How to minimize vat in. VAT exemption: how to avoid paying VAT while working in general mode

Craftsmen and VAT can reduce, and keep profits intact. Basically, "games" with the amounts of this tax only lead to a delay in payment of the tax. However, transferring the "headache" of the current one to the next tax period does not mean reducing the amount of tax payable. P, every taxpayer dreams of not paying at all. Let's try?

What to hide?

VAT - indirect tax... You create added value - add to sales price your product or service the amount of tax. The buyer will pay it to you as part of the price of the goods. It would seem that you simply transfer the amount that the buyer gave you to the budget, all yours remains with you. So why is the urge not to pay so strong? Right! The amount of value added tax underpaid to the budget is corrected financial position entrepreneur in the direction of increasing income, and this income is not subject to income tax. In addition, you need to withdraw your own money from circulation to pay tax to the budget today, and the buyer, perhaps, will pay off tomorrow ... Or it may happen that it will never pay off. Therefore, you need to "optimize" (or "plan") this process. The main thing is that the amount of VAT payable to the budget is a value acceptable for a business entity.

The procedure for calculating and paying value added tax to the budget is established by Chapter 21 of the Tax Code of the Russian Federation. Taxpayers pay to the budget the difference between the amount of tax calculated at the established rate from tax base, determined in accordance with article 153 of the Tax Code of the Russian Federation, and the amount of tax deductions. The deductible is the amount of tax presented to the taxpayer by the sellers when purchasing goods, works, services used in activities subject to VAT.

There are two ways to reduce the amount of tax to the budget:

- understate the tax base or apply reduced tax rates;

- increase the amount of tax deductions.

We will especially mention the third way to avoid paying VAT.- for this it is enough to stop being its payer. The method is not very popular, but it is absolutely legal.

There are opportunities for the company to reduce the tax burden on VAT. Most of them stem from the competent application of the norms of Chapter 21 of the Tax Code of the Russian Federation. The basic rule for entrepreneurs who want to reduce the tax burden: “enriching the budget” in a smaller amount is possible if the probable tax implications a particular deal at the stage of its planning.

We are exempt from VAT

The method is provided by ourselves tax legislation... Based on the provisions of Article 145 of the Tax Code of the Russian Federation, a company has the right to exemption from taxpayer obligations, subject to certain conditions specified in the article.

So, for example, those companies whose revenue for three previous consecutive calendar months does not exceed 2,000,000 rubles (excluding tax) can be exempted from VAT. The main thing is that the business entity does not sell excisable goods, meets the criteria stipulated by the norms of Art 145 of the Tax Code of the Russian Federation and notifies the tax authority of the use of the right to exemption from VAT. For the next 12 consecutive months, the organization may not pay VAT to the budget, if it does not lose this right earlier. However, the organization will have to recover the VAT amounts already accepted for deduction before using the right to exemption from VAT. This method is also bad for those who sell goods and services to companies using the general taxation system. After all, not being a tax payer, you will not be able to allocate tax amounts in invoices, and buyers will not be able to show VAT on the valuables purchased from you, for deduction.

"Simplified"

You can transfer your company to a simplified taxation system. In this case, the company ceases to be a VAT payer, reducing optimization costs. However, there is one complication. The transition to the “simplified system” will require the restoration of VAT amounts for those values for which the amount of tax has already been accepted for deduction, but which have not been used in VAT-taxable activities prior to the transition. There is a secret to avoid this: reorganization in the form of an allocation. The new legal successor is endowed with property without the obligation to charge VAT upon its transfer (subparagraph 2, paragraph 3 of article 39 of the Tax Code of the Russian Federation and subparagraph 1 of paragraph 2 of article 146 of the Tax Code of the Russian Federation). go to the "simplified" system. There is no need to restore VAT on property received during the reorganization, since the reorganized organization is exempt from the obligation to restore VAT (clause 8 of article 162.1 of the Tax Code of the Russian Federation), and the newly created company did not use the deduction, therefore there is nothing to restore it (clause 3 of article 170 Tax Code of the Russian Federation).

When using this method, remember that no measures should be aimed solely at optimizing taxation (clause 9 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation of October 12, 2005, No. 53).

Instead of the price of the goods - a fine

The two companies enter into an agreement, the terms of which stipulate strict deadlines. The contract clearly stipulates penalties for violation, for example, of the payment deadline. In this case, the price of the goods is reduced upon sale by the amount of penalties that the seller will receive in the event of a "deliberate" violation of the terms of the contract. The buyer's benefit is the ability to immediately take into account the amount of recognized sanctions for violation of the contract in the costs, the seller's benefit is the ability not to charge VAT on the amount of the forfeit received, since it is not related to payment for the goods, but is a way to protect the violated right. The sanctions received for violation of the terms of business contracts do not increase the tax base for VAT (Resolution of the Supreme Arbitration Court of the Russian Federation of February 5, 2008 No. 11144/07).

