the Russian Federation; the amounts of standard, social... immovable property are calculated To be completed by individuals - tax residents of the Russian Federation; calculating property taxes... professional deductions» is filled in by individuals - tax residents of the Russian Federation who received income from sources ...

- Deoffshorization, CFC and tax information exchange in 2017

Accounts whose (beneficial) owners are Russian tax residents. In the list of information collected ... double taxation applies ONLY to tax residents of contracting countries that are the ultimate beneficiaries ...

- International Group of Companies (MGK): new concepts and new administration

From the criteria: is recognized as a tax resident of the Russian Federation; is not recognized as a tax resident of the Russian Federation, is subject to taxation ... persons) is not recognized as a tax resident of the Russian Federation; is recognized as a tax resident of the Russian Federation, is subject to taxation... by an organization that voluntarily recognized itself as a tax resident of the Russian Federation, submitted a notice of... an organization that voluntarily recognized itself as a tax resident of the Russian Federation, which is entrusted with... the CIM for the states (territories), whose tax residents are members of the MGK, ...

- We are hiring a foreign worker

Payers of personal income tax individuals are recognized as tax residents of the Russian Federation, as well as individuals ... of sources in the Russian Federation who are not tax residents of the Russian Federation. Remuneration for the performance of labor ... Tax Code of the Russian Federation): for a foreigner who is a tax resident of the Russian Federation - 13% (clause 1, ... 3); for a foreigner who is not a tax resident of the Russian Federation - 30% (clause 3). ... applies even without obtaining the status of a tax resident of the Russian Federation (Article 73 of the Treaty, p.

- We work with countries with which there are international agreements on the avoidance of double taxation: what documents to confirm

State certificates confirming the status of a tax resident of the relevant country for the application of the provisions ... states of the certificate confirming the status of a tax resident of the corresponding country for the application of the provisions ... allow to accept documents confirming the status of a tax resident of a foreign state, without affixing an apostille ...

- Income tax in 2018: clarifications of the Ministry of Finance of Russia

Federations that are concluded with states whose tax residents are foreign organizations that have ... the availability of an original document confirming the status of a tax resident of a foreign organization, issued by the competent authority ...

When distinguishing between the concepts of "resident of the Russian Federation" and "non-resident of the Russian Federation", one can often hear that any Russian citizen is considered a Russian resident. In fact, such a status is assigned based on the length of time a person has been in Russian territory.

Basically, these distinctions are necessary for taxation and control in the field of currency legislation. Tax categories have different tax rates, foreign currency categories have different obligations when opening accounts abroad and using them.

Tax residents and non-residents

Residents- These are citizens of the Russian Federation or citizens of other states staying on the territory of the Russian Federation for more than 183 days in the last 12 months.

However, the period of 183 days does not have to be consecutive. The main thing is that the total number of days during the year should be at least 183.

Non-residents- Russian and other citizens staying on Russian territory for less than 183 days in consecutive 12 months.

Exceptions:

- Russian military serving abroad.

- Civil servants who are on business trips abroad.

For employees of consulates and trade missions, the status is determined in accordance with the generally established procedure.

Obtaining the status of "tax resident"

How and who becomes a tax resident:

- citizens of Russia automatically, unless proven otherwise (the fact of residence in the Russian Federation is less than 183 days);

- Foreign citizens are automatically recognized as non-residents unless they prove that they have lived in the territory of the Russian Federation for more than 183 days.

Only a residence permit in the Russian Federation of a foreign citizen does not confirm his recognition as a tax resident.

Determining this status is important. For example, for residents of the Russian Federation, personal income tax (PIT) is levied at a rate of 13%, for non-residents - 30%.

Currency resident / non-resident

All Russian citizens are currency residents, as well as foreign citizens with a residence permit and stateless persons permanently residing in the Russian Federation.

At the same time, the legislation provides for the obligations of currency residents that arise when opening and maintaining accounts abroad:

- inform the tax authorities about opening, changing details or closing accounts in foreign banks (within a month);

- send reports on transactions on these accounts once a year (not later than June 1 of the year following the reporting one);

- carry out only those operations that are listed in Art. 12 of the Law of the Russian Federation "On currency regulation and currency control".

Until 2018, citizens living outside the Russian Federation for more than 12 months were recognized as foreign currency non-residents.

However, when entering the territory of Russia even for a day, they again became currency residents with the renewal of the need to comply with all legal requirements, which is extremely inconvenient for citizens permanently residing and working abroad, but periodically coming to Russia to visit relatives or on vacation.

On January 1, 2018, amendments to the law came into force, according to which all Russian citizens, regardless of the period of stay abroad - currency residents. But at the same time, individuals permanently residing abroad for more than 183 days within 12 months are exempted from the restrictions of currency legislation and are not required to inform the tax authorities about their accounts in foreign banks.

Thus, tax and currency residents have actually become equated concepts.