Advance payments. How to calculate monthly advance payments for income tax during the reporting period

Organizations that do not have the right to pay only quarterly advances on income tax and have not voluntarily switched to monthly advance payments based on actual profits, in 2019 must pay monthly advance payments calculated based on the data of the previous quarter, with an additional payment based on the results of the quarter.

Newly created companies begin to pay monthly advances after the expiration of a full quarter from the date of registration, if their revenue exceeded the limit established by the Tax Code of the Russian Federation (clause 6 of Article 286 of the Tax Code of the Russian Federation) and the payment of advances on actual profits was not initially chosen.

Calculation of accrued advance payment/tax based on the results of the quarter/year

These amounts are considered a cumulative total from the beginning of the year and are reflected in the Income Tax Declaration (approved by Order of the Federal Tax Service dated October 19, 2016 No. ММВ-7-3/572@) as follows:

Calculation of the amount due monthly in the next reporting period (quarter)

During the first quarter of the current year, the organization pays monthly advances in the same amount as they should have been paid during the fourth quarter of the previous year (clause 2 of article 286 of the Tax Code of the Russian Federation).

The amount of advances transferred monthly to the budget during the 2nd, 3rd and 4th quarters is calculated as follows:

Every month you need to transfer 1/3 of the amount calculated using the above formulas.

Calculation of the amount of advance/tax to be paid additionally to the budget based on the results of the reporting period/year:

Please note that we have provided general formulas for calculating advance/tax. For organizations paying trade tax, as well as for organizations paying tax outside the Russian Federation, the amount of which is counted towards the payment of income tax, the advance/tax is calculated slightly differently.

Example

To determine the advance transferred to the budget monthly during a certain quarter, you need to divide the amount of monthly advances for this quarter by 3. For example, the organization must transfer no later than 10/28/19, 11/28/19 for 26,667 rubles, 12/30/19 - 26,666 rub. (RUB 80,000/3). In addition, do not forget to distribute the advance amount between the federal and regional budgets. For example, no later than November 28, 2019, the company must pay 4,000 rubles to the federal budget. (RUB 26,667 x 3%/20%), regional - RUB 22,667. (RUB 26,667 x 17%/20%).

What to consider when calculating and paying advance payments

1. Declarations reflect only accrued amounts (and not actually paid). For example, if every month during a quarter you were supposed to transfer 10,000 rubles, but in fact you paid only 7,000 rubles, then when calculating the advance payment subject to additional payment at the end of this quarter and reflecting it in the declaration, 30,000 is still taken into account rub. (RUB 10,000 x 3).

2. If the amount of monthly advances and the advance accrued for the previous period exceeded the amount of the advance payment/tax calculated based on the results of the reporting/tax period, then based on the results of this reporting/tax period you do not need to pay anything to the budget (clause 1 of Art. 287 of the Tax Code of the Russian Federation). For example, the amount of the advance for the first quarter was 15,000 rubles, during the second quarter you transferred monthly advances totaling 15,000 rubles, and at the end of the first half of the year the amount of the advance was equal to 20,000 rubles, then 10,000 rubles. - essentially your overpayment (20,000 rubles - 15,000 rubles - 15,000 rubles).

Cash flows in the form of income taxes are significant payments that fill the federal and regional budgets. The tax period for income tax is significant - a calendar year. But the state is not willing to wait that long to get its share of the pie. Therefore, during the year the legislator provided for the payment of advance tax payments. And it is easier for an organization to pay taxes in installments.

Calculating advance payments based on profits seems simple at first glance. But, firstly, you need to reasonably select the appropriate calculation option, fixing it in the accounting policy (quarterly or based on actual profit). Secondly, the quarterly calculation has its own subtleties with advance payments, which sometimes confuse the accountant. Let's look at this in detail in two approaches. In this article we will discuss the calculation rules. Using specific examples, we will make calculations and enter the required amounts into the declaration.

1. Who pays advances on profits

2. Types of advance payments

3. Calculation of advance payments based on quarterly profits

4. Monthly advances on profits based on estimated profits for the previous quarter

5. Examples of calculating advance payments by quarter

6. Subtleties of calculating advance payments

7. Monthly advances on profits based on actual profits

8. Advance payments in the income statement

9. Deadlines for payment of advances on profits

So, let's go in order.

1. Who pays advances on profits

Almost all income tax payers pay advances on profits. In this case, neither the size nor the nature of the company’s activities, nor the calculated amount of tax matters.

The list of those who do not pay advance income tax payments is not long. Such organizations are directly listed in the Tax Code of the Russian Federation. These are budgetary institutions such as libraries, concert organizations, museums, and theaters.

2. Types of advance payments

There are 3 types of advances on profits (Article 286 of the Tax Code), which can be roughly called:

- Quarterly payments

- Monthly payments based on estimated profit,

- Monthly payments calculated based on the actual profit received by the organization for the month.

Data on the frequency of advance payments and submission of declarations are given in Table 1.

Table 1

3. Calculation of advance payments based on quarterly profits

Typically, calculating advance payments based on quarterly profits (quarterly advance payments) does not cause any difficulties for an accountant. You just need to know the basic rules:

- The right to pay only quarterly advance payments has organizations that have revenue for the previous 4 quarters did not exceed an average of 15 million rubles per quarter without VAT. For newly created organizations, sales revenue should not exceed 5 million rubles per month or 15 million rubles per quarter (Example 1).

- The right to pay only quarterly advance payments is also from some other legal entities listed in paragraph 3 of Article 286 of the Tax Code of the Russian Federation - budgetary and autonomous institutions, non-profit organizations that do not have income from the sale of goods (works, services), participants in simple partnerships and some others.

- Advances on profit for the quarter are considered based on the tax base for the reporting period. The amount payable is obtained as the difference between the calculated advance for the reporting period and the advance determined for the previous reporting period (Example 4).

