Organization of accounting of fixed assets in the organization. Organization of accounting of fixed assets

Fixed assets can come to the enterprise in one of the following ways:

1.Acquisition for a fee or in exchange for other property;

2.Construction and manufacturing;

3. By making contributions to the authorized capital by the founders;

4.Free receipt;

5. In other cases.

The accounting of the presence and movement of fixed assets belonging to the enterprise on the basis of ownership rights is carried out on the active account 01 "Fixed assets".

Account 01 "Fixed assets" reflects fixed assets at historical cost:

The cost of buildings, structures, equipment, vehicles and other individual items of fixed assets acquired by the enterprise is reflected using account 08 "Investments in non-current assets". This account is used to reflect in the accounting of all costs of the company associated with the acquisition and commissioning of fixed assets, and thus serves as a costing account. Analytical accounting for account 08 is carried out for each acquired or created object.

The inventory value of buildings, structures, equipment, vehicles and other individual items of fixed assets consists of the actual costs of their acquisition and the costs of bringing them to a state in which they are suitable for use for the planned purposes.

Fixed assets acquired for a fee from other enterprises and persons, as well as those created in the enterprise itself, are reflected in the debit of account 01 "Fixed assets" and credit of account 08 "Investments in non-current assets". Fixed assets received from other organizations and persons free of charge are reflected in the debit of account 08 and credit of account 98 "Deferred income" at market value, when the fixed asset received free of charge is put into operation, its value is debited from the credit of account 08 to the debit of account 01 "Fixed funds". Depreciation for these fixed assets is charged in accordance with the generally established procedure, at the same time, debit 98 and credit 91 "Other income and expenses" are posted to the amount of accrued depreciation.

The acceptance for accounting of fixed assets contributed by the founders on account of their contributions to the authorized capital is reflected by posting debit 08 credit 75, then debit 01 credit 08.

When purchasing fixed assets from a foreign supplier (by import), the initial cost of fixed assets is the amount of actual costs of their acquisition. The costs incurred by the organization in foreign currency are reflected in the corresponding accounting accounts in rubles at the exchange rate of the Central Bank of the Russian Federation on the date of the transaction. When the received fixed asset is taken into account, the resulting exchange rate differences are written off to account 91 “Other income and expenses”.

Under a lease agreement for fixed assets, the lessor undertakes to provide the lessee with the property for a fee into temporary possession. The lessor records the leased property on its balance sheet as part of its own fixed assets. The lessee records the property received for temporary use under a lease agreement on off-balance sheet account 001 "Leased Fixed Assets".

An enterprise can independently manufacture or construct items of property, plant and equipment. In this case, the debit of account 08 "Investments in non-current assets" reflects all the actual costs of the enterprise associated with the creation of the object, namely: the cost of the materials used, wages of employees and deductions to non-budgetary funds, the cost of work of third-party organizations, depreciation of the company's fixed assets, used when creating a new item of fixed assets, other expenses. This method of creating fixed assets is called economic.

The organization can also conclude a contract for the creation of fixed assets with a specialized organization. In this case, the debit of account 08 will reflect the cost of work performed in accordance with the contract. This method of creating objects of fixed assets is called contractual.

When purchasing fixed assets, the buyer pays value added tax to the seller in addition to the value of the fixed asset. The amount of VAT on the acquisition of fixed assets is accounted for on b / account 19 subaccount "Value added tax on the acquisition of fixed assets". After the actual payment and in the presence of an invoice, this amount of VAT is debited from the credit b / account 19 -1 to debit b / account 68 "Settlements with the budget".

Subaccount 19-1 "Value added tax on the acquisition of fixed assets", active:

Upon receipt of equipment requiring installation, its cost is reflected in the debit of account 07 "Equipment for installation" in correspondence with account 60 "Settlements with suppliers and contractors". The amount of VAT on the equipment received is reflected in the debit of account 19 "VAT" and the credit of account 60.

The installation of equipment is recorded by the presence of costs in the certificate on the volume of work performed for the installation of this equipment, drawn up in the prescribed manner.

When carrying out construction and installation work in an economic way, the cost of the equipment transferred for installation is debited from the credit of account 07 to the debit of account 08.

Account 07 "Equipment for installation", active:

Accounting for depreciation of fixed assets.

Depreciation(depreciation) is a reflection of the cost of physical and moral depreciation of fixed assets. Depreciation makes it possible to transfer part of the book value of fixed assets to the cost of production.

If materials and raw materials are written off to the cost price as they are written off to production in full, then fixed assets - in parts.

Firstly, this is due to the fact that fixed assets are not transferred directly to products (works, services). Secondly, the service life of fixed assets exceeds one year. Thirdly, the cost of fixed assets, as a rule, is high and its inclusion immediately in the cost price will cause undesirable financial consequences.

Depreciation of fixed assets is carried out in one of the following ways of calculating depreciation charges:

linear way,

diminishing balance method,

method of writing off the value by the sum of the number of years of useful life,

method of writing off the cost in proportion to the volume of products (works, services).

The application of one of the methods for a group of homogeneous objects of fixed assets is carried out during the useful life of the object of fixed assets. The useful life of an item of fixed assets is determined by the organization when the item is accepted for accounting.

The determination of the useful life of an item of fixed assets is based on:

the expected life of this item in accordance with the expected performance or capacity;

expected physical wear and tear, depending on the operating mode (number of shifts), natural conditions and the influence of an aggressive environment, the repair system;

regulatory and other restrictions on the use of this object (for example, the lease period).

In cases of improvement (increase) of the originally adopted normative indicators of the functioning of an item of fixed assets as a result of reconstruction or modernization, the organization revises the useful life of this item.

During the useful life of an item of fixed assets, the accrual of depreciation charges is not suspended, except when they are under reconstruction and modernization by the decision of the head of the organization, and fixed assets transferred by the decision of the head of the organization to conservation for a period of more than 3 months.

Fixed assets worth not more than 2,000 rubles per unit, as well as purchased books, brochures, etc. publications are allowed to be written off to production costs (sales costs) as they are released into production or operation. In order to ensure the safety of these objects in production or during operation, the organization should organize proper control over their movement. Items of fixed assets, the consumer properties of which do not change over time (land plots and natural resources), are not subject to depreciation.

The accrual of depreciation charges for an item of fixed assets begins on the first day of the month following the month of accepting this item for accounting, and is made until the cost of this item is fully paid off or this item is written off from accounting.

The accrual of depreciation charges for an item of fixed assets is terminated from the first day of the month following the month of full repayment of the cost of this item or the write-off of this item from the accounting records.

At linear method, the amount of deductions is the same for the entire period of operation. The second and third methods are non-linear. When they are applied, the amount of depreciation deductions in previous years is greater than in subsequent years.