There is no need to repeat this operation with the same counterparty. Provide in the contracts initially feasible conditions, demand from the buyer a written explanation of the reasons for the violation of the terms of the contract. At the same time, these reasons themselves should convincingly prove the absence of "intentionality" in the actions of the buyer.

Masking received advances

The method is as old as this world. In accordance with subparagraph 15 of paragraph 3 of article 149 of the Tax Code of the Russian Federation, the loan is classified as an operation not subject to VAT. Therefore, for the amount of the advance payment between the seller and the buyer, it is possible to draw up a loan agreement, which subsequently, by the novation agreement, can be transferred into payment under the supply agreement. It is extremely difficult for the tax authorities to prove that such a transaction is feigned. Instead of the novation agreement, you can return the loan to the buyer, who will already transfer the specified amount as payment under the supply agreement.

The norms of article 380 of the Civil Code of the Russian Federation state that the deposit is not an advance, and therefore it is not necessary to charge VAT from it. The issue, of course, is controversial, and to resolve it in favor of the taxpayer, you will have to go to court.

We provide commercial loans

A common case is when a large batch of goods or expensive fixed assets is sold in one tax period. The seller, having a preliminary agreement with the buyer, reduces the value of the property while providing a deferred payment. The amount of interest is equal to the amount of the discount. The result of such actions is a decrease in the proceeds from the sale of goods, and, consequently, the tax base for VAT. Interest on commercial loan are not related to payment for goods, therefore, they are not included in the VAT tax base (subparagraph 3, paragraph 3, article 149 of the Tax Code of the Russian Federation).

Friendly companies

In order to constantly regulate the amount of tax payable, you can use the right established by paragraph 12 of Article 171 of the Tax Code of the Russian Federation, namely: to receive a deduction from the advance paid to the supplier. A deduction is possible on the basis of an appropriate invoice. This method works well when one of the holding companies for the tax period has the amount of tax to be reimbursed from the budget, and the other, on the contrary, is obliged to pay significantly more O the largest amount to the budget.

Friendly companies can use a tolling scheme. It allows you not to lose "input" VAT when purchasing materials from "simplified". The owner of the goods obtained as a result of processing is a giver, he will give the materials for processing to a company with a general taxation regime and will sell finished products... The processor will receive for his services minimum amount rewards.

Within the framework of a simple partnership, any property can be transferred without VAT. The two companies enter into a simple partnership agreement and contribute to the joint activity: one party - property, the other - cash. The VAT restored upon transfer of the contribution to a simple partnership will be deducted by the partnership itself. Upon termination of a simple partnership agreement, the property is distributed among the participants. The interested party can receive property instead of a monetary contribution, because it is in shared ownership divided at the discretion of the owners (clause 1 of article 252 of the Civil Code of the Russian Federation). If, upon exiting a simple partnership, a participant receives property at a cost that does not exceed his initial contribution, VAT is not charged (subparagraph 1 of paragraph 2 of article 146 of the Tax Code of the Russian Federation).

Goods in load

The seller sells the main commodity taxed at the rate of 18 percent with a minimum mark-up. When buying one product, the buyer is offered another, the sale of which is taxed at a rate of 10 percent. The second item is sold with a maximum mark-up. Such a transaction seriously affects the amount of tax calculated to be paid for the tax period.

Let's buy something unnecessary

The easiest way to reduce the amount of VAT that "accidentally" got out for payment on the eve of the return is to buy unnecessary things. This will not solve the problem of high VAT, but it will provide a deferral. But keep in mind - the constant use of the method leads to an overstocking of the warehouse. By the way, even if the goods have not yet been entered into the buyer's warehouse, but the transfer of ownership has taken place, the organization, if there is an invoice from the supplier, can accept the "input" VAT deduction. Of course, purchased goods can be written off, but in this case, the "input" VAT will have to be restored. There are ways not to do this. Judicial practice confirms that the write-off of goods for justified reasons gives the right not to recover VAT. Justified reasons include theft, shortage, or an emergency.

You can also adjust the amount of VAT payable by postponing the deduction to a later date. A delay in the commissioning of fixed assets, a change in the date of receipt of a supplier invoice, or a delay in the moment of posting of goods leads to the possibility of using the deduction in a different tax period.

The amount of VAT payable can be predicted already at the stage of preparing the transaction. Optimization paths depend solely on the terms of various contracts and the content of business transactions.

