Calculation of the monthly depreciation amount for fixed assets. How to calculate depreciation using the straight-line method

This calculator calculates depreciation amounts for tax purposes, in accordance with Article 259 of the Tax Code of the Russian Federation. For tax purposes - that is, in order to take them for deduction when calculating personal income tax.

In order not to go far, but to be able to go to the original source right here, Article 259 of the Tax Code of the Russian Federation, according to the edition of which the calculator was written, is given below.

Initial cost of a depreciable property

Term beneficial use, in months

Depreciation rate as a percentage, straight-line method

Depreciation rate as a percentage, non-linear method

Article 259 of the Tax Code of the Russian Federation - Methods and procedure for calculating depreciation amounts

Federal law dated June 6, 2005 N 58-FZ, which comes into force on January 1, 2006 and Federal Law dated July 27, 2006 N 144-FZ, which comes into force on January 1, 2007 and applies to legal relations arising from On January 1, 2006, amendments were made to Article 259 of this Code:

- For the purposes of this chapter, taxpayers calculate depreciation using one of the following methods, taking into account the features provided for in this article:

1) linear method;

2) nonlinear method.

1.1. The taxpayer has the right to include in the expenses of the reporting (tax) period expenses for capital investments in the amount of no more than 10 percent initial cost fixed assets (except for fixed assets received free of charge) and (or) expenses incurred in cases of completion, additional equipment, reconstruction, modernization, technical re-equipment, partial liquidation of fixed assets, the amounts of which are determined in accordance with Article 257 of this Code.

- The amount of depreciation for tax purposes is determined by taxpayers on a monthly basis in the manner prescribed by this article. Depreciation is calculated separately for each item of depreciable property.

Accrual of depreciation for an object of depreciable property begins on the 1st day of the month following the month in which this object was put into operation. Calculation of depreciation on depreciable property in the form capital investments in objects of leased fixed assets, which in accordance with this chapter are subject to depreciation, begins for the lessor from the 1st day of the month following the month in which this property was put into operation, but not earlier than the month in which the lessor reimbursed the cost to the lessee of the specified capital investments, for the tenant - from the 1st day of the month following the month in which this property was put into operation.

The accrual of depreciation on an object of depreciable property ceases from the 1st day of the month following the month when the cost of such an object was completely written off or when this object was removed from the depreciable property of the taxpayer for any reason.

When calculating the amount of depreciation, the taxpayer does not take into account the costs of capital investments provided for in paragraph 1.1 of this article.

- The taxpayer applies the straight-line method of calculating depreciation to buildings, structures, transmission devices included in the eighth to tenth depreciation groups, regardless of the timing of commissioning of these objects.

For other fixed assets, the taxpayer has the right to apply one of the methods specified in paragraph 1 of this article.

The depreciation calculation method chosen by the taxpayer cannot be changed during the entire period of depreciation calculation for the depreciable property.

Depreciation is calculated in relation to an object of depreciable property in accordance with the depreciation rate determined for this object based on its useful life.

- When applying the linear method, the amount of depreciation accrued for one month in relation to an object of depreciable property is determined as the product of its original (replacement) cost and the depreciation rate determined for this object.

When applying the linear method, the depreciation rate for each item of depreciable property is determined by the formula:

K = x 100%,

where K is the depreciation rate as a percentage of the original (replacement) cost of the depreciable property;

- When applying the non-linear method, the amount of depreciation accrued for one month in relation to an object of depreciable property is determined as the product of the residual value of the object of depreciable property and the depreciation rate determined for this object.

When applying the non-linear method, the depreciation rate of the depreciable property is determined by the formula:

where K is the depreciation rate as a percentage of the residual value applied to a given item of depreciable property;

n is the useful life of a given depreciable property item, expressed in months.

Moreover, from the month following the month in which residual value of an object of depreciable property will reach 20 percent of the original (replacement) cost of this object, depreciation on it is calculated in the following order:

1) the residual value of the depreciable property for the purpose of calculating depreciation is fixed as its base value for further calculations;

2) the amount of depreciation accrued for one month in relation to a given object of depreciable property is determined by dividing the base cost of this object by the number of months remaining before the expiration of the useful life of this object.