Using diminishing balance method the annual amount of accrued depreciation is determined based on the residual value of an item of fixed assets taken at the beginning of each reporting year and the depreciation rate calculated when registering this item based on its useful life and the acceleration factor, which is established by the legislation of the Russian Federation. Currently, multiplying coefficients can be applied in accordance with the Decree of the Government of the Russian Federation of 08.19.94 No. 967 (as amended on 06.24.98).

Depreciation is calculated using the following formula:

I = First * (At / 100) * (K1 + K2 + ... + Kn - n + 1), where

AND- depreciation for the reporting period,

First- the initial cost of fixed assets,

On- depreciation rate,

TO- correction factors (applied in case of deviation from the standard conditions for the use of fixed assets).

The depreciation amount for fully depreciated fixed assets is not charged.

Accumulated depreciation for fixed assets is recorded on account 02 "Depreciation of fixed assets", on the credit of which the amount of annual depreciation charges is recorded, and on debit - the accumulated depreciation of sold, liquidated or otherwise disposed of fixed assets.

Account 02 "Depreciation of fixed assets", passive:

Analytical accounting for account 02 "Depreciation of fixed assets" is carried out by type and individual inventory items of fixed assets.

When calculating depreciation, the company transfers part of the cost of fixed assets to the cost of fixed assets, which is equal to the difference between the original (replacement) cost and depreciation.

In the balance sheet, this process is reflected by a decrease in non-current assets, which are accounted for at their residual value.

Depreciation is not charged on:

machinery, equipment and other similar means of labor, which are listed in the enterprise as a commodity or finished product;

housing stock;

objects of external improvement and other similar objects of forestry, road facilities, specialized structures for the navigable environment, etc.;

productive livestock, buffalo, deer;

perennial plantations that have not reached the operational age;

mobilization capacities, unless otherwise provided by the legislation of the Russian Federation.

The accrual of depreciation is suspended at facilities that are undergoing modernization by the decision of the head of the organization - as works on their restoration with a period of more than 12 months (previously - with a period of 3 months).

Thus, depreciation is charged on all items of property, plant and equipment during their useful life, except for the time the items are located at:

conservation for more than three months. In this case, the order of conservation is established by the head of the organization, and it acts in relation to objects located in a certain complex, or objects with a complete production cycle;

restoration (carrying out work on them for reconstruction, modernization, overhaul and other repair and restoration work) with a term of work exceeding 12 months.

Accounting for the costs of maintaining and repairing fixed assets.

In terms of the volume and nature of the repair work performed, they are distinguished capital and Maintenance fixed assets. They differ in complexity, volume and deadlines.

Routine repair consists in daily maintenance of machinery and equipment in order to keep them in working order. The scope of work on current repairs provides for the lubrication and adjustment of individual units and parts, the replacement of some of them with new ones, but without disassembling the unit. For other types of fixed assets (buildings, structures, etc.), other terms and other types of repairs are established (whitewashing, painting, etc.).

Overhaul means:

for equipment and vehicles - complete disassembly of the unit, repair of base and body parts and assemblies, replacement or restoration of all worn out parts and assemblies with new and more modern ones, assembly, regulation and testing of the unit;

for buildings and structures - changing worn-out structures and parts or replacing them with more durable and economical ones that improve the operational capabilities of the repaired facilities, with the exception of the complete replacement of the main structures, the service life of which is the longest in this facility (stone and concrete foundations of buildings, pipes of underground networks , mot supports, etc.).

Repairs of fixed assets can be carried out in an economic way (by the organization itself) or by a contract method (by third-party organizations).

In both cases, a list of defects is created for each repaired object. It indicates:

work to be done

start and end dates of repairs,

parts to be replaced,

time norms for work and production of replaceable parts,

estimated cost of repairs by item of expenditure.

The actual costs associated with the repair or payment for the repair of fixed assets, organizations can debit the accounts for accounting for production costs (20 "Main production", etc.) from the credit of the corresponding material, cash and settlement accounts (account 10 "Materials" , 70 "Payroll calculations", etc.). In the accounts for accounting for production costs and distribution costs, the costs of repairing fixed assets are reflected in the corresponding cost elements (material costs, labor costs, etc.).

For overhaul carried out by a contractor, the organization enters into an agreement with the contractor. Acceptance of the completed overhaul is formalized by the acceptance certificate (form No. OS -3). Completed capital works are paid to the contractor based on the estimated cost of their actual volume.

Organizations can create a repair fund to accumulate funds for the implementation of repair work, especially in organizations with seasonal production. To account for the repair fund, a sub-account "Reserve for the repair of fixed assets" to account 96 "Reserves for future expenses" is opened.

Subaccount "Provision for the repair of fixed assets" to account 96 "Provisions for future expenses", passive:

Account 96 "Reserves for future expenses"

Organizations can initially take into account the costs of repairing fixed assets at the debit of account 97 "Deferred expenses" (from a loan of material, settlement and other accounts), and from this account, as a rule, during the year, evenly write off to production (circulation) costs. It is advisable to use this option for accounting for the costs of repairing fixed assets in those organizations of seasonal industries where the bulk of the costs of repairing fixed assets falls on the first months of the year, when the repair fund has not yet been created.

VAT on expenses for the repair of fixed assets, carried out both in a household and a contract, is accounted for on account 19 in accordance with the generally established procedure. A subaccount "Value added tax on work performed, services rendered" can be opened to this account.

Repair and maintenance of non-production fixed assets is carried out at the expense of the organization's profits. The actual expenses for the repair of such fixed assets are written off to the debit of account 99 "Profits and losses" from the credit of material, cash and settlement accounts (10, 70, 60, 69, 76, etc.). VAT on the repair of non-production fixed assets is written off to the debit of account 99 and does not apply to the reduction of settlements with the budget.

Accounting for transactions on disposal of fixed assets.

The cost of an item of fixed assets that is retired or is not constantly used for the production of products, the performance of work and the provision of services, or for the management needs of the organization, is subject to write-off from the accounting records.

Disposal of an item of fixed assets takes place in the following cases:

sales to other legal entities and individuals;

write-off or liquidation as a result of moral or physical deterioration;

transfers under agreements of exchange, donation and other types of gratuitous transfer of objects;

liquidation of fixed assets in case of accidents, natural disasters and other emergencies;

transfer to the lessee in connection with the transfer of ownership of objects previously leased out with the right to purchase;

non-use for the purpose of manufacturing products or works or for other management needs;

for other reasons.

If an item of fixed assets is written off as a result of its sale, then the proceeds from the sale are accepted for accounting in the amount agreed by the parties in the contract.

Income and expenses from writing off fixed assets from accounting are reflected in accounting in the reporting period to which they relate. Income and expenses from the write-off of fixed assets from the accounting records shall be credited to the profit and loss account as operating income and expenses.

Accounting for transactions on disposal of fixed assets is carried out as follows. On account 01, a sub-account "Disposal of fixed assets" can be opened. The debit of this sub-account of the account reflects the initial value of fixed assets, and the credit - the amount of accumulated depreciation on retired fixed assets. The residual value of the retired fixed asset is written off to the debit of account 91 "Other income and expenses" in correspondence with account 01.