Example 1

It is necessary to determine whether the company has the right to make quarterly payments if the revenue excluding VAT is:

1st quarter of 2017 - 25 million rubles,

2nd quarter 2017 - 8.5 million rubles,

3rd quarter of 2017 - 9.5 million rubles,

4th quarter of 2017 - 29 million rubles,

The average revenue for 4 quarters is checked.

Average revenue for 4 quarters = (25 + 8.5 + 9.5 + 29) / 4 = 18.0 million rubles.

Conclusion - from the 1st quarter of 2018, the organization is obliged to pay monthly income tax payments.

4. Monthly advances on profits based on estimated profits for the previous quarter

The rules for calculating monthly advance payments for each quarter are given in paragraph 2 of Article 286 of the Tax Code of the Russian Federation.

For ease of understanding, we will use calculation formulas, conventionally denoting:

- AMn – monthly advance payment for the nth quarter,

- АКn – quarterly advance payment for the nth quarter,

- n – quarter number from 1 to 4.

Formulas for calculating advance payments of profit by quarter:

- Monthly advance payment in 1st quarter

AM1 = AM4, where AM4 is the monthly payment of the 4th quarter of the previous year,

- Monthly advance payment in 2nd quarter

AM2 = AK1 / 3,

- Monthly advance payment in 3 quarter

AM3 = (AK2 - AK1) / 3,

- Monthly advance payment in 4th quarter

AM4 = (AK3 - AK2) / 3.

When preparing a declaration for the reporting period, the actual data obtained for the period are analyzed. If the calculated advance payment for the current quarter is greater than the total quarterly and monthly payments paid, then an additional payment of the quarterly advance payment is required in the amount of the difference.

5. Examples of calculating advance payments by quarter

Example 2

According to the declaration for the half-year, monthly advance payments due in the 3rd quarter amounted to 10 thousand rubles. per month. According to the declaration for 9 months, the calculated advance payment is 55 thousand rubles, quarterly payments for the last quarter are 10 thousand rubles. Calculate the quarterly surcharge taking into account the monthly advance payments paid.

- - 10 - 3 * 10 = 15 thousand rubles.

If suddenly the amounts of advances paid turn out to be more than those calculated for the reporting period, then advance payments based on the results of the reporting period are counted against the tax payment based on the results of the next reporting (tax) period (clause 1 of Article 287 of the Tax Code of the Russian Federation).

But the Declaration indicates estimated data for monthly advance payments for the next period.

Example 3

According to the declaration for the half-year, monthly advance payments due in the 3rd quarter amounted to 20 thousand rubles. per month. According to the declaration for 9 months, the advance payment is 50 thousand rubles, quarterly payments for the last quarter are 10 thousand rubles. Determine what data needs to be reflected in the Declaration for 9 months.

- – 10 – 3 * 20 = – 20 thousand rubles. - there was an overpayment.

Such overpayment is reflected in lines 280,281 of Sheet 02 of the Declaration. The overpayment can be offset against the tax payment based on the results of the next reporting (tax) period (clause 1 of Article 287 of the Tax Code of the Russian Federation).

6. Subtleties of calculating advance payments

1. Only in the declaration for 9 months the amounts of advance payments for the 4th quarter of the current and 1st quarter of the next year are determined (lines 320, 330, 340 of Sheet 02 of the Declaration).

If, when preparing a declaration for 9 months, the limit is 15 million rubles. has not been exceeded, planned monthly payments are not reflected in the declaration.

But if suddenly (as in our example) based on the results of the declaration for the year, the specified limit is exceeded, then in the opinion of the regulatory authorities, planned monthly advance payments should be reflected in the declaration for 9 months (Letter of the Ministry of Finance of the Russian Federation dated December 24, 2012 N 03-03-06/ 1/716).

From the text of the letter we can conclude that you will need to submit an updated declaration within 9 months. Otherwise, the Federal Tax Service simply has nowhere to find out the amount of monthly advance payments that the organization will need to pay in the 1st quarter.

There is another point of view - do not submit an updated declaration for 9 months, reflect the monthly advance payments of the 1st quarter only in the declaration for the year. But then we will violate the provisions of clause 5.11 of the Order of the Federal Tax Service of Russia dated October 19, 2016 N ММВ-7-3/572@, which determines the procedure for filling out the declaration. After all, it clearly states that lines 290-310 in the declaration for the tax period are not filled out.

2. When keeping records in the 1C program it is necessary to reflect in the settings the fact of the transition to paying monthly advance payments (Main - Tax and reporting settings - Income tax - Procedure for paying advance payments - select “Monthly according to estimated profit”).

3. The calculation of lines 210 (220 and 230) includes both quarterly (lines 180 (190, 200)) and monthly (lines 290 (300, 310)) advance payments reflected in the declaration for the previous reporting period.

For an example of calculating monthly payments, see the video.

7. Monthly advances on profits based on actual profits

In this case, it is necessary to submit a notification to the Federal Tax Service about the transition to monthly advance payments based on actual profits. The notification is submitted for the next year no later than December 31 of the current year.

With this method, the Declaration is submitted monthly, the advance is calculated based on the actual profit for the month.

In the event of a transition to paying monthly advance payments based on the actual profit received, the reporting periods will be one month, two months, three months, and so on until the end of the calendar year (Clause 2 of Article 285 of the Tax Code of the Russian Federation).

Calculation of advance payments on profit can be done using the formula:

AM of the reporting period = Tax base of the reporting period x Tax rate.

Each time at the end of the reporting period, the amount to be paid is determined:

AM for additional payment = AM reporting - AM previous.