- If an organization during any calendar month was established, liquidated, reorganized or otherwise transformed in such a way that, in accordance with Article 55 of this Code, the tax period for it begins or ends before the end of the calendar month, then depreciation is calculated taking into account the following features:

1) depreciation is not accrued by the liquidated organization from the 1st day of the month in which the liquidation is completed, and by the reorganized organization - from the 1st day of the month in which the reorganization is completed in accordance with the established procedure;

2) depreciation is accrued by the organization established as a result of reorganization - from the 1st day of the month following the month in which its state registration was carried out.

The provisions of this paragraph do not apply to organizations changing their legal form.

Federal Law No. 195-FZ of July 19, 2007 introduced amendments to paragraph 7 of Article 259 of this Code, which come into force on January 1, 2008.

- In relation to depreciable fixed assets used for work in conditions of an aggressive environment and (or) increased shifts, the taxpayer has the right to apply a special coefficient to the basic depreciation rate, but not higher than 2. For depreciable fixed assets that are the subject of an agreement finance lease(leasing agreement), to the basic depreciation rate, the taxpayer, for whom this fixed asset must be accounted for in accordance with the terms of the financial lease agreement (leasing agreement), has the right to apply a special coefficient, but not higher than 3. These provisions do not apply to fixed assets related to the first, second and third depreciation groups, if depreciation on these fixed assets is calculated using a non-linear method.

Taxpayers using depreciable fixed assets to work in an aggressive environment and (or) increased shifts have the right to use the special coefficient specified in this paragraph only when calculating depreciation in relation to these fixed assets. For the purposes of this chapter, an aggressive environment is understood as a set of natural and (or) artificial factors, the influence of which causes increased wear (aging) of fixed assets during their operation. Working in an aggressive environment also equates to the presence of fixed assets in contact with an explosive, fire-hazardous, toxic or other aggressive technological environment, which can serve as the cause (source) of initiating an emergency.

Taxpayers - agricultural organizations industrial type(poultry farms, livestock farms, fur-bearing state farms, greenhouse plants) have the right to apply a special coefficient, but not higher than 2, to the basic depreciation rate, chosen independently taking into account the provisions of this chapter, in relation to their own fixed assets.

Taxpayers are organizations with resident status of an industrial and production special economic zone or a tourist and recreational special economic zone, has the right to apply a special coefficient to the basic depreciation rate in relation to its own fixed assets, but not higher than 2.

In relation to depreciable fixed assets used only for the implementation of scientific and technical activities, the taxpayer has the right to apply a special coefficient to the basic depreciation rate, but not more than 3.

- Taxpayers who transferred (received) fixed assets that are the subject of a leasing agreement concluded before the entry into force of this chapter have the right to calculate depreciation on this property using the methods and norms that existed at the time of transfer (receipt) of the property, as well as using a special coefficient no higher than 3.

Federal Law No. 216-FZ of July 24, 2007 amended paragraph 9 of Article 259, coming into force on January 1, 2008.

- For passenger cars and passenger minibuses with an initial cost of more than 600,000 rubles and 800,000 rubles, respectively, the basic depreciation rate is applied with a special coefficient of 0.5.

Organizations that received (transferred) the specified cars and passenger minibuses on lease, include this property in the corresponding depreciation group and apply the basic depreciation rate (taking into account the coefficient used by the taxpayer for such property) with a special coefficient of 0.5.

- An organization purchasing used fixed assets has the right to determine the depreciation rate for this property, taking into account its useful life, reduced by the number of years (months) of operation of this property by the previous owners.

It is allowed to charge depreciation at depreciation rates lower than those established by this article by decision of the head of the taxpayer organization, enshrined in the accounting policy for tax purposes. The use of reduced depreciation rates is allowed only from the beginning tax period and throughout the tax period.

When selling depreciable property by taxpayers using reduced depreciation rates, recalculation tax base for the amount of underaccrued depreciation against the norms provided for in this article, no depreciation is made for tax purposes.

If the period of actual use of this fixed asset by the previous owners turns out to be equal to or exceeds its useful life, determined by the classification of fixed assets approved by the Government Russian Federation in accordance with this chapter, the taxpayer has the right to independently determine the useful life of this fixed asset, taking into account safety requirements and other factors.

- An organization receiving in the form of a contribution to the authorized (share) capital or by way of succession during reorganization legal entities used fixed assets have the right to determine their useful life as the useful life established by the previous owner of these fixed assets, reduced by the number of years (months) of operation of this property by the previous owner.

Excluded.

Federal Law No. 144-FZ of July 27, 2006 supplemented Article 259 of this Code with paragraph 15, which comes into force on January 1, 2007.