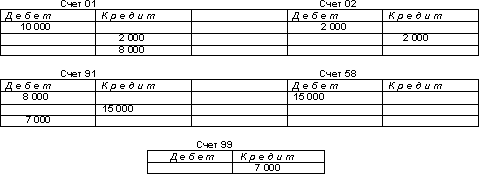

For example, the cost of a retired property, plant and equipment is RUB 10,000. The depreciation amount for this fixed asset at the time of disposal was 2,000 rubles.

Fixed assets transferred as a contribution to the authorized capital of other organizations are reflected at the cost determined by the agreement of the parties, on the debit of account 58 "Financial investments" and the credit of account 91. The initial value of the transferred fixed assets is debited from the credit of account 01 "Fixed assets" in the debit subaccount "Disposal of fixed assets", and the amount of depreciation - the debit of account 02 "Depreciation of fixed assets" and the credit of the subaccount "Disposal of fixed assets". Additional costs associated with the transfer of fixed assets are debited to account 91 from the credit of the respective accounts.

For example, the initial cost of a fixed asset to be contributed to the authorized capital is 10,000 rubles, the amount of depreciation is 2,000 rubles. By agreement of the parties, fixed assets are contributed to the authorized capital at a cost of 15,000 rubles.

2.5 Forms of primary documents for fixed assets accounting.

Fixed assets are accounted for on the basis of the following primary documents:

the act of acceptance and transfer of fixed assets, invoice for the internal movement of fixed assets;

an act of acceptance and transfer of repaired, reconstructed and modernized facilities;

the act of liquidation of fixed assets;

act on the liquidation of vehicles, inventory card for accounting of fixed assets;

fixed asset movement card, inventory list of fixed assets;

fixed asset inventory book.

The receipt of fixed assets is documented by an acceptance certificate, which is drawn up and signed by a commission appointed by the head of the enterprise.

The acceptance certificate indicates:

characteristics of the object of fixed assets;

its location;

the source of financing for its acquisition;

year of manufacture or construction;

commissioning date;

test results, etc.

Simultaneous acceptance(posting) of the same type of tools, machines, household equipment, etc. objects with the same value can be formalized in one act.

Each item of fixed assets, taken into account, is assigned inventory number... It is saved during the entire operation time of the object and is indicated on it (a token is attached, an inscription is made with paint, etc.). It is not allowed to assign inventory numbers of written off fixed asset objects to newly received objects, as this can lead to accounting errors.

The acceptance certificate is transferred to the accounting department, where an inventory card is entered, indicating the inventory number of the object and basic data about it (initial or replacement cost, depreciation rates, depreciation at the time of acceptance).

2. 6. Inventory of fixed assets.

The procedure for the inventory of fixed assets and the reflection of its results in accounting is regulated by the "Methodological Guidelines for the Inventory of Property and Financial Liabilities" (approved by order of the Ministry of Finance of the Russian Federation of 13.06.95).

The purpose of the inventory- to confirm the availability of fixed assets in kind according to the places of their operation or location according to the accounting data.

Inventory of fixed assets is a mandatory procedure in the following cases:

in case of reorganization of the enterprise (merger, division, accession, separation, transformation) as of the date of compilation of the balance sheet);

when changing financially responsible persons (on the day of acceptance and transfer of cases);

after natural disasters (immediately after their end);

upon revealing the facts of theft, as well as damage to such property (immediately after the establishment of such facts);

in other cases stipulated by the legislation of the Russian Federation or regulations of the Ministry of Finance of the Russian Federation.

An inventory of fixed assets can be carried out once every three years, and the book fund of libraries - once every five years.

The head of the enterprise has the right to establish other terms for carrying out the inventory. He also determines the composition of the inventory commission.

Before the inventory, the correctness of the primary accounting documentation for the presence and movement of fixed assets (inventory cards or books, technical passports, acceptance certificates, etc.) is also clarified.

Financially responsible persons must confirm in writing that all incoming and outgoing documents for fixed assets have been handed over to the accounting department. Accepted objects are capitalized, and retired objects are expensed. In the future, such an approach will allow avoiding possible conflicts between members of the inventory commission and persons with financial responsibility.

The actual presence and technical condition of objects are established by members of the inventory commission together with financially responsible persons by direct inspection at the location.

The results of the check are recorded in inventory lists (f. no. inv.-1) manually or by means of computer technology in the context of each name of the object, with the obligatory indication of their inventory number.

Unaccounted fixed assets, as well as fixed assets for which a shortage has been identified, are recorded in a separate inventory list (f. No. inv.-18).

For fixed assets used by the enterprise on a lease basis, regardless of its nature (short-term or long-term), a separate inventory list is drawn up in duplicate. One copy remains with the company, and the other is sent to the address of the lessor.

Objects that are included in the accounting for the active part of fixed assets (machinery, equipment, vehicles) are shown in the inventory list with a detailed decoding of their technical characteristics and factory inventory number.

If the object has undergone restoration, reconstruction, expansion or re-equipment and, as a result, its main purpose has changed, then it is entered into the inventory under the name corresponding to the new purpose.

Inventory lists drawn up accordingly, the commission transfers to the accounting department for compiling a collation sheet. This statement includes only those items for which there are discrepancies with accounting information.

The identified surplus of fixed assets is credited to the debit of account 01 "Fixed assets" and the credit of account 99 "Profits and losses". In case of shortage and damage to fixed assets, the amount of depreciation is written off by posting: debit of account 02 "Depreciation of fixed assets" and credit of account 01. The residual value of fixed assets is debited from the credit of account 01 to the debit of account 94 "Shortages and losses from damage to values". When specific culprits are identified, the missing or damaged fixed assets are assessed at market value and debited from account 94 credit to account 73 debit “Settlements with personnel for other operations”. The difference between the market price and the residual value of fixed assets is reflected in the debit of account 94 and credit of account 98 "Deferred income". As the debt is repaid by its culprit, the corresponding part is debited from account 98 on credit to account 99 “Profits and losses”.

If the specific culprits are not identified, then the missing and damaged fixed assets are debited from the credit of account 94 for production (circulation) costs by decision of the head of the organization.

Fixed assets - part of the property of an organization used as means of labor in the production of products, performance of work or provision of services, as well as for management for a period exceeding 12 months, or a normal operating cycle if it exceeds 12 months.

In accounting, fixed assets with a value of no more than 40,000 rubles can be accounted for as part of inventories. From January 1, 2016, the limit on the value of fixed assets in tax accounting has increased from 40,000 to 100,000 rubles. Fixed assets put into operation from January 1, 2016 are accounted for taking into account the new limit of 100,000 rubles (Federal Law No. 150-FZ dated June 8, 2015).

The unit of accounting for fixed assets is an inventory item:

- a separate item (for example, a safe);

- a single complex of several items that are mounted on a single foundation and have common control (for example, a computer, which includes a system unit, monitor, keyboard, mouse).