8. Advance payments in the income statement

Advance payments in the income statement are reflected in the lines:

- 180 (190, 200) – advance payments for the periods 1st quarter, half year, 9 months,

- 210 (220, 230) – advance payments reflected in lines 180 (190, 200) for the previous reporting period,

- 270, 271 (280, 281) – advances for additional payment (reduction) for the reporting period,

- 290 (300, 310) – monthly advance payments that must be paid in the months following the reporting period,

- 320 (330.340) – monthly advance payments due in the 1st quarter of the next year (these lines are filled in only in the declaration for 9 months).

The main thing to remember when filling out the declaration is that advance payments are reflected as accrued, and not as actually paid. Payment of advance payments on profits is not reflected in the declaration. Filling out the declaration.

9. Deadlines for payment of advances on profits

Payment of advance payments on profits must be made within the time limits established by Article 287 of the Tax Code of the Russian Federation:

- Quarterly advance payments paid no later than the deadline established for filing tax returns for the corresponding reporting period - April 28, July 28, October 28. If the deadline falls on a weekend or holiday, payment is made on the first business day after the weekend or holiday.

- Deadlines for payment of advances on profits for organizations paying monthly advance payments during the reporting period - no later than the 28th day of each month of this reporting period.

- Deadlines for payment of advances on profits for organizations paying monthly advance payments based on the actual profit received, - no later than the 28th day of the month following the month based on the results of which the tax is calculated.

Read and study examples of calculations and filling out advances in the declaration. And if you already have questions on the topic, ask in the comments!

Calculation of advance payments based on profit - general rules

If your reporting periods are the first quarter, six months and nine months of the calendar year, then you are required to make quarterly advance payments. You must calculate advance payments to the budget yourself. This is not difficult to do: you need to calculate the tax base for the reporting period, select the tax rate, and take into account the advance payment for the previous reporting period. In addition, when calculating, you can take into account trade fees and taxes paid outside the Russian Federation, if you paid them.

In which case can only quarterly advance payments of income tax be made?

Organizations that have sales income for the previous four quarters, determined in accordance with Art. 249 of the Tax Code of the Russian Federation, did not exceed an average of 15 million rubles. for each quarter, quarterly advance payments are made (clause 3 of Article 286 of the Tax Code of the Russian Federation).

If the average sales revenue exceeds 15 million rubles, then from the next quarter you will have to pay monthly advance payments in addition to quarterly advance payments (clause 2 of Article 286 of the Tax Code of the Russian Federation).

Also, quarterly advance payments based on the results of the reporting period are paid by the following persons (clause 3 of Article 286 of the Tax Code of the Russian Federation):

- budgetary (except for theatres, museums, libraries, concert organizations) and autonomous institutions;

- foreign organizations operating in the Russian Federation through a permanent representative office;

- non-profit organizations that do not have income from the sale of goods (works, services);

- participants of simple and investment partnerships in relation to the income they receive from participation in simple partnerships and investment partnerships;

- investors of production sharing agreements in terms of income received from the implementation of these agreements;

- beneficiaries under trust management agreements.

Within the quarter, these persons do not pay monthly advance payments. The reporting periods for them are the first quarter, half a year and nine months of the calendar year (clause 2 of article 285, clause 3 of article 286 of the Tax Code of the Russian Federation).

see also

How to calculate quarterly advance payments for income taxes

The quarterly advance payment for income tax is calculated as the product of the tax base for income tax and the income tax rate (clause 2 of Article 286 of the Tax Code of the Russian Federation).

The tax base is the actual profit received, calculated on an accrual basis from the beginning of the year (clause 7 of Article 274 of the Tax Code of the Russian Federation, clause 1 of Article 285 of the Tax Code of the Russian Federation).

Moreover, if you calculate the advance payment at the general rate, then you will also calculate it at the rate for the federal and regional budgets (clause 1 of Article 284 of the Tax Code of the Russian Federation).

Quarterly advance payments for six months and nine months are reduced by the amount of the advance payment that was accrued for the previous reporting period (clause 1 of Article 287 of the Tax Code of the Russian Federation).

- for the amount of the trade fee actually paid from the beginning of the tax period until the date of payment of the advance payment, if you pay the trade fee (clause 10 of Article 286 of the Tax Code of the Russian Federation);

- the amount of tax paid outside the Russian Federation (clause 3 of Article 311 of the Tax Code of the Russian Federation).

It should be remembered: if you received a loss during the reporting period, then the tax base will be equal to zero (clause 8 of Article 274 of the Tax Code of the Russian Federation).

See also:

Calculation of advance payments for income tax for the first quarter

In addition, the advance payment can be reduced:

Tax calculation at the end of the year

Profit tax at the end of the year is determined as the product of the tax base for profit tax and the tax rate minus the advance payment accrued for nine months (clause 1, article 274, clause 1, article 285, clauses 1, 2, art. 286, paragraph 1 of Article 287 of the Tax Code of the Russian Federation):

In addition, the tax can be reduced:

- on the amount of the trade fee actually paid from the beginning of the tax period until the date of payment of the tax, if you pay the trade fee (clause 10 of Article 286 of the Tax Code of the Russian Federation);

- the amount of tax paid outside the Russian Federation (clause 3 of Article 311 of the Tax Code of the Russian Federation).

If the amount of tax calculated at the end of the tax period is less than the amount of advance payments calculated during the year, then you do not pay tax at the end of the year (clause 1 of Article 287 of the Tax Code of the Russian Federation).

See also:

An example of calculating quarterly advance payments for income tax

Alpha LLC pays only quarterly advance payments. The tax rate is 20% (3% to the federal budget and 17% to the regional budget).

The organization received as a result:

- I quarter profit in the amount of 250,000 rubles;

- half-year loss of 100,000 rubles;

- nine months profit of 500,000 rubles.