List of methods tax planning given here is far from complete. Based only on the norms of the Tax Code of the Russian Federation, the existing arbitration practice and on the explanations of the Ministry of Finance, each specific transaction can be carried out in such a way that tax burden will not be overwhelming.

Irina Sidorova, Financial Consultant legal company

The desire to reduce the amount of tax is a completely natural desire. On this moment Among all types of taxes, the second largest tax is rightfully taken by VAT. It must be paid by everyone who uses the general taxation system. And although in this situation it is impossible to avoid paying it without punishment, but how to reduce the VAT payable, there is a scheme in 2017, and it operates exclusively within the framework of the law.

Any purchase and sale is not carried out without VAT. It is a subtotal calculated on the margin that the entrepreneur uses to generate income. According to the established norms, the tax must be calculated from the proceeds that were received in connection with the shipment of the item that is eligible for taxation. Also, the calculation of this tax is carried out from other sums of money entering the account of the enterprise in the form of an advance. Reducing the accrued tax amount can help in 2017, there are two types of schemes.

The tax reduction process in both cases is carried out using the vendor invoice. In the first embodiment, it is possible to reduce the amount of realization. Another is to exaggerate the amount of deductions. The effectiveness of these methods will be achieved only with a competent approach to their application.

Any mistake is fraught with serious consequences. In addition to additional VAT charges, there will be penalties in the form of penalties and fines. Moreover, in the event of fraud detection by the tax authorities, more serious measures can be taken. However, VAT can be reduced by legal means.

Legal ways to reduce tax

For those who work according to OSNO, there are as many as 4 ways that make it possible to reduce tax within the framework of the law. So, to reduce VAT, you can replace the purchase and sale transaction with an agency agreement. The next method consists of drawing up a document between the seller and the buyer, which is a commodity / cash loan.

It is also possible to reduce the amount of tax with the receipt of income in installments, that is, using the advance amount as a deposit. But if these methods are not very suitable, there is an opportunity to be exempted from VAT altogether. To do this, the person working at OSNO must be transferred to tax statement about liberation.

What does it take to get rid of the tax?

Despite the fact that VAT is one of the mandatory types taxation, from its payment is quite possible. To achieve what you want, you just need to meet a few conditions. First of all, it is worth knowing that VAT exemption can be obtained monetary transactions held only at Russian market... All types of goods sold should not be related to the excisable category. In addition to these conditions, there is one more important one, which is directly related to income. Only those whose revenue qualifying for taxation for the quarter has not reached the limit of 2 million rubles can be exempted. This amount of income should be calculated excluding VAT.

If these criteria are met, the taxpayer can get rid of VAT for the entire calendar year. To do this, you must promptly submit an application for exemption from VAT to the Federal Tax Service. According to the law, those companies and entrepreneurs who have received tax exemption lose the obligation to calculate and pay it, as well as maintain an appropriate register. Along with the exemption from VAT, the taxpayer is additionally exempted from submitting a declaration to the tax authorities.

Of course, with the tax exemption, there are some restrictions on doing business. So, when the VAT is canceled, an economic object is deprived of the opportunity to conduct tax deductions for this tax. All incoming VAT amounts must be included on the unit of the product or service offered. It is worth noting that if a VAT-exempt payer will still issue invoices with tax, then he will need to make transfers tax amounts to the budget and timely submit declarations on them to the Federal Tax Service.

Substitution of a contract

One of the most common options used to reduce the amount of tax is the substitution of a standard agreement for an agency analogue. In this situation, the seller receives the status of an agent, which means that the tax base will need to be calculated from the amount of the remuneration received, which is indicated in the drawn up contract.

When using this option, you should be careful when drafting the contract. In the event of the slightest oversight, the tax authorities will deftly be able to re-qualify this document into a supply agreement. And here it will not be possible to get rid of penalties.

Value added tax (VAT) is federal tax, which all organizations and individual entrepreneurs using the general taxation system (OSNO) are obliged to pay to the state budget. Consider possible ways and schemes of how to reduce VAT payable in 2018.

Organizations and individual entrepreneurs apply in practice different ways and VAT reduction schemes.

1. Tax incentives

The application of tax incentives is provided for in article 145 of the Tax Code of the Russian Federation. Organizations and individual entrepreneurs are entitled to tax exemption if the amount of proceeds from the sale of goods (works, services) excluding value added tax for the three preceding consecutive months does not exceed 2 million rubles in aggregate, in accordance with paragraph 1 of Article 145 of the Tax Code of the Russian Federation. But legal entities that sell excisable goods, the list of which is specified in article 181 of the Tax Code of the Russian Federation, cannot take advantage of the tax incentive.