You must depreciate items of property, plant and equipment. How to proceed, see account 02 "Depreciation of fixed assets".

Purchase and commissioning of fixed assets

If your organization has acquired fixed assets, then you must account for them on the balance sheet at their original cost. The initial cost is the sum of the actual costs of acquiring an item of property, plant and equipment.

Record the posting of an object of fixed assets on the debit of account 08 "Investments in non-current assets":

DEBIT 08 CREDIT 60 (75-1, 76, 98-2, ...)

- capitalized item of fixed assets.

DEBIT 01 CREDIT 08

Purchase of fixed assets

If your organization has acquired property, plant and equipment for a fee (under a sale and purchase agreement or supply), define their initial cost as the sum of all costs associated with this purchase.

Such costs, for example, can be:

- amounts paid to the seller in accordance with the contract;

- amounts paid for delivery and installation;

- amounts paid for information and consulting services related to the acquisition of this item of fixed assets;

- customs duties and fees;

- non-refundable taxes, state duty paid in connection with the acquisition of an item of fixed assets;

- interest on loans and borrowings received for the acquisition of an item of fixed assets, if it is an investment asset;

- other costs directly related to the acquisition of an item of fixed assets.

The costs of acquiring fixed assets must first be taken into account on the debit of account 08 "Investments in non-current assets" (excluding value added tax):

DEBIT 08 CREDIT 60 (76, ...)

- expenses directly related to the acquisition of an item of fixed assets (excluding VAT) have been taken into account;

then, based on the invoices, reflect the amount of value added tax:

DEBIT 19 CREDIT 60 (76, ...)

- VAT is taken into account on costs directly related to the acquisition of an item of fixed assets.

After the item of fixed assets is put into operation, make a posting on the debit of account 01:

DEBIT 01 CREDIT 08

- the object of fixed assets was put into operation.

Then reflect the value added tax deduction:

- a tax deduction was made.

There are situations when a real estate object needs state registration, but is already in operation.

Until 2011, such objects could be accounted for in two ways: on account 08 “Investments in non-current assets” or on a separate sub-account opened to account 01 “Fixed assets”.

Starting from 2011, temporarily operated real estate objects should be accounted for in the structure of fixed assets (with allocation on a separate subaccount).

The fact of submission of documents for state registration does not matter (clause 52 of the Methodological Instructions for the Accounting of Fixed Assets, approved by Order No. 91n of October 13, 2003).

Depreciation for such fixed assets must be charged in the usual manner: from the 1st day of the month following the month of the registration of the property (letter of the Federal Tax Service of the Russian Federation of August 29, 2011 No. ZN-4-11 / [email protected]).

The fact of filing documents for state registration of property rights for the calculation of depreciation does not matter.

AO Aktiv acquired a warehouse building under a sale and purchase agreement. According to the agreement, the cost of the warehouse is 1,180,000 rubles. (including VAT - 180,000 rubles). 15,000 rubles were paid for the state registration of the building.

DEBIT 60 CREDIT 51

- 1,180,000 rubles. - the seller's invoice has been paid;

DEBIT 08 CREDIT 60

- 1,000,000 rubles. - the building was capitalized on the balance sheet of the organization (excluding VAT);

DEBIT 19 CREDIT 60

- 180,000 rubles. - the amount of VAT is taken into account according to the invoice of the seller;

DEBIT 01 subaccount "Fixed assets that are subject to state registration" CREDIT 08

- 1,000,000 rubles. - the building is accounted for on a separate subaccount;

DEBIT 68 subaccount "Calculations for VAT" CREDIT 19

- 180,000 rubles. - a tax deduction was made.

After the building is ready for commissioning, the "Asset" accountant must make the following entries:

DEBIT 01 CREDIT 01 subaccount "Fixed assets that are subject to state registration"

- 1,000,000 rubles. - the building is included in fixed assets.

Since now state registration takes place after the registration of the real estate object, it is impossible to take into account the costs of paying the state duty in its initial value.

The amount of expenses for payment of the state duty must be taken into account as part of current expenses:

DEBIT 76 CREDIT 51

- 15,000 rubles. - money is transferred to pay for the state registration of ownership of the building;

DEBIT 26 CREDIT 68 subaccount "State duty"

- 15,000 rubles. - the amount of the state duty for the registration of the title to the building is taken into account.

If you use real estate objects that are reflected in your account 08 (it was not transferred to fixed assets in time), for the production of goods, the provision of services or for management needs, then property tax must be charged on such objects (Definition of the Supreme Arbitration Court of the Russian Federation of 25 March 2013 No. VAS-3043/13).

Recall that in accordance with paragraph 6 of PBU 6/01, the unit of accounting for fixed assets is an inventory item. An inventory item of fixed assets is an object with all fixtures and fittings, or a separate structurally separate item designed to perform certain independent functions, or a separate complex of structurally articulated items that are a single whole and designed to perform a certain work. A complex of structurally articulated objects is one or more objects of the same or different purposes, having common fixtures and accessories, general management, mounted on the same foundation, as a result of which each object included in the complex can perform its functions only as part of the complex, and not independently.

Consider how a company should register the purchase of a personal computer in its accounting records.

AO Aktiv acquired a personal computer under a sale and purchase agreement. The invoice indicated the cost of the components of the computer:

- system unit - 33,040 rubles. (including VAT - RUB 5040);

- monitor - 13 570 rubles. (including VAT - 2070 rubles);

- keyboard - 1180 rubles. (including VAT - 180 rubles);

- mouse - 590 rubles. (including VAT - RUB 90).

Total: the cost of a computer is 48,380 rubles. (including VAT - 7380 rubles).

The components of the computer (system unit, monitor, keyboard, mouse) can function only as part of a single complex, therefore the accountant of "Asset" took them into account as a single inventory item and made the following entries:

DEBIT 60 CREDIT 51

- 48 380 rubles. - the seller's invoice has been paid;

DEBIT 08 CREDIT 60

- 41,000 rubles. (48 380 - 7380) - the computer was capitalized on the balance sheet of the organization (at the cost of components, excluding VAT);

DEBIT 19 CREDIT 60

- 7380 rubles. - the amount of VAT is taken into account according to the invoice of the seller.

For the delivery of the computer (236 rubles, including VAT - 36 rubles), "Aktiv" paid additionally in cash from the cash desk through the accountable person:

DEBIT 71 CREDIT 50

- 236 rubles. - money was issued from the cash desk to the accountable person to pay for the delivery of the computer; v

DEBIT 08 CREDIT 71

- 200 rubles. (236 - 36) - delivery charge is included in the book value of the computer (based on the accountable person's advance report);

DEBIT 19 CREDIT 71

- 36 rubles. - VAT included on delivery costs (based on the invoice of the transport organization).

