Accounts receivable payments. What is accounts receivable: management, write-off and sale

As part of their business, companies often have to deal with transactions associated with the emergence of receivables. The presence of a large number of nuances and subtleties due to the peculiarities of recognizing this small nuisance and reflecting it in documents can often cause questions from accountants and users of reports. However, this problem will not present great difficulties if we consider in detail all the features associated with the recognition and reflection of debt in accounting. This article is devoted to these aspects.

What is a receivable and when does it arise?

In the course of its business activities, a company often has to interact with customers who purchase its goods and services, and suppliers who provide materials and components for a fee. DZ (accounts receivable) arises in the process of this interaction in the following cases:

- The company has transferred goods to customers, but has not yet received revenue for these goods. It is assumed that the customer will pay for the item at a later date.

- The company paid for the materials, but has not received them yet. The supplier is expected to deliver the materials at a later date.

That is, we can say that if a company has a remote control, then there are those who owe it something. It is important not to confuse accounts receivable with accounts payable. The fact that a firm has the latter means that there are economic agents to whom this company owes. At the same time, accounts receivable from one company are often payable to another.

The impact of accounts receivable on business

The question of the impact of the existence of accounts receivable on the conduct of business is controversial. On the one hand, it allows you to significantly expand your business opportunities. The entities with whom the company interacts do not always have sufficient funds to pay for goods and services in full. Then DZ is one of the few means that makes interaction possible.

However, it must be remembered that accounts receivable are the cost of goods that were sold but not paid for, or materials that were bought but did not receive for use. Accordingly, it always causes the diversion of funds from circulation, their temporary numbness. Consequently, if the volume of accounts receivable is too large, this does not contribute to the development of the business, but rather, on the contrary, hinders its expansion. In addition, there is always a risk that the debt will not be repaid, which inevitably leads to financial losses and may even lead to bankruptcy of the company. For this reason, the allowable amount of debt must be approached very carefully, carefully weighing all the risks and possible benefits.

Accounts receivable in the company's reporting

The amount of accounts receivable can be found by looking at the company's balance sheet. It is located in the balance sheet circulating assets. This category is presented without a reserve for doubtful debts, that is, without additional funds that, in theory, the company may not collect from debtors.

Sale of company debts and firm liquidity

The elements of the second section of the balance sheet are arranged in order of increasing degree of their liquidity. This concept is understood as its ability to transform into money in a relatively short time. The most illiquid part of the balance sheet is stocks, since selling them is the most difficult task. Selling DZ is also not easy, but a realizable task. The probability of a successful one depends on its conditions: the term, the reliability of the debtor, and so on. There are frequent cases of selling remote control devices at a reduced price, due to the lack of demand or tight deadlines for implementation.

Doubtful debts

Doubtful accounts receivable is an amount that a company may never expect to return. In order for it to be recognized as questionable, it must meet the following conditions:

- Debt arose in the course of operating activities, that is, that which is the direct purpose of the company's existence.

- The debt was not returned within the period specified in the contract. If there is no term in it, then to determine it, you must refer to laws, regulatory legal acts and other official sources of law.

- In relation to the debt, there should be no pledge or surety, since otherwise it can be claimed from another person who is the guarantor, or received by selling the pledged item.

It is important to remember that DZ is questionable if it meets all three of these conditions. Accounting for doubtful accounts receivable is characterized by the presence of some features that distinguish it from simple accounting.

The presence of such a problem does not mean at all that the funds are irretrievably lost. Doubtful accounts receivable is an amount, the recovery of which is still real. True, this happens extremely rarely, but if you act quickly and within the framework of the law, then everything can turn out very well. The write-off of receivables for doubtful debts occurs in the event of its full repayment.

Bad accounts receivable

Doubt receivables should not be confused with bad debts. The latter is almost impossible to return. To recognize a debt as uncollectible, any of these conditions must be met:

- The company cannot go to court to recover the amount from the debtor for reasons related to the law.

- The debtor company is liquidated. In this case, there is no economic entity that could return the debt, therefore, its collection cannot be implemented in any way.

Both of these conditions are equivalent, and for the recognition of the debt as hopeless, it is enough to fulfill at least one of the conditions.