Quarterly advance payment based on the results of the first quarter - 50,000 rubles. (250,000 x 20%):

- to the federal budget 7,500 rubles. (250,000 x 3%);

- to the regional budget 42,500 rubles. (250,000 x 17%).

The quarterly advance payment and the amount payable at the end of the half-year will be equal to zero, since at the end of the half-year a loss of 100,000 rubles was received. (clause 8 of article 274 of the Tax Code of the Russian Federation). In addition, the organization incurred an overpayment of 50,000 rubles.

Quarterly advance payment based on the results of nine months - 100,000 rubles. (RUB 500,000 x 20%):

- to the federal budget 15,000 rubles. (500,000 x 3%);

- to the regional budget 85,000 rubles. (500,000 x 17%).

The overpayment based on the results of the half-year is offset against the payment of the quarterly advance payment based on the results of nine months. The advance payment at the end of nine months will be 50,000 rubles. (100,000 rub. - 50,000 rub.):

- to the federal budget 7,500 rubles. (RUB 15,000 - RUB 7,500);

- to the regional budget 42,500 rubles. (RUB 85,000 - RUB 42,500).

See also:

Monthly advance payments for income tax are calculated in the manner established by clause 2 of Art. 286 Tax Code of the Russian Federation. Let's look at the general algorithm and give an example of calculating an advance payment for a month, and also talk about the features of using this procedure in some non-standard situations.

Algorithm for determining the amount of monthly advance payment

On a quarterly basis, the taxpayer calculates the amount of the advance on profits based on data obtained from the actual results of work for the period from the beginning of the year. However, at the same time (if he does not use the right to pay advances only quarterly), he must make payments ahead of this calculation, made monthly on time.

To determine the amount of such payments, clause 2 of Art. 286 of the Tax Code of the Russian Federation establishes the following dependencies:

- the monthly advance payment in the first quarter of the current year is equal to the monthly advance payment in the fourth quarter of the previous year;

- the monthly advance payment paid in the second quarter is equal to 1/3 of the quarterly advance payment for the first quarter of the current year;

- the monthly advance payment paid in the third quarter is equal to 1/3 of the difference between the advance payment for the six months and the advance payment for the first quarter;

- The monthly advance payment paid in the fourth quarter is equal to 1/3 of the difference between the advance payment for 9 months and the advance payment for six months.

Trade tax payers can reduce advance payments of income tax by the amount of trade tax actually paid in relation to the consolidated budget of a constituent entity of the Russian Federation (clause 10 of Article 286 of the Tax Code of the Russian Federation).

Read about where and for whom the trade tax applies in this material. .

What happens to the advance if there is a loss in the quarter?

In one quarter of the tax period, a taxpayer may receive less profit than in the previous one, or a loss. But these circumstances do not exempt the taxpayer from paying monthly advance payments in the current quarter. In such cases, the amount or part of the monthly advance payments paid in the current quarter will be recognized as an overpayment of income tax, which, according to clause 14 of Art. 78 of the Tax Code of the Russian Federation is subject to offset against upcoming payments for income tax or other taxes; for repayment of arrears, payment of penalties or refund to the taxpayer.

If the calculated amount of the monthly advance payment turns out to be negative or equal to 0, then monthly advance payments in the corresponding quarter are not paid (paragraph 6, paragraph 2, article 286 of the Tax Code of the Russian Federation). A similar result obtained based on the results of the third quarter leads to the absence of payment of advances in the fourth quarter of the current year and the first quarter of the next.

Calculation of advance payments during reorganization and when changing the payment procedure

In the event of a reorganization of a taxpayer, during which another legal entity is merged with it, the amount of the monthly advance payment on the date of reorganization is calculated without taking into account the performance indicators of the merging organization (letter of the Ministry of Finance of Russia dated July 28, 2008 No. 03-03-06/1/431).

If a taxpayer changes the procedure for calculating advances, moving from monthly determination of them from actual profit to monthly payments calculated quarterly, then this can only be done from the beginning of the new year (paragraph 8, paragraph 2, article 286 of the Tax Code of the Russian Federation), notifying the Federal Tax Service no later than 31 December of the year preceding the change. The amount of the monthly payment that will have to be paid in the first quarter, in this case, will be determined as 1/3 of the difference between the amount of the advance calculated based on the results of 9 months and the amount of the advance payment received based on the results of the half-year in the previous year (paragraph 10 p. 2 Article 286 of the Tax Code of the Russian Federation).

To learn about the timing of advance payments, read the article “What is the procedure and deadlines for paying income tax (postings)?” .

Example of calculating advance payments

Quarterly advance payments calculated based on the results of the reporting periods of the previous year for the Kvant organization amounted to:

- for half a year - 700,000 rubles;

- for 9 months - 1,000,000 rubles.

In the current year, advance payments based on the results of reporting periods (quarterly) amounted to:

- for the first quarter - 90,000 rubles;

- a loss was incurred for the half-year, as a result of which the advance payment at the end of the half-year was equal to zero;

- for 9 months - 150,000 rubles.

It is necessary to determine the amount of the monthly advance payment that the Kvant organization should pay in each quarter of the current tax period and the first quarter of the next year.

Solution

1. The monthly advance payment payable in the first quarter of the current year is equal to the monthly advance payment that was paid by the Kvant organization in the fourth quarter of the previous year (paragraph 3, paragraph 2, article 286 of the Tax Code of the Russian Federation). Its calculation is carried out in the following order:

(1,000,000 rub. - 700,000 rub.) / 3 = 100,000 rub.

Consequently, in January, February and March, the Kvant organization pays 100,000 rubles each. advances, distributing them among budgets in the required proportion.