When the computer was put into operation, the accountant of "Asset" made the entries:

DEBIT 01 CREDIT 08

- 41,200 rubles. (41,000 + 200) - the computer is included in the fixed assets of the organization;

DEBIT 68 subaccount "Calculations for VAT" CREDIT 19

- 7416 rubles. (7380 + 36) - a tax deduction was made.

In exchange for the goods, "Aktiv" receives a laptop from LLC "Passive".

DEBIT 45 CREDIT 41

- 35,000 rubles. - the cost of goods shipped under a commodity exchange agreement has been written off;

DEBIT 08 CREDIT 60

- 43,000 rubles. - a laptop received under a commodity exchange agreement was capitalized.

After that, the accountant of "Asset" must reflect the proceeds from the sale of the goods and write off its cost. For the procedure for reflecting these operations, see the typical situations "How to reflect the proceeds under a commodity exchange (barter) agreement" to account 90 "Sales".

If it is impossible to establish the market price of the transferred property, then determine the value of the fixed assets received based on the prices at which the organization acquires similar fixed assets.

Fixed assets must be constantly maintained in working order, which requires certain costs.

Maintenance costs (technical inspection, maintenance, etc.) and all types of repairs (current, average, capital) of fixed assets include the cost of production:

DEBIT 20 (23, 25, 26, 29, 44, ...) CREDIT 10 (60, 69, 70, ...)

- reflects the costs of maintenance and repair of fixed assets.

The costs of all types of repairs are taken into account in taxation of profits in the amount of actual costs. These expenses are included in the cost of production in the reporting period in which they arose (Article 260 of the Tax Code of the Russian Federation).

JSC "Aktiv" performed current repairs of the machine. The repair costs were:

- workers' wages - 1000 rubles;

- contributions to the Pension Fund, Social Insurance Fund, FFOMS and insurance against industrial accidents and occupational diseases, assessed from workers' salaries - 302 rubles;

- cost of purchased parts - 1416 rubles, including VAT - 216 rubles.

The accountant of "Asset" made the entries:

DEBIT 20 CREDIT 70

- 1000 rubles. - the wages of the workers who carried out the repairs were written off to the prime cost;

DEBIT 20 CREDIT 69-1, 69-2, 69-3

- 302 rubles. - contributions to the Pension Fund of the Russian Federation, FSS, FFOMS and contributions for "injury" were written off to the cost price;

DEBIT 71 CREDIT 50

- 1416 rubles. - money was issued from the cash desk to the accountable person to pay for the details;

DEBIT 10 CREDIT 71

- 1200 rubles. (1416 - 216) - parts purchased for the repair of the machine were capitalized;

DEBIT 19 CREDIT 71

- 216 rubles. - VAT included;

DEBIT 68 subaccount "Calculations for VAT" CREDIT 19

- 216 rubles. - VAT is accepted for deduction;

DEBIT 20 CREDIT 10

- 1200 rubles. - written off to the prime cost of the parts used in the repair of the machine.

In total, 2502 rubles were written off to the cost of repairs. (1000 + 302 + 1200). This amount can be fully taken into account when taxing profits.

The original cost of the refurbished property, plant and equipment is not subject to change.

If you decide to revalue fixed assets, then in the future you will need to do this every year.

Revaluation is made by indexation or direct translation at documented market prices.

In this case, the following can be used (clause 43 of the Methodological Instructions for the Accounting of Fixed Assets):

- data on similar products received from manufacturers;

- information on the price level available from state statistics bodies, trade inspections and organizations;

- information about the price level published in the media and special literature;

- assessment by the bureau of technical inventory;

- expert opinions on the current (replacement) value of fixed assets.

However, for property tax purposes, the revaluation results are taken into account.

The revaluation results are taken into account either on account 83 "Additional capital", or are referred to financial results.

note

In tax accounting, the value of fixed assets is formed without revaluation. Depreciation is charged in the same manner and in the same amounts as before the revaluation of fixed assets (Article 257 of the Tax Code of the Russian Federation).

Disposal of property, plant and equipment

If your organization has sold, liquidated, or transferred to another enterprise an item of property, plant and equipment, you must write off its value from the balance sheet of the organization.

As you know, fixed assets are recorded on the balance sheet at their residual value, which is determined as follows:

When writing off an item of fixed assets from the balance sheet, first write off the amount of the accrued depreciation.

To do this, make the wiring:

DEBIT 02 CREDIT 01

- the amount of the accrued depreciation of the item of fixed assets was written off.

Thus, on the debit of account 01, the residual value of the retiring object of fixed assets will be formed. You must refer this amount to the debit of account 91 "Other income and expenses":

DEBIT 91-2 CREDIT 01

- the residual value of the fixed asset has been written off.

To account for the disposal of fixed assets, you can open a separate subaccount "Disposal of fixed assets" to account 01.

If your organization has decided to use the "Disposal of Fixed Assets" subaccount, when writing off an item of fixed assets from the balance sheet, you must make the postings:

DEBIT 01 subaccount "Disposal of fixed assets" CREDIT 01

- written off the initial cost of the item of fixed assets;

- the depreciated value of the item of fixed assets was written off.

If an item of fixed assets is retired, the value of which was increased as a result of the revaluation, then the amount of its revaluation, recorded on account 83 "Additional capital", include in retained earnings:

DEBIT 83 CREDIT 84

- the sum of revaluation of the retired item of fixed assets is included in retained earnings.

If property worth not more than 40,000 rubles is included in fixed assets, then depreciation is charged on it in the usual manner.

In February, Aktiv JSC purchased a pneumatic motor for 17,700 rubles. (including VAT - RUB 2700). Its useful life is 3 years. In accordance with the accounting policy of Aktiv JSC, property worth over 10,000 rubles. takes into account in the structure of fixed assets. The pneumatic motor was put into operation in February.

The "Asset" accountant must make the entries:

in February

DEBIT 08 CREDIT 60

- 15,000 rubles. (17 700 - 2700) - the debt to the supplier is reflected;

DEBIT 19 CREDIT 60

- 2700 rubles. - VAT included;

DEBIT 01 CREDIT 08

- 15,000 rubles. - the pneumatic motor was put into operation;

DEBIT 68 subaccount "Calculations for VAT" CREDIT 19

- 2700 rubles. - accepted for deduction of VAT;

in March

DEBIT 26 CREDIT 02

- 417 rubles. (15,000 rubles: 3 years: 12 months) - depreciation has been charged.

Sale of fixed assets

If your organization decides to sell an item of property, plant and equipment, make the postings:

DEBIT 62 (76) CREDIT 91-1

- reflected income from the sale of fixed assets and the buyer’s debt;

DEBIT 51 (50, ...) CREDIT 62 (76)

- funds have been received from the buyer;

DEBIT 91-2 CREDIT 68 subaccount "Calculations for VAT"

- VAT charged;

DEBIT 01 subaccount "Disposal of fixed assets" CREDIT 01

- written off the initial cost of fixed assets;

DEBIT 02 CREDIT 01 subaccount "Disposal of fixed assets"

- the amount of accrued depreciation has been written off;

DEBIT 91-2 CREDIT 01 subaccount "Disposal of fixed assets"

- the residual value of fixed assets was written off;

- expenses related to the sale of an item of fixed assets have been written off (for example, expenses for dismantling equipment, dismantling a building, etc.).