Doubtful accounts receivable in the balance sheet

Let's consider some of the accounting features of this phenomenon. The share of doubtful accounts receivable affects its total value. So, if the company failed to recognize the fact of doubtfulness, then the entire debt is reflected as a receivable. If everything fully complies with the conditions specified earlier in the article, then the reserve for doubtful debts of receivables is calculated for the liability. This reserve reduces the total amount presented in section 2 of the company's balance sheet.

The write-off of doubtful accounts receivable occurs at the expense of the amount of the reserve, if, of course, it was created as part of the accounting policy. If the amount of the liability is greater than the amount of the provision, then the difference is written off to the company's expenses, reduces the amount of income tax and, therefore, increases the amount of net profit.

Why do you need a reserve for doubtful debts?

This reserve is necessary if there are serious reasons to believe that the debt will not be repaid on time. Doubtful accounts receivable is a factor that can harm the financial well-being of the company, and in order to reduce its impact on the business, the above provision exists.

The scheme of work is as follows: firstly, the company must indicate in the accounting policy the fact of creating a reserve. Based on the accounting data for doubtful accounts receivable, the organization calculates the amount of the reserve. Further, it is deducted from the profit, thereby reducing the volume of tax payments and increasing the amount of net income.

Features of creation

How to create an allowance for doubtful accounts receivable? Its value depends on how long the debt is overdue. Establishing these terms is a fairly reasonable decision of the state, since doubtful receivables are a debt that was not returned on time, and, of course, the likelihood that the liability will be returned, the delay time for which is 10-15 days, is much higher than if this time was six months or a year. Accordingly, due to differences in the likelihood of debt recovery, there is also a difference in the amount of reserves recognized.

So, if the counterparty does not repay the debt within a period of one to 45 days, this receivable cannot be considered doubtful, since this period is too short. Doing business is not always predictable, perhaps the counterparty does not repay the debt due to the presence of an unforeseen cash gap, therefore, for this reason, these types of debts are not recognized as doubtful, do not increase the amount of the provision and do not reduce the amount of income tax paid

If the maturity of the debt is from 45 to 90 days, then it is recognized in the amount of 50% of the total amount, increasing the amount of the provision by this amount.

Accounts receivable with a maturity of more than 90 days are recognized in full.

Debt Inventory Process and Its Significance

The definition of the above terms occurs during the inventory of doubtful receivables. After this operation, the reserve is adjusted as follows:

- If the counterparty returns a debt that was previously considered doubtful, then the amount of the liability is restored, respectively, the volume of the reserve is reduced by this amount. In addition, the company will be obliged to pay income tax based on the amount of debt received.

- If the counterparty does not repay the debt, then its value is completely written off at the expense of the reserve. If it is formed, then the company has no right to write off the debt at the expense of other means.

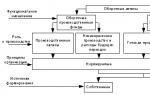

Accounts receivable management

Provisioning is a commonly used, but far from the only, receivables management tool. The main task of this process is to reduce the time it takes to repay the debt and to reduce the likelihood of receiving losses due to the bad faith of counterparties. However, there are other ways to achieve this goal.

So, if the DZ needs to be transformed into cash, it can be sold. However, in this case, there is a possibility of losses.

In addition, you can provide preferential terms of interaction for suppliers and customers who pay the company immediately, or as soon as possible. These conditions may include discounts, reduced commissions, and so on.

In addition, at the moment there is an opportunity to check the conscientiousness of debtors using special services, which can also significantly reduce the likelihood of economic losses. There are special factors of reliability of the counterparty, compiled on the basis of a survey of its suppliers.

DZ is a unique tool that allows companies to carry out inter-firm interaction, as well as cooperation with customers, even if the counterparties do not have the amount of funds sufficient to carry out various business operations.

Introduction. 3

1 Theoretical foundations of the analysis of receivables. five

1.1 Concept, essence and types of accounts receivable. five

1.2 Methodology for the analysis of receivables. nine

1.3 Methods and problems of accounts receivable management .. 16

2 Assessment of financial and economic activities of OJSC "Karavai". 21

2.1 General characteristics and assessment of the main economic indicators of the economic activity of the organization. 21