- Organizations operating in the field information technologies, have the right not to apply the depreciation procedure established by this article in relation to electronic computer equipment. In this case, the expenses of these organizations for the purchase of electronic computer equipment are recognized material costs taxpayer in the manner established by subparagraph 3 of paragraph 1 of Article 254 of this Code. For the purposes of this paragraph, organizations operating in the field of information technology are recognized as organizations specified in paragraphs 7 and 8 of Article 241 of this Code.

Each company has the opportunity to take into account costs that are directly related to the purchase of certain categories of assets using the depreciation method. It is in this way that expenses incurred by the company are taken into account when calculating taxes. Due to the fact that the actual amount of depreciation has a direct impact on the amount of the company’s income tax, the importance of correct calculation is an important task for the accountant. Let us consider in practice examples of calculating depreciation of property belonging to the group of fixed assets.

Methods for calculating depreciation

All the main points related to the calculation of depreciation are reflected in PBU 6/01 “Accounting for fixed assets”. This legal document reveals techniques that allow you to determine wear. These include:

- Linear;

- Declining balance;

- Write-offs are proportional to the volume of products produced;

- Write-offs based on the sum of numbers of SPI years.

It is important for an accountant to know that these methods are available for use strictly in accounting for the purposes of the organization’s accounting. As for tax accounting, the law establishes the existence of only 2 permitted methods - non-linear and linear.

Let us consider in more detail each proposed method of calculation in a practical situation.

Example of depreciation using the straight-line method

This technique is distinguished by its simplicity. That is why it has gained the greatest popularity among companies. The meaning of the methodology is that throughout the SPI, depreciation should be accrued in equal amounts using the formula:

A = Initial OS st. * The depreciation rate, in which case the depreciation rate will be calculated as follows:

Am-tion rate = 1 / Number of months of SPI.

Imperia LLC for 170 rubles. weaving equipment belonging to the OF group was purchased on 03/20/17. Based on the technical documentation, the SPI was set at 84 months.

Let us determine how the amount of deductions for weaving equipment will be calculated:

A = 170 tr. * (1/84*100%) = 2.024 tr.

Therefore, starting from April 1, 2017, the company will take into account depreciation in the amount of 2,024 tr. for 7 years.

The linear method is reasonably considered the most popular due to its ease of use in practice.

Depreciation: examples of calculation using the reducing balance method

The Avangard company purchased expensive computer equipment belonging to the OS category, costing 230 thousand rubles. In this case, the useful life will be 8 years or 84 months. The company's internal documentation determined that depreciation would be calculated using the reducing balance method. The company's management assumes that maximum income from the operation of the specified equipment will be received in the first years after purchase. As a result, Avangard decided to use an acceleration coefficient in the calculations, the value of which was determined to be 1.6%.

- Let's calculate the depreciation rate for 1 year:

NA = 100% / 8 years = 12.5%

- The annual depreciation rate taking into account the acceleration factor will be determined as follows:

NA = 12.5% * 1.6% = 20%.

- Size depreciation charges for the first year after commissioning, the operation of the equipment is calculated as follows:

A = 230 tr. * 20% = 46 tr, that is, the Avangard company will monthly depreciate computer equipment in the amount of 3,833 tr. (46 TR / 12 months).

Feature practical use This method makes it possible to take into account the specific intensity of equipment use.

- The amount of depreciation charges for the second year after commissioning of the equipment is determined:

A = (230 tr. – 46 tr.) * 20% = 36.8 tr. per year or 3,067 tr. per month (36.8 tr. / 12 months).

- The amount of depreciation charges for the third year after commissioning of the equipment is calculated:

A = (230 tr. – 46 tr. – 36.8 tr.) * 20% = 29.44 tr. per year or 2,453 tr. monthly (29.44 tr. / 12 months).

Depreciation: example of calculation using the write-off method in proportion to the volume of products produced

The Tandem organization purchased a machine for producing components for 780 rubles. In this case, the SPI is 5 years, that is, 60 months. Acceptance for registration was made in March 2017. Based technical passport The company's management assumes that this facility will be able to produce 70,000 units of components over the entire SPI. At the same time, 1,500 units were actually produced in April, and 1,800 units of products were produced in May. Let's determine the amount of depreciation in April and May 2017.