Since at the end of the first quarter the actual amount of the advance payment, determined based on the tax rate and the tax base calculated on an accrual basis, amounted to 90,000 rubles, the organization incurred an overpayment of tax in the amount of 210,000 rubles. (RUB 100,000 × 3 - RUB 90,000).

2. Monthly advance payment due in the second quarter of the current year: RUB 90,000. / 3 = 30,000 rub.

The Kvant organization calculated monthly advance payments calculated for the second quarter in the tax return for the first quarter.

Due to the presence of an overpayment based on the results of the first quarter (RUB 210,000), the overpaid amount was offset against the monthly advance payments for the second quarter.

Thus, the overpayment at the end of the second quarter amounted to 120,000 rubles. (RUB 210,000 - RUB 30,000 × 3).

3. The Kvant organization did not pay monthly advance payments in the third quarter (July, August, September), since the difference between the quarterly advance payment for the half-year and the quarterly advance payment for the first quarter of the current year was negative (0 - 90,000 rubles = - 90,000 rubles) (paragraph 6, clause 2, article 286 of the Tax Code of the Russian Federation).

4. Quarterly advance payment for 9 months in the amount of 60,000 rubles. credited towards the overpayment.

5. Monthly advance payment due in the fourth quarter of the current year and the first quarter of the next year:

(150,000 rub. - 0 rub.) / 3 = 50,000 rub.

Thus, in October, November and December of the current year, as well as in January, February and March of the next year, the amount of monthly advance payments will be 50,000 rubles. Since the Kvant organization has overpaid taxes, monthly advance payments can be offset.

Results

The rules for determining the amount of monthly advances paid on profit are established by the Tax Code of the Russian Federation and are described in relation to each quarter. This value is determined for each subsequent quarter by the amount of actually calculated tax attributable to the previous quarter. The monthly advance is taken from this amount as 1/3. Receiving a loss at the end of a quarter eliminates the need for advance payments in the following quarter.

For mandatory payments with a one-year tax period, quarterly advance payments are usually provided. This is necessary to ensure that funds flow into the budget more evenly. Property tax is no exception. Let's look at how to calculate the advance payment for property tax for the 3rd quarter of 2018 and fill out the corresponding reporting form.

General rules for calculating property tax advances

The procedure for calculating and paying property tax for organizations is regulated by Chapter 30 of the Tax Code of the Russian Federation.

In general, the object of taxation is movable and immovable property, recorded on the balance sheet as fixed assets.

The tax period is the calendar year, and the reporting period is periods that are multiples of a quarter.

Before you start calculating the advance payment for property tax for the 3rd quarter of 2018, you should do the following:

- Check whether you need to make this calculation at all. The Tax Code gives the authorities of the constituent entities of the Russian Federation the right to cancel advance payments for property tax both in the region as a whole and for certain categories of taxpayers (clause 3 of Article 379, clause 6 of Article 382 of the Tax Code of the Russian Federation).

- Specify the category of property. For some types of objects, the tax base is determined in a special manner (based on cadastral value).

- Consider the location of objects. If they are located in territories under the jurisdiction of different Federal Tax Service Inspectors, then they should be “segregated” into different reports.

Calculation of advance payments for property tax depending on the category of objects

The procedure for calculating property tax based on the cadastral value is determined by Art. 378.2 Tax Code of the Russian Federation. This method is used to calculate tax for the following objects:

- Business or shopping centers (complexes) and premises inside them. These objects must satisfy the following conditions:

– the permitted use of the land plot under the building involves the placement of office buildings or retail facilities;

– at least 20% of the building’s area must have permitted use as office or retail premises, public catering and consumer services, or actually be used for these purposes.

- Separate non-residential premises that are permitted to be used for offices, trade, consumer services or public catering, or that are actually used for these purposes.

- Real estate objects of foreign organizations not related to work through permanent representative offices.

- Residential buildings and premises that are not included on the balance sheet as fixed assets.

A specific list of “office” and “retail” objects for which property tax is calculated on the basis of cadastral value is determined by the regional authorities at the beginning of each tax period (clause 7 of Article 378.2 of the Tax Code of the Russian Federation).

The advance payment of property tax for the 3rd quarter of 2018 in relation to such objects is determined as 1/4 of their total cadastral value as of 01/01/2018, multiplied by the corresponding tax rate (clause 1, clause 12, article 378.2 of the Tax Code of the Russian Federation).