DEBIT 91-2 CREDIT 01 subaccount "Disposal of fixed assets"

- the residual value of the object of fixed assets to be liquidated was written off;

DEBIT 91-2 CREDIT 23 (20, 25, ...)

- expenses related to the liquidation of an item of fixed assets have been written off (for example, expenses for dismantling equipment, dismantling a building, etc.);

DEBIT 10 CREDIT 91-1

- capitalized materials, scrap received during the liquidation of the object of fixed assets.

The costs of the liquidation of fixed assets reduce the taxable profit of the company (clause 1 of article 265 of the Tax Code of the Russian Federation).

At the end of the month, you must determine the financial result from the liquidation of an item of fixed assets (usually a loss):

DEBIT 99 CREDIT 91-9

- reflected the loss from the liquidation of the object of fixed assets.

1.1 Concept, classification and assessment of fixed assets ... ... ... ... ... ... 8

1.2 Regulatory support for fixed assets accounting ...................... 18

1.3 Analytical review of literature ………………. …… ... ………… .23

Chapter 2 Organization and accounting of fixed assets in LLC "Module" …………………………………………………………………………………………………………………………………………………………………… .33

2.1 Organizational and economic characteristics of LLC "Module" ……………………………………………………………………………… 33

2.2 Documentary accounting of the movement of fixed assets in LLC "Module" …………………………………………………. ………… ..42

2.3 Synthetic and analytical accounting of fixed assets in LLC “Module” ………………………………………………………… .. ……. 48

Chapter 3 Improving the accounting of fixed assets in LLC "Module" ………………………………………………………………………… .61

3.1 Automation of fixed assets accounting …………………………… 61

3.2 Advantages of leasing in LLC “Module” ……………………………………………………………… .70

Conclusion… ... ………………………………………………………………… .80

References …… .. ………………………………………………… ..84

Appendices… .. ……………………………………………………………… ..88

INTRODUCTION

The main production assets of the enterprise are the basis for the production of products, the performance of work, and the provision of services. The activity of the enterprise is not possible without fixed assets. Therefore, accounting for the movement of fixed assets is an integral and important part of the organization of accounting at the enterprise.

Fixed assets are one of the most important factors in any production. Their condition and effective use directly affects the final results of economic activities of enterprises.

The formation of market relations presupposes a competition between various manufacturers, in which those of them who most effectively use all types of available resources will be able to win.

Fixed assets play an important role in the labor process, since they together form the production and technical base of the organization and determine its production potential.

The condition and use of fixed assets and production facilities of the enterprise contributes to the improvement of all its technical and economic indicators: an increase in labor productivity, an increase in capital productivity, an increase in output, a decrease in its cost, and savings in capital investments.

The purpose of the work is to study the theoretical and practical foundations of fixed assets accounting.

To achieve this goal, it is necessary to perform the following tasks:

1) study the theoretical foundations of accounting for fixed assets;

2) study the regulatory framework;

3) check the execution of documents and the reflection in the accounting of the receipt of fixed assets, their internal movement, disposal;

4) study the organization of synthetic and analytical accounting of fixed assets at LLC "Module";

5) identify reserves for improving the accounting of fixed assets and the organization of document flow;

6) identify shortcomings in accounting for the movement of fixed assets at LLC "Module" and give recommendations for their elimination.

The object of the research is LLC "Module".

When performing the thesis, the methods of comparison, observation, comparison, as well as vertical and horizontal analysis were used.

We used legislative regulations, periodicals, textbooks, as well as primary documentation, registers of synthetic and analytical accounting for fixed assets accounting, reporting of LLC "Module".

CHAPTER 1 THEORETICAL BASIS OF FIXED ASSETS ACCOUNTING

1.1 Concept, classification and valuation of fixed assets

The transition to a market economy and the requirements for the competitiveness of products presuppose the technical re-equipment of organizations in different industries, the renewal and reconstruction of fixed assets, the improvement of the use of existing capacities, the acceleration of the replacement of obsolete equipment and the development of newly commissioned capacities. This places new demands on the quality of accounting information on the formation, movement, use and safety of fixed assets.

Fixed assets are the means of labor used by the organization in the production of products, works, services, or necessary in the management of the organization for a period exceeding 12 months.

Fixed assets gradually wear out and transfer their value to the cost of manufactured products, works, services in the form of depreciation deductions. During operation, fixed assets do not change their forms and properties.

The problem of the useful life of objects registered in the organization (at the enterprise) is closely related to the definition of the concept. Useful life is the period during which items of property, plant and equipment must generate income for the organization or serve to fulfill the objectives of its activities. For individual groups of fixed assets, the useful life is calculated based on the amount of production or another natural indicator (the amount of work expected to be received as a result of using this group or a separate object).

To achieve uniformity in the construction of accounting and reporting on fixed assets and the possibility of summarizing data on their availability and movement on the scale of the branches of the economy of the Russian Federation as a whole, the All-Russian Classifier of Fixed Assets (OKOF), introduced since January 1, 1996, is used. funds (funds), that is, assets used repeatedly or continuously over a long period, but not less than a year, for the production of goods, the provision of market and non-market services.

Fixed assets include: buildings, structures, workers and power machines and equipment, measuring and regulating instruments and devices, computers, vehicles, tools, industrial and household inventory and accessories, working, productive and breeding cattle, on-farm roads and other relevant objects.

Buildings (except for residential) - architectural and construction objects, the purpose of which is to create conditions for work, storage of material values, social and cultural services for the population. These include: production buildings of workshops, workshops, warehouses, laboratories, garages, depots, clubs, mobile houses for production (workshops, automatic telephone exchange) and non-production purposes, as well as communications inside buildings necessary for their operation; specialized buildings for the implementation of specific activities, in which the foundations of large-sized equipment, erected simultaneously with the construction of the building, are part of the building for this group.

Structures - engineering and construction objects, the purpose of which is to perform certain technical functions in the production process without changing the subject of labor or for the implementation of various non-production functions. These include oil wells, dams, bridges, complete functional devices for the transmission of energy and information (power lines, heating plants, pipelines, cable communication lines).

Machinery and equipment are devices that convert energy, materials and information. Depending on the main purpose, they are divided into energy (power) and workers.

Energy (power) machines include: machines-generators, machine-motors designed for the production of heat and electrical energy and for converting energy of any kind into mechanical energy (steam boilers, steam machines, turbines, nuclear reactors, various engines).

Working machines and equipment include: machines, apparatus, equipment designed for mechanical, thermal and chemical effects on objects of labor in order to obtain a finished product and to move objects of labor during production. This group also includes all types of technological equipment (automatic machines and equipment), as well as transport, construction, trade, warehouse, agricultural, sanitary and hygienic, water supply and sewerage equipment and other types.