2.2 Express - analysis of the financial condition of the organization. 24

2.2.1 Analysis of the financial stability of the enterprise. 24

2.2.2 Analysis of the solvency and liquidity of the enterprise. 29

2.2.3 Analysis of the turnover of working capital (business activity) 36

3 Analysis of accounts receivable of JSC "Karavay". 38

3.1 Analysis of the composition and structure of receivables. 38

3.2 Analysis of the ratio of receivables and payables. 40

Conclusions and offers. 48

List of used literature .. 50

Applications. 52

Introduction

In the process of financial and economic activities, the enterprise constantly needs to settle accounts with its counterparties, budget, tax authorities. When shipping manufactured products or providing some services, an enterprise, as a rule, does not receive money in payment immediately, that is, in fact, it credits buyers. Therefore, during the period from the moment of shipment of products to the moment of receipt of payment, the company's funds are numb in the form of accounts receivable, the level of which is determined by many factors: type of product, market capacity, degree of market saturation with this product, contract terms, settlement system adopted at the enterprise, etc.

In order to properly build relationships with clients, it is necessary to constantly monitor the current state of mutual settlements and track trends in their changes in the medium and long term. At the same time, control should be differentiated in relation to different groups of customers, distribution channels, regions and forms of contractual relations.

Accounts receivable is indeed one of the most pressing topics of business entities in an emerging market economy. Carrying out entrepreneurial activities, participants in property turnover suggest that as business transactions are carried out, they will not only return the invested funds, but also receive income.

However, in real practice, especially with the transition to market relations and a decline in production, often, or rather constantly, situations arise when, for one reason or another, an enterprise cannot collect debts from counterparties. Accounts receivable "hang" for months, and sometimes even years. The growth of accounts receivable worsens the financial condition of enterprises, and sometimes leads to bankruptcy.

As a result, from the above, we can conclude that the topic of this course work "Analysis of receivables" is relevant.

The purpose of the course work consists in the analysis of accounts receivable and the development of recommendations for its management.

When writing a term paper, the following were solved tasks:

Disclosed theoretical aspects of accounts receivable;

Various methods of analysis of accounts receivable are considered;

The analysis of the financial condition of OJSC "Karavai" was carried out;

The analysis of dynamics, structure of accounts receivable of OJSC "Karavai" was carried out;

Research object is OJSC "Karavay".

The subject of research is the receivable.

Information base - annual accounting statements of the enterprise, constituent documents, accounting policies, synthetic and analytical accounting registers.

Study period - 2012-2014

To reveal the topic, textbooks on financial analysis, methodological instructions for analyzing the financial condition of organizations, as well as articles and publications of leading economists and accountants were used.

Theoretical foundations of the analysis of receivables

Concept, essence and types of receivables

Accounts receivable in monetary terms are part of the current assets of an economic entity and occupy a significant share in their composition. Accounts receivable can be defined as the amount of debts owed to an enterprise, firm, company from other enterprises or individuals, as a result of economic relationships with them. It is objectively necessary for the implementation of economic activities and is due to the current payment system.

Accounts receivable have now become the most liquid asset of the company. Hence the need for serious attention to it, its analysis, and its management.

In the literature, there are various definitions of receivables.

Accounts receivable are the claims of an enterprise in relation to other enterprises, organizations and customers to receive money, supply goods or provide services, or perform work.

Accounts receivable is the amount of debt owed by an enterprise from other legal entities or citizens.

Accounts receivable are funds temporarily withdrawn from the company's turnover.

The most complete definition, in our opinion, may be the following.

Accounts receivable as an economic category expressing financial relations between a debtor (debtor) and a creditor is:

· One of the types of current assets of the enterprise;

· The part of his proceeds from sales not received;

· A separate type of relationship arising from the contract, as well as as a result of causing harm and other grounds (Art. 307 and other Civil Code of the Russian Federation).

Or you can do it differently. Accounts receivable are mainly the uncollected part of the company's sales proceeds, which is formed from the contract as a separate type of obligations between companies. Accounts receivable can also be the result of harm and other reasons.

Accounts receivable of the enterprise as a whole is one of the types of its current assets.

The relationship between receivables and payables is that payables are the source of coverage for receivables. Therefore, in practice, when analyzing enterprises, they usually follow the relationship between them. At the same time, in the conditions of inflation, which stimulates non-payment, the growth of accounts payable is beneficial for the enterprise, and accounts receivable is not profitable.

Accounts receivable include the following:

· Debt of buyers and customers;

· Promissory notes receivable;

· Debts of subsidiaries and affiliates;

· Debt of founders on contributions to the authorized capital;

· Advances issued;

· Other debtors.