Possibility of application tax relief organizations and individual entrepreneurs, simultaneously selling excisable and non-excisable goods at the moment is controversial. Specialists of the Ministry of Finance of Russia, in a Letter dated October 31, 2013 No. 03-07-14 / 46542, indicated that if a taxpayer sells excisable goods, the right to a tax benefit is lost. That is, the right to exemption from tax is lost, starting from the first day of the month in which the excisable goods were sold until the end of the exemption period (paragraph 2 of Article 145 of the Tax Code of the Russian Federation).

Get 267 1C video tutorials for free:

To receive a tax benefit, a taxpayer must submit the following documents to the tax office no later than the 20th day of the month:

- extract from balance sheet;

- an extract from the sales book;

- journal of received and issued invoices;

- individual entrepreneurs provide an extract from the book of income and expenses.

2. Transition to the simplified taxation system (STS)

The transition to the simplified tax system relieves organizations from value added tax. But organizations using this method of reducing tax payable risk losing their counterparties working with VAT.

3. Transfer of the deposit to the counterparty

The listed deposit to the counterparty is not subject to taxation and thereby allows to reduce the amount of VAT paid.

4. Agency agreement

Conclusion of an agency agreement with a counterparty instead of a purchase and sale agreement. An agency agreement allows you to reduce costs. Only percentage is set agency fee, since the agent does not buy the goods, but takes them for sale.

5. Issuance of a cash loan

The scheme for issuing a cash loan instead of transferring an advance to a counterparty is as follows:

- an agreement is concluded on the provision of a loan to a counterparty, where it is necessary to indicate for what purpose the loan is issued;

- the agreement indicates an amount equal to the cost of the advance payment;

- issued money loan not subject to VAT;

- according to the supply agreement, the goods are shipped;

- provide services according to the service agreement;

- the counterparties approve the Offsetting Act, which stipulates the terms of repayment of the loan issued at the expense of the delivered goods or at the expense of the services rendered.

6. Payment of an advance on a bill

Taxpayers do not often use this method of reducing VAT payable. To apply a bill advance, you need:

- the supplier to issue its own bill;

- to transfer the bill to the buyer under the act;

- for the bill of exchange received, the buyer shall transfer the indicated amount to the current account of the drawer. In this case, tax agents will not consider the transferred money as an advance;

- document netting after the shipment of the goods or the provision of the service.

What should not be done when reducing VAT payable

It is not recommended to use fly-by-night companies to reduce the tax or understate the total amount of revenue. If, during the audit, the tax office proves that it was understated total amount proceeds, or that the used firm was a fly-by-night, you will be entitled to charge all your expenses. And on the identified amount of expense to charge VAT, respectively, a penalty and a penalty for late payment of tax are automatically charged.

Considering one or another of the above methods of reducing VAT, it is necessary to take into account the current tax legislation and comply with the rules for drawing up regulations in favor of the taxpayer. Correctly drawn up accounting and legal documentation by the accountant will protect the taxpayer from the claims of the tax service.

The main feature successful business- profitability. And it is achieved not only by increasing income, but also by reducing costs. Every entrepreneur knows that a significant part of the money earned goes to taxes. Therefore, it is extremely important to approach their payment rationally and use all legal opportunities to avoid unnecessary spending. One of the largest payments is value added tax, so we will talk about it.

Below we will talk about ways to reduce the amount of taxation, schemes in which you can not pay VAT at all, as well as the main conditions for the correct optimization of this tax. Important note - our story will be exclusively about legal methods of reducing tax burden.

How to avoid paying VAT?

Every time a business entity sells goods or services, the question arises of paying VAT. The desire to avoid it is quite understandable, but not all entrepreneurs take adequate measures for this. Meanwhile, there are effective ways to save on taxes, which are absolutely legal and will not raise questions from the tax authorities either during their conduct or during offsite events.

Take advantage of the benefits

Let's start with the easiest and safest way to avoid paying value added tax. If you are lucky enough to be one of those for whom the legislator has provided benefits, you will not have to do almost anything to avoid paying VAT. It is enough to confirm that you belong to the category of beneficiaries. Companies such as FIFA, its subsidiaries, national football associations, confederations, suppliers of goods, services and a number of other organizations associated with FIFA are not considered payers of the tax in question.

- When carrying out postal items abroad.

- For air transportation in some regions, city transport common use as well as suburban transport.

- In the case of the sale of certain medical goods and products, the provision of medical services.

- When funeral services are provided.

- When providing educational services.

- In the course of the activities of cultural and art institutions.

- When conducting banking operations.

This is not a complete list of non-taxable transactions. All categories are listed in article 149 of the Tax Code. If an economic entity conducts both taxable and non-VATable transactions, it is necessary to keep their separate records.