Measuring and regulating devices and devices are designed to measure volume, weight, length, that is, a means of measuring production processes and control (regulation).

Computer equipment - all types of computing and office equipment, as well as equipment for communication systems, communication systems for transmitting information of any kind, means of visual and acoustic display of information, means of storing information.

Vehicles are designed to move people and goods. These include the rolling stock of all types of transport (rail, water, road). It should be noted that cars and trailers, railway cars with a specialized purpose (mobile workshops, power plants, laboratory cars, mobile kitchens, showers) are not vehicles, but are accounted for as buildings or as appropriate equipment.

Industrial and household inventory - means of labor designed to facilitate production processes (work tables, counters, trading cabinets), for storage of liquid and bulk materials (vats, barrels, tanks), as well as office and household items that are not used in the production process (sports equipment, fire-fighting items, that is, objects of classification can only be items that have an independent meaning and are not part of any other object.

Working cattle - horses, oxen, camels.

Perennial plantations - all types of artificial perennial plantings, regardless of their age, breed, including individual fences for each plantation.

We talked about tax accounting of fixed assets in. In this article, we will talk about synthetic and analytical accounting of fixed assets.

Fixed assets in accounting

In accordance with PBU 6/01 "Accounting for Fixed Assets", an asset is accepted for accounting as part of fixed assets, provided that the following conditions are met (clause 4):

- the object is intended for use in the production of products, in the performance of work or the provision of services, for the managerial needs of the organization, or for provision by the organization for a fee for temporary possession or use;

- the object is intended to be used for a long time, that is, for a period longer than 12 months or a normal operating cycle if it exceeds 12 months;

- the organization does not imply the subsequent resale of the object;

- the object is able to bring economic benefits to the organization in the future.

At the same time, they are not fixed assets (clause 3 of PBU 6/01):

- machines, equipment and other similar items that are listed in the warehouses of manufacturing organizations as finished products or in the warehouses of trade organizations as goods;

- items handed over for installation or subject to installation, which are in transit;

- capital and financial investments.

The unit of accounting for fixed assets is an inventory item (clause 6 of PBU 6/01). This ensures the analytical accounting of fixed assets.

Fixed assets in accounting in 2017 with a cost per unit of 40,000 rubles or less PBU for accounting for fixed assets 6/01 allows accounting as part of the inventories (clause 5 of PBU 6/01). Each organization approves the cost criterion independently in its own.

Organization of fixed assets accounting

The procedure for organizing the accounting of fixed assets in accordance with PBU 6/01 is established by the Methodological Guidelines for Accounting for Fixed Assets (approved by Order of the Ministry of Finance dated 13.10.2003 No. 91n).

We can say that the accounting of fixed assets and intangible assets in general is characterized by the unity of approaches. In accounting for these objects, there is a commonality of the principles of initial and subsequent valuation, depreciation, accounting for receipts and disposal. At the same time, however, synthetic accounting of fixed assets is kept on separate account 01 "Fixed assets", and intangible assets - on account 04 "Intangible assets" (). Therefore, the acceptance of fixed assets for accounting is reflected as the debit of account 01 - Credit of account 08 "Investments in non-current assets", and the receipt of intangible assets - Debit of account 04 - Credit of account 08. Answers to the questions of how to keep records of the receipt and disposal of fixed assets are contained not only in PBU 6/01, Methodical Instructions, but also Instructions for the application of the chart of accounts of accounting (Order of the Ministry of Finance dated October 31, 2000 No. 94n).

Fixed assets are accepted for accounting at their initial cost (clause 7 of PBU 6/01). But the procedure for its determination depends on how the object of fixed assets entered the organization (for a fee, free of charge, in exchange for other property, etc.). How to determine the initial cost in such cases is indicated in clauses 8 - 11 of PBU 6/01.

Along with the issues of accounting for the acquisition and disposal of fixed assets, their depreciation is of particular interest, as we talked about.

Typical postings on account 01 when accounting for the receipt of fixed assets, accounting for the disposal of fixed assets, on account 02 during their depreciation, as well as accounting records for revaluation, we considered in.

Let us also remind that the accounting of the lease of fixed assets is kept separately. The rented fixed assets are accounted for by the lessee in accordance with the balance on account 001 "Rented fixed assets", and with the lessor, as a rule, on a separate subaccount to account 01.

Note!

The second of the listed documents is mainly used to determine the useful lives of fixed assets for profit tax purposes, however, paragraph 1 of this Resolution states that the classification can also be used for accounting purposes. Due to the fact that since January 1, 2002, organizations, along with accounting, also maintain tax accounting, then, as a rule, for the purpose of classifying fixed assets, accountants use the Government Decree of January 1, 2002 No. 1 "On the classification of fixed assets included in depreciation groups ", as this allows in some cases to avoid a gap between the data of both types of accounting.

By types, fixed assets are divided into: buildings, structures, workers and power machines and equipment, measuring and regulating devices and devices, computers, vehicles, tools, production and household equipment, and other relevant objects.

Depending on the purpose of use, fixed assets are divided into fixed assets for production and non-production purposes. Fixed assets for production purposes are property directly used for the production and sale of products or for the management of an organization. Non-production fixed assets serve mainly the social sphere of industrial organizations.

On the basis of use, they are distinguished:

· Fixed assets in operation;

· Fixed assets in stock;

· Fixed assets under reconstruction or modernization;

· Fixed assets under conservation.

And the last type of classification provides for the division of fixed assets into own and leased fixed assets.

Account 01 "Fixed assets" is intended for the chart of accounts of accounting approved by Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n "On approval of the Chart of accounts for financial and economic activities of organizations and Instructions for its application". Analytical accounting for account 01 "Fixed assets" is carried out for individual inventory items of fixed assets.

The correct organization of analytical accounting for account 01 "Fixed assets" (as well as for any other synthetic account) largely depends on the Working Chart of Accounts used by the organization for accounting. The development of the Organization's Working Chart of Accounts, which is based on the standard Chart of Accounts proposed by the Ministry of Finance of the Russian Federation for use, is one of the elements of the accounting policy.

The main purpose of the Working Chart of Accounts is that with its help it would be possible to create such an organization's accounting scheme, which would allow not only to provide analytics for all structural divisions of the organization, but to use the information obtained to generate accounting, statistical reporting and use it in others. necessary purposes.

Consider how the structure of account 01 "Fixed assets" should be formed, for example, an industrial organization engaged in the production of furniture - a furniture factory. Suppose that for the purposes of accounting and tax accounting of fixed assets, this organization applies the norms of the Decree of the Government of the Russian Federation dated January 1, 2002 No. 1 "On the classification of fixed assets included in depreciation groups."

The following sub-accounts are opened for this account:

01-1 "Fixed assets for production purposes";

01-2 "Fixed assets for non-production purposes";

01-3 Leased Property, Plant and Equipment.