In most cases, the receivables from buyers and customers are the largest and reach 90% of all receivables. It is quite natural in a market economy to have a sufficient level of promissory notes to be received, since a deferral of payment to the buyer against a promissory note is the most effective form of such a relationship. That is why, when managing accounts receivable, it is very important for an enterprise, firstly, to optimize the amount of accounts receivable, secondly, to ensure timely receipt of this debt and, thirdly, to organize appropriately work with bills.

There are many signs of classification of receivables. Table 1 presents the most significant of them, as well as their explanation.

Table 1 - Classification of receivables

| Classification attribute | Debt types | Explanations |

| By the degree of liquidity | Highly liquid | Debt term less than 1 month |

| Medium liquid | ||

| Illiquid | Unrealistic to convert into cash, is hopeless | |

| By elements | Debts of buyers and customers | For the products provided, works, services rendered |

| Bills receivable | When issuing weights to the seller organization by its clients for the goods received | |

| Advances issued | Debts of suppliers to supply the enterprise with products or services against previously received advances | |

| Other debt | Subsidiaries and branches of the organization; accountable persons; budget, etc. | |

| By due dates | Short term | Payment is due within 12 months after the reporting date |

| Long term | Payment is due no earlier than one year after the reporting date | |

| By the nature of education | Justified (normal) | Complies with the terms of the agreement, due to the chosen credit policy of the organization; the due date is not yet due |

| Unjustified (overdue) | The terms of the contract have been violated, or the settlement documents have been drawn up with errors; payment is not received on time | |

| By the degree of reliability of debt repayment | Reliable | The client confirms his obligation, or secures his debt with a guarantee |

| Dubious | Payment was not received within the agreed period and the debt is not secured by a pledge, surety or bank guarantee. | |

| Hopeless | Debt that cannot be collected due to the fact that the limitation period (3 years) has expired, the debtor organization has been liquidated, or payment cannot be received on the basis of an act of the state body (in this case, a reserve for doubtful debts may be created). |

Continuation of table 1

| Classification attribute | Debt types | Explanations |

| By providing guarantees | Secured debt | Forfeit, pledge, surety, deposit, bank guarantee |

| Unsecured debt | ||

| By the degree of compliance with legal regulations | Debt duly reclaimed | The buyer confirmed his obligations, or there was an appeal to the court |

| Unclaimed receivables | ||

| Whenever possible planning | Planned | The debt is assumed in advance, as it is provided for by the credit policy |

| Unplanned | ||

| By the degree of control | Controlled | If an affiliate has an obligation to the organization |

| Uncontrolled |

Accounts receivable play an important role in the process of functioning of economic entities, as it affects many aspects of its activities, such as:

· Structure and size of working capital;

· The size and structure of the received proceeds from sales;

· Duration of the financial and operational cycle;

· The rate of turnover of circulating assets and assets in aggregate;

· The state of liquidity, solvency and financial stability of the organization;

· Sources of funds of the organization.

If the amount of receivables in the company is too large, there is a slowdown in the turnover of its assets and, as a result, an increase in the duration of the financial cycle. In addition, in this case, the organization needs to look for additional sources of funds to finance its activities.

Thus, it is possible to highlight both positive and negative aspects of the existence of receivables. Granting a deferred payment for goods, works, services helps to attract buyers and thereby stimulates the growth of sales and profits. However, on the other hand, an increase in the size of accounts receivable causes a slowdown in the turnover of current assets and a decrease in the efficiency of using current assets in general. In this regard, the organization needs to carry out competent management of accounts receivable.

From the article you will learn:

1. Why group receivables according to the likelihood of repayment.

2. Under what conditions the receivables are doubtful.

3. What accounts receivable are considered uncollectible. How to determine the limitation period for debt.

The well-known principle "in the morning - money, in the evening - chairs" in real life works exactly the opposite: as a rule, the final payment occurs after the delivery of the goods (provision of services, performance of work). Therefore, accounts receivable are an integral part of settlements with counterparties, and in many organizations its value is a significant part of all current assets. The presence of accounts receivable, in itself, is quite common, but do not forget that the amount of such debt shows the amount of funds actually withdrawn from circulation. In addition, there is always a risk of late repayment of debts on the part of debtors or non-repayment at all. Thus, receivables, as part of the property of the organization, requires special attention from the point of view of the principle of prudence: its indicator, reflected in accounting and reporting, must correspond to reality. For this, accounts receivable are divided into types depending on the likelihood of its repayment. What are these types, and what are the criteria for assigning to each of them - we will consider in this article.