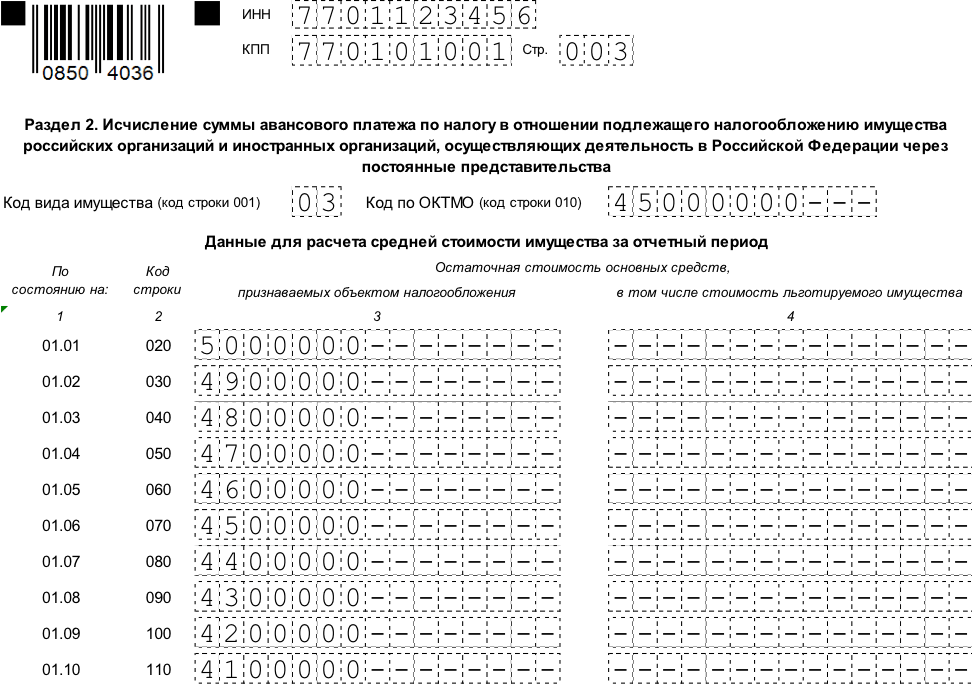

The tax base for all other taxable objects, except for “cadastral” ones, is determined on the basis of their value according to accounting data. The base for 9 months of 2018 is calculated as the sum of the values of the residual value at the beginning of each month, from January to October, divided by 10. The amount of the advance payment will be equal to ¼ of the product of the tax base by the rate established for this category of objects (clause 4 of Art. 382 of the Tax Code of the Russian Federation).

Example.

Alpha LLC owns office space. Its cadastral value at the beginning of 2018 is KS = 10,000 thousand rubles. The residual value of other objects subject to property tax for 9 months of 2018 was:

| date | Residual value, thousand rubles. |

| 01.01.18 | 5 000 |

| 01.02.18 | 4 900 |

| 01.03.18 | 4 800 |

| 01.04.18 | 4 700 |

| 01.05.18 | 4 600 |

| 01.06.18 | 4 500 |

| 01.07.18 | 4 400 |

| 01.08.18 | 4 300 |

| 01.09.18 | 4 200 |

| 01.10.18 | 4 100 |

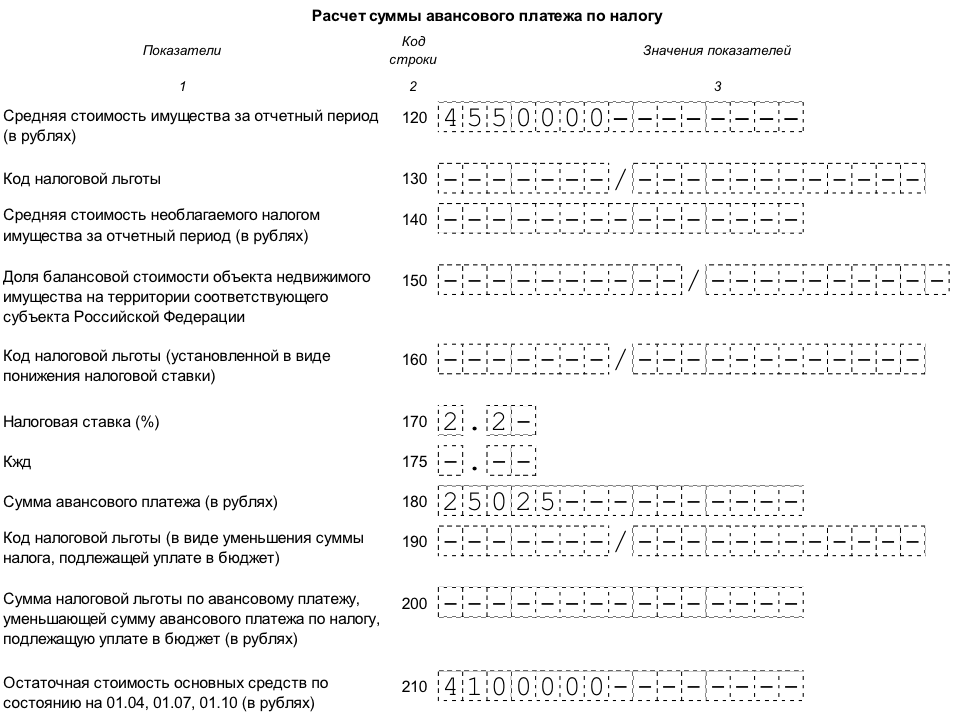

Tax rate for objects taxed at cadastral value – C1 =1.5%, for other taxable property – C2 = 2.2%. The company does not benefit from property tax benefits.

The advance payment for the 3rd quarter of 2018 for “cadastral” objects will be:

APk = ¼ x KS x C1 = ¼ x 10,000 x 1.5% = 37.5 thousand rubles.

Advance payment on objects taxed at average cost:

APs = ¼ x SS x C2 ,

where CC is the average residual value of objects for the period

CC = (5,000 + 4,900 + 4,800 + 4,700 + 4,600 + 4,500 + 4,400 + 4,300 + 4,200 + 4,100) /10 = 4,550 thousand rubles.

APs = ¼ x 4,550 x 2.2% = 25.025 thousand rubles.

The total amount of the advance payment of Alpha LLC for property tax for the 3rd quarter of 2018 will be:

AP = APk + APs = 37.5 + 25.025 = 62.525 thousand rubles.

A sample of filling out a calculation based on example data can be downloaded.

Rules for filling out the calculation of the advance payment for property tax for the 3rd quarter of 2018.

The form for calculating advance payments for property tax and the Procedure for filling out (hereinafter referred to as the Procedure) were approved by order of the Federal Tax Service of the Russian Federation dated March 31, 2017 N MMV-7-21/

The calculation consists of the following sections:

- Title page.

- Section 1, containing information about the advance payment amounts to be transferred to the budget.

- Section 2, in which advance payments are calculated based on the average cost of objects.

- Section 2.1, which deciphers information about real estate objects subject to property tax based on their average value.

- Section 3, which provides information about objects taxed at cadastral value and the calculation of the advance payment for them.