Apply zero rate

In addition to the automatic exemption of certain transactions from taxation, the law also provides for the possibility of applying zero rate... Business entities can, at their discretion, use it or refuse to zero the rate. The list of goods and services for the sale of which a zero rate may be applied is given in article 164 of the Tax Code.

Since January 2018, there have been some changes in this procedure. An additional category of goods has appeared, when the sale of which you can not pay the tax in question. In the case of processing on the territory of a free warehouse, free customs zone or on customs territory re-export objects are sold without paying VAT. To confirm the right to apply a zero rate, it is necessary to submit the relevant documents, in particular, a contract on the commission foreign trade transaction, shipping and transport certificates, as well as customs declaration... The right to apply a zero rate since the beginning of this year has also appeared for companies that carry passengers and baggage by air in the Kaliningrad region.

Get VAT exemption

When the business does not generate huge profits, you can count on a temporary VAT exemption. This chance is spelled out in Article 145 of the Tax Code. In accordance with it, if the conditions listed below are met, the tax can be waived throughout the year:

- Activities are carried out in the domestic market.

- The product that is being sold is not provided.

- The quarterly revenue to be taxed is less than RUB 2 million. excluding VAT.

To obtain an annual exemption from taxation, you must apply to the tax office and submit copies of issued or received invoices and an extract from the sales ledger. Private entrepreneurs submit an extract from the book of income, expenses and business transactions, and companies - an extract from the balance sheet. Taking advantage of the privilege, the company or Self employed may not keep a tax register and not submit a tax return.

After a year of VAT exemption, you can apply to the tax office again and extend the period for another year. The main disadvantage of this method of getting rid of the obligation to pay tax is the impossibility of canceling the benefit early. And this may be required if cooperation with a company exempted from taxation would be disadvantageous for counterparties.

Important: if, having received a tax exemption, you continue to issue invoices with VAT, you will have to pay this tax and file a declaration on it.

Hire people with disabilities

Article 149 of the Tax Code provides for exemption from VAT for organizations employing disabled people. In this case, the team should mainly consist of such persons. They must be at least 80 percent of the total number of employees, and if authorized capital consists of deposits public organizations disabled, the number of employees with disabilities must be at least 50 percent.

Switch to preferential tax payment regime

If you abandon the general taxation system in favor of one of the preferential ones, you can get rid of the need to pay VAT. The choice of tax payment regime depends on the characteristics of the particular business. Let's consider under what conditions they are used.

STS

All entities are obliged to pay value added tax economic activity who work for common system taxation. Hence, real way to get away from VAT - to switch to a simplified tax payment regime. However, this method is not available to all business entities, since there are some restrictions on the use of the “simplified system”. Only companies and private entrepreneurs who meet the following requirements can switch to it:

- The total amount of proceeds for six months did not reach 75 million rubles.

- The company has no more than 100 employees.

- The organization does not belong to one of the groups of taxpayers who, according to tax legislation, cannot use the simplified system (Article 346.12 of the Tax Code).

- Have legal entity there are no branches.

To formalize the transition to a simplified system, you must submit an application of the established form to the tax service. If all the conditions mentioned above are met, the economic entity gets the opportunity to not pay VAT and some other taxes during the next calendar year after the application.

Advice: if the business is too big for application of the simplified tax system, that is, the company has more than 100 employees or half-year revenue exceeds 75 million rubles, the situation is not hopeless (you are not doomed to pay VAT). You can reorganize a company by dividing it into several that meet the requirements for profitability and the number of personnel required for "simplified".

The benefits of using the simplified tax system are obvious, but do not rush to go to the tax office with an application for the transition. It is worth assessing the negative aspects of the change in the tax regime:

- Not all former and potential partners will agree to cooperate with you in a new status if they remain on the common tax system. This is due to the fact that when entering into contractual relations with economic entities on the simplified tax system, their tax expenses... In this case, to attract contractors, you can offer a system of discounts.

- Before changing the tax payment regime, we strongly recommend that you resolve the issue with the amounts of tax that are presented for deduction. Reorganization can be an excellent way out of this situation. The newly formed company will not have to recover the VAT amounts and will switch to the simplified tax system without any problems.

If such consequences do not scare you, feel free to switch to "simplified". It is completely legal and safe. Only preliminarily follows in tax office and pay for them.

Vmenenka

In addition to the simplified taxation system, there are several other taxation regimes under which businesses are exempted from the need to pay VAT. One of them is the imputed income tax (UTII), or the so-called "imputation". With this specific regime, the amount tax payments is determined based on the area in which the business operates and how large it is. When calculating UTII, the base monthly profitability is multiplied by indicators such as the area of the retail space and the number of employees. There is no income level in this formula and does not affect the amount of tax.