The “reality” of receivables is checked for each debt separately, depending on the time of occurrence and the likelihood of repayment. According to these characteristics, the debt can be normal, dubious, or hopeless. Accounts receivable are considered normal if they are not due yet. Such debt is a consequence of the settlement procedure established in the contract, in which the final payment must be made within a certain period of time after the delivery of the goods (provision of services, performance of work).

Doubtful and bad debts of debtors (these concepts are enshrined in the legislation of the Russian Federation) deserve special attention from the accountant for the following reasons:

- doubtful and bad debts overestimate the indicator of accounts receivable and in the balance sheet currency as a whole, which leads to inaccurate financial statements;

- doubtful accounts receivable serves as the basis for the formation. In accounting, the creation of a reserve for doubtful debts is the responsibility of the organization, and in tax accounting it is the right of the taxpayer;

- for both accounting and tax accounting purposes.

Doubtful accounts receivable

What kind of debt is recognized as doubtful and hopeless under Russian law? In accordance with the Tax Code of the Russian Federation, accounts receivable are dubious if in relation to her simultaneously the following conditions are met (clause 1 of article 266 of the Tax Code of the Russian Federation):

- The debt arose in connection with the sale of goods, the provision of services, the performance of work.

! Note: in accordance with the clarifications of the Ministry of Finance of the Russian Federation, receivables not related to the sale of goods, works, services, namely:

- on advances to listed suppliers (Letters of the Ministry of Finance of the Russian Federation dated 08.12.2011 No. 03-03-06 / 1/816, dated 30.06.2011 No. 07-02-06 / 115, dated 17.06.2009 No. 03-03-06 / 1 / 398);

- on penalties for violation of the terms of the agreement (Letters of the Ministry of Finance of the Russian Federation dated June 15, 2012 No. 03-03-06 / 1/308, dated September 29, 2011 No. 03-03-06 / 2/150);

- on the amounts of interest collected by the arbitration court for the use of other people's funds (Letter of the Ministry of Finance of the Russian Federation of July 24, 2013 No. 03-03-06 / 1/29315);

- under loan agreements (Letter of the Ministry of Finance of the Russian Federation dated 04.02.2011 No. 03-03-06 / 1/70).

2. The debt repayment period established by the agreement has expired. If the term is not established in the agreement or the agreement was not concluded in writing, then it can be determined on the basis of the law, other legal acts, business customs, other conditions or the essence of the obligation (clause 2 of article 314, clause 1 of article 486 Civil Code of the Russian Federation).

3. The debt is not secured by a pledge, surety, bank guarantee.

For purposes accounting the conditions for recognizing accounts receivable as doubtful are established by the Regulations on accounting and financial reporting in the Russian Federation No. 34n (paragraph 2, clause 70):

- Debtors' debts, regardless of the nature of their occurrence, have not been repaid on time or which, with a high degree of probability, will not be repaid on time.

- Debt is not secured by guarantees.

! Note: in accounting and tax accounting, the criteria for recognizing doubtful receivables differ.

Bad accounts receivable

Thus, in respect of doubtful accounts receivable, there is a possibility that it will be settled. But hopeless (unrecoverable) accounts receivable practically excludes such a possibility. Accounts receivable are recognized hopeless if she answers at least one of the following signs (clause 2 of article 266 of the Tax Code of the Russian Federation):

1. The statutory limitation period has expired with respect to the debt.

2. The debtor's obligation was terminated due to the impossibility of its fulfillment, on the basis of an act of a state body or liquidation of the organization.

3. The impossibility of collecting receivables was confirmed by the decision of the bailiff-executor on the end of the enforcement proceedings in the event of the return of the executive document to the recoverer on the following grounds:

- it is impossible to establish the location of the debtor, his property, or to obtain information about the availability of funds and other valuables belonging to him,

- the debtor does not have property on which a claim can be levied, and all measures taken by the bailiff-executor permissible by law to find his property turned out to be ineffectual.

! Note: If several of the listed conditions are fulfilled in relation to accounts receivable, it is recognized as hopeless in the tax (reporting) period when the first condition arose (Letter of the Ministry of Finance of Russia dated 22.06.2011 No. 03-03-06 / 1/373).