Apr = 780 tr. / 70,000 units * 1,500 units. = 16.714 tr.;

And May = 780 tr. / 70,000 units * 1,800 units. = 20.057 tr..

This method also allows you to take into account the intensity of equipment use, without taking into account those months when production is idle. However, in cases where the lack of orders is regular, the use of this technique is inappropriate.

Depreciation of fixed assets: example of calculation using the write-off method based on the sum of the numbers of years of SPI

The company purchased a vehicle painting booth for 460 rubles. and SPI 6 years or 72 months. Let's calculate the amount of wear and tear in the first three years of use of an asset.

- Am-tion rate = 6/(1+2+3+4+5+6) * 100% = 28.57%;

And annual = 460 tr. * 28.57% = 131.422 tr., that is 10.952 tr. monthly.

- Am-tion rate = 5/(1+2+3+4+5+6) * 100% = 23.81%;

And annual = 460 tr. * 23.81% = 109.526 tr., that is, 9.127 tr. monthly.

- Am-tion rate = 4/(1+2+3+4+5+6) * 100% = 19.05%;

And annual = 460 tr. * 19.05% = 87.630 tr., that is 7.303 tr. monthly.

Each company, based on its own needs and specifics of activity, individually determines the methods for calculating depreciation.

A vehicle, like any other equipment, after a certain period of operation due to wear and tear, requires repair. A cash, spent on maintaining and repairing any equipment or transport will be depreciation of the equipment (vehicle). If a car or other equipment is registered with any organization, then sum of money depreciation is included in consumable part enterprises.

Methods for calculating car depreciation

To calculate transport wear and tear, four methods are used in accounting. These four techniques are divided into linear and nonlinear. The company personally chooses the more suitable method for itself and uses it to calculate depreciation write-offs.

Accruals for automobile depreciation can be calculated using the following options:

- linear option;

- reducing balance option;

- option of deducting the price based on the sum of the numbers of years of useful consumption;

- option to write off the price according to the size of products or services.

The linear method of calculating transport depreciation is that the finances that are accrued for depreciation within one month are calculated by multiplying the initial or replacement price of depreciation specific for a given property.

To calculate the depreciation rate using the linear method, you need to know the number of months of useful transport consumption. Then you need to divide the unit by the period of useful use (calculated in months) and multiply by one hundred percent. The resulting figure is annual; to calculate monthly deductions, this value must be divided by 12.

To calculate the depreciation rate using the linear method, you need to know the number of months of useful transport consumption. Then you need to divide the unit by the period of useful use (calculated in months) and multiply by one hundred percent. The resulting figure is annual; to calculate monthly deductions, this value must be divided by 12.

This method of calculation is the most common due to its simplicity. Accrual of transport depreciation must begin on the 1st date of the month, which is subsequent to the month the vehicle was put into use. And these wear and tear are written off in equal amounts throughout the entire period of consumption.

Declining balance method

The fastest way to depreciate equipment is the declining balance method, which can write off movable property much faster in the early years of useful operation. This can be explained by the fact that in the initial period the productivity of the new vehicle higher and decreases over time due to aging. Therefore, it is advisable to depreciate the car as quickly as possible in the first years of its intended use.

To calculate this method of calculating depreciation, knowledge of the following characteristics is required:

- initial cost of assets;

- residual price;

- useful life.

To calculate wear motor vehicle using the reducing balance method, you need to: multiply the residual price (beginning of the year or month) by the depreciation rate (the formula is indicated in the linear method), multiply by the forcing coefficient (this indicator is set by the enterprise independently) and multiply by one hundred percent.

Method of calculating the price based on the sum of the numbers of years of useful life

Calculation of depreciation of a machine by the number of years of useful use, since the previous method is accelerated. The largest amount of money that is written off each month will be in the first year of using the car, after which these funds will decrease with each subsequent year.

The basis for this calculation is the initial price of the vehicle at which it was taken into account. This calculation is the product of the initial cost of the car and the depreciation rate.

The basis for this calculation is the initial price of the vehicle at which it was taken into account. This calculation is the product of the initial cost of the car and the depreciation rate.

Here, the wear rate will be calculated separately for each year and depend on the useful life of the vehicle. A method of writing off prices according to the volume of products or services.

This calculation differs from the previous three, which can be used mainly only for road transport. This depreciation rate is set as a percentage of the initial cost of vehicles for every thousand kilometers driven.