Agricultural tax

Choosing the unified agricultural tax (UAT) as a taxation system, business entities that operate in the agro-industrial sector should take into account that agricultural tax payers are exempt from paying value added tax until the end of the current year. At the same time, VAT accepted for deduction before the transition to a single agricultural tax is not restored. In a year, that is, from the beginning of 2019, entrepreneurs at the Unified Agricultural Taxation will become value-added tax payers, and the transition to this regime to save on VAT will no longer make sense.

Patent system

Only private entrepreneurs can conduct business activities on the basis of a patent. There is no such tax regime for companies. Its essence lies in the fact that an individual entrepreneur acquires a patent for a certain type of activity, and payment of its cost eliminates the need to pay taxes, including VAT.

How to reduce VAT?

So, you are not one of the lucky ones who managed to avoid paying VAT. Then we will try to at least reduce its amount. All of the methods described below are legal, but require close attention to detail and correct design to avoid problems with tax authorities... How can you reduce the tax burden?

Reduce the amount of tax with incentives

By general rule, VAT is paid at the rate of 18 percent of the tax base. But in some cases, listed in article 164 of the Tax Code, a 10 percent rate is applied, in particular when selling certain food products, medical goods, periodicals and goods for children, as well as in the case of the provision of domestic air transportation services.

Make a contribution to the authorized capital of another company

The legislation does not include property contributions to authorized capital as objects of taxation. The following legal scheme for reducing VAT is based on this. A company that wants to save on taxation is a member of the founders of another legal entity and makes a property contribution, and then leaves the number of participants and takes monetary equivalent their contribution.

Although the combination looks suspicious from the tax authorities' point of view, the law is not violated in this case, which is confirmed by an extensive arbitrage practice in favor of business entities.

Create a simple partnership

This method is similar to the previous one, but the company does not make a property contribution to the authorized capital of an existing organization, but merges with other firms for temporary cooperation. A simple partnership is created for the purpose of achieving a specific goal and is not subject to registration with the tax office. After the conclusion of the contract, the organizations included in the partnership contribute in the form of funds or property. After some time, when the goals set for the merger are achieved, the contract is terminated. At the same time, a company that made a property contribution to the authorized capital can receive money in return without paying VAT.

Exercise the right to deductions

According to Article 171 of the Tax Code, some categories of taxpayers can receive tax deductions, that is, reduce the amount of tax. This right is granted exclusively to companies operating under the general taxation system. To receive a deduction, it is recommended to conclude agreements for the supply of materials and the provision of services with organizations that pay VAT. At the same time, it is important to correctly draw up the operations carried out so that subsequently the tax authorities do not refuse to deduct due to an error in the name of the company or identification number.

Since the beginning of 2018, there have been some changes in the procedure for applying deductions. Now this procedure cannot be used if a company (individual entrepreneur) purchases a product or service for funds that were received as budget investment or subsidies.

In addition, the right to deduct the amount of input VAT if the share of expenses for non-taxable transactions is not more than 5 percent in this year will remain only for those economic entities that keep separate accounting records.

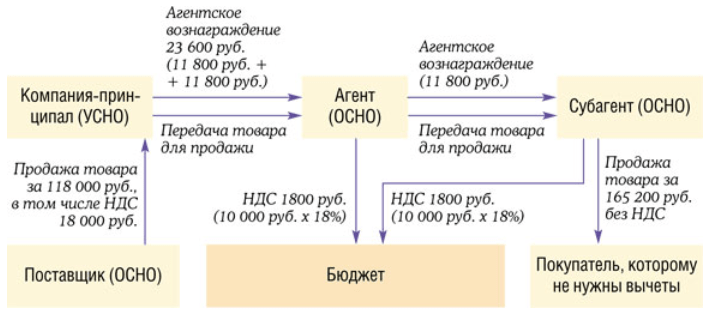

Replace the contract with an agency one

If the standard agreement is replaced by an agency agreement, the seller acts as an agent, and in this case, VAT must be paid only on the amount of his remuneration specified in the agreement. Under this scheme, prepayment for goods is made in the form of payment under an agency agreement, which is not subject to taxation. This method requires special attention to the paperwork. If the tax authorities succeed, using the oversights made in drawing up the contract, to conclude that this is not an agency, but a supply contract, a fine cannot be avoided. It is necessary to draw up a written order, which will contain specific tasks for the intermediary, as well as prepare a report on the work of the agent.