The most common reasons for classifying a receivable as hopeless are the liquidation of the debtor organization and the expiration of the limitation period. In the event of liquidation of the debtor, the debt is recognized as unrealistic to be collected from the moment the organization is excluded from the Unified State Register of Legal Entities, which is confirmed by an extract from the Register. The procedure for recognizing receivables as hopeless due to the expiration of the limitation period is not so clear, so I propose to dwell on it in more detail.

Limitation period

In general, the limitation period is three years (Article 196 of the Civil Code of the Russian Federation). The course of the limitation period begins from the date of the end of the term for the fulfillment of obligations by the debtor (payment term) established in the contract. If the contract establishes the procedure for payment in parts, then the limitation period is calculated in relation to each part separately. If the deadline for the fulfillment of obligations has not been established, the limitation period begins to be calculated from the moment the debtor is presented with a demand for the fulfillment of obligations.

Example.

The organization LLC "Supplier" shipped the goods to the buyer on July 28, 2014. According to the agreement with the buyer, the final payment date was set on August 15, 2014. However, the buyer did not pay for the goods within the set period. In this case, the limitation period will begin on August 16, 2014 and will end on August 15, 2017.

To classify a debt as hopeless, it must be borne in mind that the course of the limitation period may be interrupted in cases of recognition by the debtor of its obligations. After the interruption, the course of the limitation period begins anew. The following actions testify to the recognition by the debtor of his obligations:

- recognition of a claim (requesting a deferred payment, signing a debt reconciliation statement, a statement on offsetting mutual claims);

- partial payment by the debtor of the principal or interest on the principal;

- amendment of the contract, from which it follows that the debtor recognizes the existence of a debt (for example, a deferral, payment by installments).

! Note: you can go to court even after the statute of limitations has expired. However, the debtor's statement on the application of the limitation period will serve as the basis for refusing the claim.

The presence of a counterclaim

It often happens that the same counterparty is both a creditor and a debtor at the same time. In this case, the question arises: can such a receivable be considered uncollectible, despite the presence of a counter payable? The Ministry of Finance of the Russian Federation believes that it is impossible, since the organization can carry out and, thus, pay off the obligations of the debtor (Letter of the Ministry of Finance dated 04.10.2011 N 03-03-06 / 1/620). However, the position of the judiciary is the opposite: a receivable can be recognized as hopeless regardless of the existence of a counter claim against the debtor. Indeed, in accordance with the Civil Code of the Russian Federation, offset is a right, not an obligation, which can be used by sending a corresponding statement to the counterparty, and even unilaterally. And yet, in order to avoid the claims of the regulatory authorities, it is safer to recognize as hopeless only that part of the receivable that is not covered by the counter payable.

So, we examined the criteria for recognizing doubtful and uncollectible receivables. In order to assess the likelihood of repayment of each debt separately and refer it to one type or another, carry out. And based on the results of the inventory, a decision is made to create, as well as Fr. Thus, the correct determination of the amount of doubtful and bad accounts receivable will allow you to avoid serious violations of accounting and tax accounting.

Do you find the article useful and interesting - share with colleagues on social networks!

There are comments and questions - write, we will discuss!

Yandex_partner_id = 143121; yandex_site_bg_color = "FFFFFF"; yandex_stat_id = 2; yandex_ad_format = "direct"; yandex_font_size = 1; yandex_direct_type = "vertical"; yandex_direct_border_type = "block"; yandex_direct_limit = 2; yandex_direct_title_font_size = 3; yandex_direct_links_underline = false; yandex_direct_border_color = "CCCCCC"; yandex_direct_title_color = "000080"; yandex_direct_url_color = "000000"; yandex_direct_text_color = "000000"; yandex_direct_hover_color = "000000"; yandex_direct_favicon = true; yandex_no_sitelinks = true; document.write ("");

Legislative and Regulatory Acts:

1. Tax Code of the Russian Federation

2. Civil Code of the Russian Federation

RF Codes can be found at http://pravo.gov.ru/

3. Letters of the Ministry of Finance of the Russian Federation:

- dated 08.12.2011 No. 03-03-06 / 1/816,

- dated 30.06.2011 No. 07-02-06 / 115,

- dated 17.06.2009 No. 03-03-06 / 1/398

- dated 15.06.2012 No. 03-03-06 / 1/308,

- dated 29.09.2011 No. 03-03-06 / 2/150,

- dated 24.07.2013 No. 03-03-06 / 1/29315,

- dated 04.02.2011 No. 03-03-06 / 1/70,

- dated 22.06.2011 No. 03-03-06 / 1/373,

- dated 04.10.2011 No. 03-03-06 / 1/620

The documents of the financial department can be found at the official http://mfportal.garant.ru/

Receivables - debts of other organizations, employees and individuals of this organization (debts of buyers for purchased products, accountable persons for the sums of money issued to them on account, etc.). Organizations and persons who owe this organization are called debtors.