Russian organizations and foreign companies operating through permanent missions must submit all calculation sheets. If there are no indicators, a dash is entered in the corresponding fields. In an abbreviated form (title page, section 1 and section 3), only foreign companies can submit calculations in relation to objects not related to activities through permanent establishments.

Let's look at the rules for filling out individual sheets in the order in which this happens in practice.

Title page

This section can be completed at the beginning of work on the report, with the exception of information on the number of sheets, because it depends on the number of objects whose data is included in the form.

The title page includes general information about the taxpayer:

- TIN and checkpoint codes. In the “KPP” field, you must indicate the code corresponding to the tax authority to which the report is being submitted. This may be a division of the Federal Tax Service at the place of registration of the organization itself, its separate division, or a taxable piece of real estate.

- Correction number. The number in this field indicates whether this report is the first “version” or contains updated data. For the primary form, “0 – -” is indicated in this field, then “1 – -”, “2 – -”, etc. The amended report must be submitted using the “old” form that was in force in the period for which the error was found.

- The reporting period code is indicated in accordance with Appendix 1 to the Procedure. For the 3rd quarter it is “18”.

- The reporting year is entered in a four-digit format, i.e. in this case – 2018.

- The tax authority code is indicated in accordance with the tax registration certificate.

- Calculation submission codes show why the form is submitted to this particular division of the Federal Tax Service. Codes are selected from Appendix 3 to the Procedure. In a “typical” situation, when a Russian organization provides a report at its location, code 214 is used.

- The full name of the organization is indicated in accordance with the constituent documents.

- The field “Reorganization form (code)” is filled in if the calculation is provided by the legal successor. Codes are selected from Appendix 2 to the Procedure. In this case, you must also fill in the “TIN/KPP of the reorganized organization” fields. They contain the codes that were originally assigned to the company.

- The contact phone number must include the country and city code and not contain spaces or other characters other than numbers.

- Number of pages of calculation and supporting documents.

- In the field “I confirm the accuracy and completeness of the information,” information about the responsible person who signed the calculation, his signature and the date of completion is entered. If the form is submitted by a representative, then the details of the power of attorney are indicated in the same field.

- The field “Information on provision of calculation” is filled in by an employee of the Federal Tax Service. It contains information about the method of submitting the form, the date of submission, the number of sheets, the registration number and the signature of the responsible person.

Section 2

This part of the form contains a calculation of the advance payment for property for the 3rd quarter of 2018, for which the tax base is determined by the average cost.

Section 2 is filled out separately according to:

- Types of property in accordance with Appendix 5 to the Procedure.

- Separate divisions with a separate balance sheet.

- Locations of property according to OKTMO codes.

- Tax rates and tax benefits (except for benefits in the form of a reduction in the entire tax amount and a lower tax rate).

When completing section 2:

- Line 001 indicates the code of the type of property from Appendix 5 to the Procedure.

- Line 010 contains the OKTMO code by which the tax will be paid.

- Lines 020 – 110 include information about the residual value of the property as of the 1st day of each month from January to October 2018. In this case, column 3 contains the total cost of taxable objects, and column 4 – the cost of preferential property from column 3.

- Line 120 indicates the average value of property for 9 months of 2018. It is determined by dividing by 10 the sum of the values of lines 020-110 in column 3.

- Line 130 has two parts. The first part contains a seven-digit tax benefit code in accordance with Appendix 6 to the Procedure. If the benefit is established by the law of a constituent entity of the Russian Federation in the form of a reduction in the tax rate (code 2012400) or a reduction in the total amount of tax (code 2012500), then line 130 is not filled in. For other regional tax benefits (code 2012000), the right side of the line is also filled in. It consistently indicates the article, paragraph and subparagraph of the relevant regional law. For each attribute, 4 positions are allocated; “extra” cells in each block are filled with zeros on the left. For example, pp. 3.3 clause 2 art. 11 of the law of the subject of the Russian Federation will be “coded” as follows: 0 0 1 1 0 0 0 2 0 3 . 3

- Line 140 indicates the average value of non-taxable property for 9 months of 2018. It is calculated similarly to the average value of all property on page 120, only the data is taken not from column 3, but from column 4.

- Line 150 is filled in only if the taxable property is located on the territory of several constituent entities of the Russian Federation (property type code 02). This field contains the share of the book value of an object related to a given constituent entity of the Russian Federation.

- Line 160 is filled in if the law of a constituent entity of the Russian Federation establishes a tax benefit in the form of a rate reduction. The first part of the line indicates benefit code 2012400, and the second part contains data on the corresponding article of the regional law, similar to line 130.

- Line 170 indicates the tax rate taking into account the benefits provided

- Line 175 is filled in only if the object is public railway tracks or their integral parts (property type code - 09). In this case, the line will contain a reduction factor Kzd, which is determined in accordance with clause 2 of Art. 385.3 Tax Code of the Russian Federation.

- Line 180 contains the amount of the advance payment for property tax for the 3rd quarter of 2018. In the general case, the difference between the values of lines 120 and 140 is multiplied by the tax rate (line 170) and divided by 4. For railway facilities, the reduction coefficient Kzh from line 175 is additionally applied. For facilities located on the territory of several subjects, the tax amount is determined taking into account the share of the cost object (line 150).

- Line 190 is filled in only if the region has established a benefit in the form of a reduction in the amount of tax payable to the budget. First, the benefit code 2012500 is indicated, and then information about the norm of the regional law, similar to lines 130 and 160.

- Line 200 reflects the amount of this tax benefit.

- In line 210 you need to indicate the residual value of fixed assets as of 10/01/2018. The cost of objects not subject to tax on the basis of paragraphs. 1 – 7 p. 4 tbsp. 374 of the Tax Code of the Russian Federation, is not included in line 210.