Conclude a mediation commission agreement

Many trading companies cooperate with business entities that use preferential taxation systems (in particular, the simplified tax system) or are exempt from VAT for other reasons. In this case, there is an opportunity to significantly save on this tax. If you enter into a commission agreement with an affiliated company that pays VAT, it will charge tax only on the amount commission... The amount of tax that must be paid corresponds to the difference between the VAT that would have been charged upon shipment of the goods and calculated after the goods were paid to the supplier-taxpayer. At the same time, purchasing goods from counterparties exempted from paying the tax in question, buyers pay value added tax in a significantly smaller amount than when buying directly without intermediaries.

Give buyers discounts

Another way to save on VAT is to provide a trade organization with discounts to its customers for goods that have already been delivered or for services rendered. If this is stipulated in advance in the contract, a correction invoice is drawn up. The taxable base and, accordingly, the VAT itself are reduced by the amount of the discount granted. In this case, the buyer is obliged to restore part of the tax amount accepted for deduction on the basis of the invoice.

Apply for a loan

The Civil Code provides for the possibility of including in the transfer agreement Money or other things in the ownership of another person, a condition on the provision of a loan, including in the form of installments, deferred payment, prepayment or advance payment. Upon receipt of an advance payment from a counterparty, an invoice is issued for its amount. Thus, the company confirms that it undertakes to pay VAT. However, this can be avoided by taking an interest-free loan from your buyer instead of a prepayment. After receiving the goods, the amounts received in debt are returned and the full payment for the delivery is made. In accordance with tax legislation, transactions of a cash loan are not taxed. This technique should be used if the advance payment and the final settlement are carried out in different tax periods.

It is possible to avoid accusations of deliberate attempt to evade VAT payment, provided that the prepayment and loan amounts do not match. In addition, you should not repay the loan and pay for the shipment of the goods on the same day. And one more caveat - you cannot abuse this method of exemption of the deposit from taxation, repeating the technique regularly.

Transfer a bill

You can also advance the purchase of goods without having to pay VAT using a bill. By Tax Code the transfer by the seller of the bill as a loan is exempt from VAT. By making a non-taxable payment on a bill of exchange, the buyer actually makes an advance payment for the purchased goods. It is important that the bill does not indicate the same date on which the delivery of the goods is scheduled. After receiving the purchased product, full payment is made for it and the bill is repaid.

Agree on a deposit

An advance payment can be replaced not only with a loan or a bill of exchange, but also with a deposit. To do this, you must conclude an appropriate agreement with the counterparty. By Civil Code the amount that is transferred under such an agreement is considered not a prepayment, but a means of securing an obligation. And VAT is not charged on such types of payments.

Fine the buyer

Another way to reduce VAT payable is to apply a fine or forfeit to the buyer for breach of contractual obligations. To use this technique, it is necessary, when drawing up the contract, to provide for the conditions that the buyer could violate, and indicate the penalty as a sanction. This can be, for example, a violation of the terms of shipment or payment. The scheme works as follows. The buyer violates his contractual obligations and pays a fine, which is actually an advance. Tax authorities can force them to pay VAT on the amount of the fine, but practice shows that the courts do not agree with this position and take the side of entrepreneurs.

Make an advance payment

In some cases, the payment of an advance can be useful to reduce the tax burden. It is possible to reduce VAT if its amount is too large for the company to be unable to pay, or there is reason to believe that in the next tax period the amount to be deducted will be large enough. The essence of the method is that the advance payment and the delivery of goods are carried out in different tax periods. With this technique, in most cases no delivery occurs. The seller simply returns the advance to the buyer.

What you need to know when optimizing VAT?

Optimization of taxation is a weakening of the tax burden by taking legitimate actions to use all the benefits provided by law, as well as other legal methods and techniques that allow you not to pay tax or reduce its amount. In other words, when optimizing VAT, the activities of a company or a private entrepreneur are organized in such a way that the amount of tax is minimized by legal means, without violating legislation (in particular, tax, criminal and administrative).

Consider the main aspects that should be taken into account when optimizing, the risks and possible negative consequences of its implementation:

- All schemes that are used with the aim of not paying or reducing VAT must be justified from an economic point of view.

- Optimization should be approached in a comprehensive manner, that is, use all legal opportunities to reduce the tax burden, various strategies, schemes, approaches and methods.

- When choosing a system for reducing tax or completely eliminating the need to pay it, you should first assess tax risks, including analyzing the practice of applying legislation and litigation.

- Optimization must be properly documented. For every business transaction you must have a document prepared in accordance with the law.

- For optimization to comply with the law, a company must apply only one type of taxation.

- The application of the chosen optimization technique should be justified from a legal point of view and aimed at achieving a clear business goal. If the measures taken are unsuccessful, this can lead to conflict situations with tax authorities, counterparties and their own employees.