The economic essence of receivables acts as funds temporarily diverted from the company's turnover. This distraction can provoke additional demand for resources and lead to financial stress.

Upon expiration of the limitation period, receivables and payables are subject to write-off. The general limitation period is set at three years. For certain types of claims, the law may establish special limitation periods, reduced or longer than the general period.

The limitation period begins to be calculated at the end of the term for the performance of obligations, if it is determined, or from the moment when the creditor has the right to file a claim for the performance of the obligation.

Accounts receivable after the expiration of the limitation period are written off to reduce profits or allowance for doubtful debts.

Accounts receivable can be viewed in three senses: firstly, as a means of paying off accounts payable, secondly, as part of the products sold to customers, and thirdly, as one element of current assets, an important part of the organization's working capital.

Accounts receivable are classified into various views depending on the economic content of the obligations, on the duration (term of provision), on the timeliness of payment.

Types of accounts receivable in accordance with its classification features are presented in Figure 1.

Fig. 1- Classification of receivables

By the content of obligations accounts receivable may be associated with the sale of products, goods, works, services (debt for products, goods, works and services, including those secured by promissory notes) and not related to it (debt on settlements with the budget, on rent, on advances issued, on accrued income, on internal settlements, other debt).

By duration debt is divided into short-term and long-term. Accounts receivable are presented as current if their maturity date is not more than 12 months after the reporting date. The rest of the receivables are presented as long-term.

On time payment accounts receivable can be divided into normal and overdue. Debt is considered normal if the due date has not arrived. And the overdue debt is considered to be for goods, works, services that have not been paid for within the period specified in the contract.

Overdue accounts receivable can be doubtful and hopeless.

Tax legislation gives a definition of doubtful debt: “A doubtful debt is any debt to a taxpayer arising in connection with the sale of goods, performance of work, provision of services, if this debt is not repaid within the terms established by the contract and is not secured by a pledge, surety, bank guarantee ”.

Bad debts are those debts to an organization for which the limitation period has expired, as well as those debts for which the obligation is terminated due to the impossibility of its performance, or on the basis of an act of a state body or liquidation.

Creditor's call the debt of this organization to other organizations, employees and persons who are called creditors.

Accounts payable after the expiration of the limitation period are written off to financial results.

Accounts payable classified depending on the content of obligations, on the duration and possibility of fulfilling obligations. The types of accounts payable are shown in Figure 2.

By the content of obligations accounts payable may be associated with the purchase of inventories, works, services (debt for purchased products, goods, works and services, including amounts on bills presented for payment) and is not related to it (debt on settlements with the budget, debt to subsidiaries and dependent companies, to the personnel of the organization, to the participants (founders) for the payment of income, other debts).

Rice. 2 - Classification of accounts payable

By time subdivided into long-term and short-term. In a broad sense, the composition of accounts payable includes any debt of an organization to anyone else. Long-term debt includes debt on long-term loans and borrowings. But it is known that loans and credits in Russian accounting and reporting are separated from accounts payable and are classified as long-term and short-term liabilities. Nevertheless, in many literary sources from an economic and legal point of view, all types of debt and credit obligations are included in accounts payable.

If possible, fulfillment of obligations debt to creditors can be divided into normal and overdue.

At the same time, two types of debt can be distinguished as part of overdue accounts payable: debt, the statute of limitations for which has not expired, and unclaimed debt (with expired statute of limitations).

To this classification, it can be added that as part of the obligations of any organization, it is conditionally possible to distinguish also urgent debt (debt to the budget for wages, social insurance and security) and ordinary (liabilities to subsidiaries and dependent companies, advances received, promissory notes payable, etc. creditors; debts to suppliers). This classification is often used in economic analysis.

A common feature of accounts payable and receivable is that they are based on the time lag between a commodity transaction and its payment.