Examples of calculating vehicle depreciation

The depreciation of a car or other type of vehicle can be calculated on the Internet. Currently, there are many sites for carrying out such calculations. You just need to fill in the required fields and the portal will provide the necessary information.

But we must take into account that online payments are approximate and do not always take into account all the necessary parameters.

To more accurately calculate depreciation, you need to independently record all the money spent on the car. These costs usually include:

- purchase of spare parts and their replacement;

- repair;

- fuel expenses;

- tire replacement;

- technical inspection.

Example No. 1

The company purchased a new car and began using it on March 21, 2006. starting price vehicle amounted to three hundred thousand rubles. The useful life is five years.

Thus, the sum of the numbers of years of required consumption of the machine is equal to: 1+2+3+4+5=15

In accounting, depreciation of movable property was accrued in the following monetary equivalents.

In 2007 (1st year of use):

- annual amount will be: 5/15*300000 rub.=100000 rub;

- monthly accordingly will be: 100000/12=8333r.

In 2008 (2nd year of use):

- annual: 4/15*300000r.=80000r;

- monthly: 80000/12=6667 rub.

In 2009 (3rd year of use):

- annual: 3/15*300000r=60000r;

- monthly: 60000/12-5000 rub.

In 2010 (4th year of use):

- annual: 2/15*300000r=40000r;

- monthly: 40000/12=3333 rub.

In 2011 (5th year of use):

- annual: 1/15*300000r=20000r;

- monthly: 20000/12=1667 rub.

However, in tax records The monetary amount of depreciation costs is the same for each month and equals: 300,000 rubles/60 = 5,000 rubles.

Because monthly depreciation amounts vary, there are deductible time differences for the first two years of a machine's service. And in 2007, this difference will be: 8333 rubles - 5000 rubles = 3333 rubles.

Example No. 2

The cost of a domestic car purchased in 2013 is 200 thousand rubles; mileage from 2013 to 2016 - 90 thousand kilometers; estimated wear – 18.6%. To calculate natural depreciation, you need to multiply the initial cost of the car by the estimated wear and tear: 200,000 rubles * 18.6% = 37,200 rubles.

The cost of a domestic car purchased in 2013 is 200 thousand rubles; mileage from 2013 to 2016 - 90 thousand kilometers; estimated wear – 18.6%. To calculate natural depreciation, you need to multiply the initial cost of the car by the estimated wear and tear: 200,000 rubles * 18.6% = 37,200 rubles.

The residual cost of this vehicle will be equal to the subtraction of natural wear and tear from the initial cost of the car: 200,000 rubles - 37,200 rubles = 162,800 rubles. Having these calculations, you can calculate the costs per kilometer of travel, for this you need to divide natural wear and tear by the original price of the car: 37,200 rubles / 200,000 rubles = 0.18 rubles / km.

Features of the linear method of calculating depreciation

The main feature of this calculation is its simplicity. What is the uniform reduction in the cost of the vehicle in equal amounts. For most enterprises, this method is the most convenient.

The positive aspects of such accrual include:

- equal deductions for wear and tear throughout use;

- the increase in accumulated depreciation is distributed equally;

- uniform distribution of the residual price of real estate.

The disadvantage of this method is that it is not suitable for organizations that seek to pay off most of the depreciation in the initial period of use. Also, this method cannot provide immediate repair of the product used, which has become obsolete.

The nuances of calculating depreciation on a car

To calculate the wear and tear of a car more accurately, it is not enough to know the basic characteristics of the car. Typically, organizations use special directories for the most accurate calculation. In which the brand of the vehicle is indicated, as well as its book value by year of its release.

If you take an indicator from a certain table and divide it by the number of months during which the car was in use, you get the cost of wear and tear on a given vehicle in use for one month.

This calculation does not include information on the cost of fuels and lubricants, weather conditions, as well as finances spent on minor cosmetic repairs.

Thus, the choice of methodology directly depends on the organization or individual. The main thing when in various ways When calculating, remember the importance of all indicators that are responsible for the performance of a vehicle.