- The techniques and optimization methods used should not be explicit to the reviewers. There is a risk of increased attention from the tax authorities. Despite the legality of the described methods of tax exemption, your actions are likely to interest authorized bodies, and you will have to explain yourself, defending your rights.

- There are some negative consequences associated with optimization. Having received a VAT exemption, an entrepreneur is faced with certain restrictions in economic activities. He, in particular, loses the right to carry out tax deductions for this type of compulsory payment. In addition, cooperation with a company exempted from the obligation to pay the tax in question may be disadvantageous to counterparties.

Save the article in 2 clicks:

A significant part of the expenses of a company or a private entrepreneur selling goods and services is VAT. Therefore, it is extremely important to use all legal opportunities to reduce the amount of this tax. At the same time, it is better to refuse the services of dubious offices offering them in order to avoid the appearance of even more serious problems than large sum VAT. Moreover, there are many legal ways to avoid paying tax or at least reduce its amount. Choose the most suitable one based on the specific characteristics of the business and possible negative consequences, but do not abuse even legal schemes and carefully draw up the documents, otherwise you will attract the close attention of the tax authorities.

In contact with

The controlling authorities consider that the amounts of the forfeit received by the seller from the buyer are measures of responsibility for violation of the deadlines for the fulfillment of obligations under the contract. Therefore, within the meaning of Article 162 of the Tax Code of the Russian Federation, they are not related to the sale and payment of goods. This means that they are not subject to VAT (letters of the Federal Tax Service of Russia dated 03.04.13 No. ED-4-3 / [email protected], Ministry of Finance of Russia dated 04.03.13 No. 03-07-15 / 6333). This method VAT optimization is safe. This was confirmed in 2008 by the Presidium of the Supreme Arbitration Court of the Russian Federation. In a resolution dated 05.02.08 No. 11144/07, the court indicated: when the seller receives a fine or penalty interest, the balance of interests of the parties to the transaction is restored, but the sale of goods, works or services has nothing to do with it. The lower courts are guided by this opinion and cancel additional charges (resolution of the Federal Antimonopoly Service of the Moscow District of 25.04.12 No. A40-71490 / 11-107-305).

What can be useful for: for planning the VAT load even before concluding an agreement for the sale of goods, works, services.

Scheme No. 2. Savings when replacing full-time employees with entrepreneurs using a simplified system

The essence of the scheme is that some of the employees leave the state and are registered as individual entrepreneurs. Insurance premiums entrepreneurs pay for themselves. If the income of the individual entrepreneur during 2016 exceeds 300 thousand rubles, then from the amount of such an excess it is necessary to pay contributions to the Pension Fund of the Russian Federation at a rate of 1 percent (part 1, 1.1 of article 14 Federal law dated 24.07.09 No. 212-FZ). If an individual entrepreneur applies a simplified tax system, then he has the right to reduce the tax on all contributions (letter of the Ministry of Finance of Russia dated 07.12.15 No. 03-11-09 / 71357).

The company has the right to take into account the amount of remuneration for the services of an entrepreneur when taxing profits. The basis depends on the type of services provided (legal, consulting, marketing, etc.).

The risk of this scheme is that auditors often try to retrain the relationship between the company and the individual entrepreneur into labor relations. If there is appropriate evidence, the court will support them. For example, in one of the cases, an individual entrepreneur provided services for a long time that were consonant with the duties of staff members. He also complied with the internal regulations (resolution of the Federal Antimonopoly Service of the North-West District of 09.11.10 No. A66-2676 / 2010). Risks increase if the organization is the only client of a friendly individual entrepreneur (definition of the Supreme Arbitration Court of the Russian Federation dated 09.06.10 No. VAS-6968/10).

What can be useful for: will help to identify the savings from replacing labor relations with civil law through the release of state and registration of an individual entrepreneur.

Scheme No. 3. Transfer of business to a privileged region

In the region where the preferential tax regime, the company registers the organization and transfers most of the assets to it. Will tax officials be suspicious of the fact that most of the revenue will settle there?

In many constituent entities of the Russian Federation, the authorities set reduced rates not only for single tax with the simplified tax system, but also for income tax, property tax. But when checking, the fiscal authorities carefully analyze the reasons for such a beneficial move from a tax point of view.

For the successful implementation of this scheme, it is important to confirm the business purpose of the business relocation. Otherwise, the court will decide that the only motive for such actions was tax evasion (for example, decisions of the Federal Antimonopoly Service West Siberian of January 29, 2013 No. A03-12357 / 2011, East Siberian from 19.09.13 No. A19-22759 / 2012 districts).