Section 2.1

This section allows you to identify real estate objects that are taxed at their average cost. For each such object, a block of lines 010-050 is filled in, containing:

- Lines 010 and 020 indicate the cadastral and conditional number of the object, respectively (if any).

- Line 030 is filled in if there is no data on lines 010 and 020 and contains the inventory number of the object.

- Line 040 indicates the object code in accordance with the OKOF classifier.

- Line 050 contains information about the residual value of the object as of October 1, 2018.

If, as of 10/01/2018, the object was retired for any reason, then section 2.1 for it is not completed.

Section 3

This section contains both information about the “cadastral” objects themselves and the calculation of the amount of the advance payment for them.

- Line 001 contains the code of the type of property, in accordance with Appendix 5 to the Procedure.

- Line 010 contains the OKTMO code by which the tax is paid.

- Line 014 indicates the cadastral number of the building (structure).

- Line 015 contains the cadastral number of the premises, if cadastral registration has been carried out in respect of it.

- Line 020 indicates the cadastral value of the object. If we are talking about premises, the cost of which has not been determined, then the line 020 indicator is calculated based on the cadastral value of the entire building and the share of the premises area given in line 035.

- Line 025 from line 020 separates out the tax-free cadastral value.

- Line 030 is filled in only if the object is in common ownership. It contains information about the taxpayer's share of the right to the object.

- Line 035 indicates the share of the premises' area in the total area of the building. It is filled in if the cadastral value of the premises has not been determined, but the value of the entire building is known.

- Line 040 consists of two parts. The first includes the tax benefit code from Appendix 6 to the Procedure. If the benefit is established by the law of a constituent entity of the Russian Federation in the form of a reduction in the tax rate (code 2012400) or a reduction in the total amount of tax (code 2012500), then line 130 is not filled in. For other regional tax benefits (code 2012000), the right side of the line is also filled in. An example of filling is given in paragraph 5 of the description of section 2.

- Line 050 is filled in if the taxable object is located on the territory of several constituent entities of the Russian Federation. Then the share of the cadastral value that relates to the part of the object located in a given region is entered in the field.

- Line 060 is filled in if the law of a constituent entity of the Russian Federation establishes a tax benefit in the form of a rate reduction. The left side of the field contains benefit code 2012400, and the right side contains details of the article of the regional law, similar to line 040.

- Line 070 contains the tax rate taking into account benefits (if any).

- Line 080 is used only if the object was owned by the taxpayer for part of the reporting period. The coefficient in this case is equal to the number of full months the object was owned, divided by 9.

- Line 90 indicates the amount of the advance payment. In general, this is ¼ of the difference between the values of lines 20 and 25, multiplied by the tax rate (line 070). If necessary, the payment amount is multiplied by additional adjustment factors from lines 030, 050 and 080.

- Line 100 is used if the law of the subject establishes a benefit in the form of a reduction in the amount of payment to the budget. First, the benefit code 2012500 is indicated, and then information about the norm of the regional law, similar to lines 040 and 060.

- Line 110 indicates the amount of the benefit.

Section 1

Completing this section completes the calculation. It contains information about the total amounts of advance payments for property tax payable to the budget.

A section consists of several blocks of lines. Each block indicates the amount of tax payable under a specific OKTMO code. In general, the section contains information about payments according to the codes of municipalities subordinate to the Federal Tax Service, to which the calculation is submitted.

- On line 010 the code OKTMO is indicated.

- Line 020 contains the BCC of the payment.

- Line 030 shows the amount of tax payable. It is calculated by summing the values from all sections 2 and 3 of the calculation for this OKTMO. From sections 2, the difference between lines 180 and 200 is taken, and from sections 3, the difference between lines 090 and 110. Thus, for each OKTMO, payments for all types of property minus benefits (if they are established in a given region) are grouped.

The information in section 1 is certified by the signature of the responsible person.

The procedure for submitting calculations for advance payments of property tax for the 3rd quarter of 2018 and sanctions for its violation

Calculation of advance payments for property tax must be submitted within 30 days after the reporting period (clause 2 of Article 386 of the Tax Code of the Russian Federation). For calculations for the 3rd quarter of 2018, the “deadline” deadline is 10.30.2018

If the number of employees for 2017 exceeds 100 people, then the calculation must be provided electronically. If there are fewer workers, then you can submit the form on paper (Clause 3, Article 80 of the Tax Code of the Russian Federation).

The invoice must be submitted to the location:

- The taxpayer himself.

- Each separate division with a separate balance sheet.

- Each piece of real estate (if it is taxed in a special manner).

The fine for failure to submit a calculation within the prescribed period is 200 rubles. (clause 1 of article 126 of the Tax Code of the Russian Federation). In addition, responsible officials may be fined from 300 to 500 rubles. according to Art. 15.6 Code of Administrative Offences.

But you should not be afraid of blocking your account. Calculation of advance payments is not a tax return, therefore the provisions of paragraph 3 of Art. 76 of the Tax Code of the Russian Federation do not apply to it.

The Tax Code of the Russian Federation does not establish a deadline for the payment of advance payments for property tax. Determining this period falls within the competence of regional authorities (clause 1 of Article 383 of the Tax Code of the Russian Federation).

For example, in Moscow, advance payments for property taxes are paid within the same deadlines established for submitting the calculation. Those. the advance payment for the 3rd quarter of 2018 must be transferred no later than October 30, 2018 (Clause 2, Article 3 of Moscow Law dated November 5, 2003 No. 64).

Conclusion

Calculation of advance payments for property tax for the 3rd quarter of 2018 is submitted by all payers of this tax, with the exception of those who are exempt from paying advances in accordance with the laws of the constituent entities of the Russian Federation. The general procedure for filling out the form and the deadline for submission - until October 30, 2018 - is established at the federal level. Specific lists of taxable objects, tax rates and benefits are determined by regional authorities.