In contact with

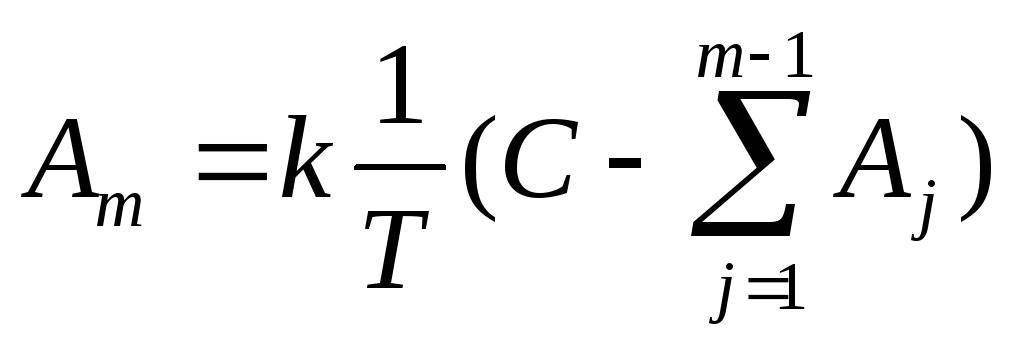

When using the linear method, the annual amount of depreciation of an object of fixed assets is determined based on the original cost of the object and the depreciation rate calculated on the basis of the useful life of this object:

where m is the number of the year from the beginning of the period of use of the fixed asset (m≥1); And m is the annual amount of depreciation; T - useful life of the object (in whole years); C is the initial cost of the fixed asset; L is the liquidation value of the fixed asset item.

Calculating depreciation in this way assumes that the cost of the asset is transferred evenly to costs over its useful life. This method is the simplest and most common.

In Microsoft Excel, the APL(C;L;T) function is used to calculate this depreciation.

Calculation of depreciation using the reducing balance method

When using this method, the annual amount of depreciation is determined not on the basis of the original cost, as with the linear method, but on the residual value of the fixed asset at the beginning of the corresponding year:

,

,

where m is the number of the year from the beginning of the period of use of the fixed asset object (m≥1);  And m is the annual amount of depreciation; T - useful life of the object (in whole years); C is the initial cost of the fixed asset;

And m is the annual amount of depreciation; T - useful life of the object (in whole years); C is the initial cost of the fixed asset;  - the amount of accumulated depreciation at the beginning of the mth year (here the liquidation value is taken equal to 0, i.e., the original cost is depreciated in full). Moreover, the depreciation rate ( ) at this method

- the amount of accumulated depreciation at the beginning of the mth year (here the liquidation value is taken equal to 0, i.e., the original cost is depreciated in full). Moreover, the depreciation rate ( ) at this method

.

.

can be increased by the acceleration factor k, i.e. may be accepted:

In Microsoft Excel, the function DDOB(C;L;T;m;k) is used to calculate this depreciation.

Calculation of depreciation by writing off the cost by the sum of the numbers of years of useful life (cumulative method)

,

,

This method involves calculating depreciation based on the original cost of the fixed asset item and the annual ratio, in which the numerator contains the number of years remaining until the end of the asset’s service life, and the denominator is the sum of the numbers of years of the asset’s service life:  where m is the goal number from the beginning of the period of use of the fixed asset object (m≥1); And m is the annual amount of depreciation; T - useful life of the object (in whole years); C is the initial cost of the fixed asset;

where m is the goal number from the beginning of the period of use of the fixed asset object (m≥1); And m is the annual amount of depreciation; T - useful life of the object (in whole years); C is the initial cost of the fixed asset;

When using this method, as with the linear method, the initial cost of the object is taken as a basis. However, the depreciation rate changes with each year of useful use of the fixed asset. The largest amount of depreciation is accrued in the first years of use of the fixed asset and gradually decreases towards the end of the term.

In Microsoft Excel, the ASC(C;L;T;m) function is used to calculate this depreciation.

Exercise

Select the task condition from Table 1 in accordance with the option number.

Calculate the amount of depreciation by year in EXCEL, taking into account the specified useful life of the object, initial cost and salvage value. Use linear method, the reducing balance method (with a factor of 2) and the method of writing off value by the sum of the number of years.

Perform the calculations in the table.

Construct a graph showing changes in the value of an object over the years when depreciated using different methods.

For each method, construct a pie chart characterizing the contribution of depreciation for each year to the total depreciation amount.

Construct a bar chart (histogram) illustrating the relationship between the amounts of depreciation calculated by different methods.

Table 1 Task options for №1

|

laboratory work |

option Initial |

price Initial |

Liquidation |

|

|

Useful life (number of years) | ||||

|

drilling | ||||

|

Computer | ||||

|

Measuring device | ||||

|

Transformer | ||||

|

Lathe |