Analytical attributes of the first level(in accordance with the depreciation groups of the fixed assets):

01-1-1 - the first group (property with a useful life of 1 to 2 years inclusive);

01-1-2 - the second group (property with a useful life from 2 years to 3 years inclusive);

01-1-10 - the tenth group (property with a useful life of over 30 years);

If there are fixed assets on the balance sheet of a furniture factory that were put into operation before January 1, 2002, it is advisable to open another group - the eleventh:

Analytical features of the second level(at the location of fixed assets) for example: a computer used in an office:

01-1-3 "Office";

or a woodworking machine used in a workshop in the production of furniture:

01-1-4 "Main shop";

Analytical features of the third level(by persons responsible for the maintenance and operation of the fixed asset).

Example 1.

Suppose that in the accounting of a furniture factory there is a personal computer used for work as an accountant Ivanova L.I. Then, using this structure of account 01 "Fixed assets" in the accounting of fixed assets will be reflected as follows:

01-1-3 "Office" Ivanova L.I.

End of the example.

ACCOUNTING OF FIXED ASSETS

The rules for the formation of information on fixed assets in the organization's accounting are established by the Accounting Regulations "Accounting for Fixed Assets" PBU 6/01, approved by Order of the Ministry of Finance of the Russian Federation dated March 30, 2001 No. 26n "On approval of the Accounting Regulations" Accounting for Fixed Assets "PBU 6/01 "(hereinafter - PBU 6/01).

To accept assets for accounting as a fixed asset, it is necessary to simultaneously fulfill four conditions established by clause 4 of PBU 6/01:

“A) use in the manufacture of products in the performance of work or the provision of services, or for the management needs of the organization;

b) use for a long time, that is, a useful life over 12 months or a normal operating cycle if it exceeds 12 months ":

As we can see, accounting does not contain a cost criterion for attributing assets to fixed assets, therefore, fixed assets include items regardless of their value, the useful life of which exceeds 12 months.

Note!

Despite the fact that there is no cost criterion for classifying an object as a fixed asset, clause 18 of PBU 6/01 establishes that fixed assets, the cost of which does not exceed 10,000 rubles per unit, are allowed to be written off to production costs as they are released into production or operation. This clause also provides that the organization can set a different cost limit based on the technological features of the OS. Moreover, the established amount of value can be either more or less than 10,000 rubles, but this provision should be enshrined in the order on accounting policy justifying the reasons for establishing such a limit.

The useful life of an asset is the period of time during which the asset is capable of generating income. The determination of the useful life of fixed assets in accordance with paragraph 20 of PBU 6/01 is based on:

· The expected life of this item in accordance with the expected performance or capacity;

· Expected physical wear and tear, depending on the operating mode (number of shifts), natural conditions and the influence of an aggressive environment, the repair system;

· Regulatory and other restrictions on the use of this property (for example, the lease period).

That is, accounting legislation gives organizations some freedom in setting the useful life of fixed assets.

“C) the organization does not expect the subsequent resale of these assets;

d) the ability to bring the organization economic benefits (income) in the future. "

Fixed assets are accepted for accounting at their initial cost, the definition of which depends on the method of receipt of fixed assets in the organization.

The main methods of receipt of fixed assets in organization are:

· Purchase for a fee;

· Receiving from the founders as a contribution to the authorized (pooled) capital;

· Receiving free of charge;

· Manufacturing by own resources;

· Construction by an economic or contractual method;

· Acceptance for accounting of unaccounted objects identified during the inventory.

According to clause 8 PBU 6/01:

“The initial cost of fixed assets purchased for a fee is the amount of the organization's actual costs for the acquisition, construction and manufacture, excluding value added tax and other reimbursable taxes (except as provided for by the legislation of the Russian Federation).

· The actual costs of the acquisition, construction and manufacture of fixed assets are:

· amounts paid in accordance with the contract to the supplier (seller);

· amounts paid to organizations for the performance of work under a construction contract and other contracts;

· amounts paid to organizations for information and consulting services related to the acquisition of fixed assets;

· registration fees, government fees and other similar payments made in connection with the acquisition (receipt) of rights to an item of fixed assets;

· customs duties;

· non-refundable taxes paid in connection with the acquisition of an item of fixed assets;

· remuneration paid to the intermediary organization through which the item of fixed assets was acquired;

other costs directly related to the acquisition, construction and manufacture of an item of fixed assets. In particular, interest on borrowed funds accrued prior to the acceptance of an item of fixed assets for accounting, if they are attracted for the acquisition, construction or manufacture of this item.

General business and other similar expenses are not included in the actual costs of the acquisition, construction or manufacture of fixed assets, unless they are directly related to the acquisition, construction or manufacture of fixed assets.

The actual costs of the acquisition and construction of fixed assets are determined (decreased or increased) taking into account the amount differences arising in cases where payments are made in rubles in an amount equivalent to the amount in foreign currency (conventional monetary units). The sum difference is understood as the difference between the ruble estimate of accounts payable expressed in foreign currency (conventional monetary units) for payment of fixed assets, calculated at the official or other agreed rate as of the date of its acceptance for accounting, and the ruble estimate of this accounts payable, calculated according to the official or any other agreed rate as of the date of its maturity. "

Let's take an example of how the initial cost of a fixed asset is determined when purchased for a fee.

Example 2.

Furniture factory LLC "Krasnoderevshchik" sent its employee to the manufacturing plant in order to purchase a woodworking machine. The cost of production equipment in accordance with the contract amounted to 253,700 rubles. The employee's travel expenses amounted to 2,500 rubles. The cost of delivery of the machine by the services of a third-party organization amounted to 35,400 rubles (including VAT - 5,400 rubles).

The installation and commissioning work was carried out by the workers of the furniture factory, the costs (remuneration of labor adjusters and UST) amounted to 10,000 rubles.

In the accounting of the furniture factory, these transactions were reflected as follows:

|

Correspondence of invoices |

Amount, rubles |

||

|

Debit |

Credit |

||

|

Reflected the cost of purchasing production equipment |

|||

|

Reflected VAT charged by the equipment supplier, payable |

|||

|

Delivery services are included in capital expenditures |

|||

|

Reflected VAT on delivery services |

|||

|

Travel expenses are included in the cost of purchasing fixed assets. |

|||

|

The expenses incurred by the organization to bring the fixed asset to a state suitable for operation are written off as costs for the acquisition of the OS |

|||

|

Woodworking machine put into operation |

|||

|

Paid for equipment to the manufacturer |

|||

|

Paid for delivery services |

|||

|

Accepted for deduction of VAT. |

|||

As a result, on account 01 "Fixed assets" the initial cost of the woodworking machine was formed in the amount of 257,500 rubles.

End of the example.

The cost of fixed assets in accounting is repaid by means of depreciation, and clause 17 of PBU 6/01 establishes a list of objects for which depreciation is not charged.

Accrual of depreciation in accounting in in accordance with paragraph 18 of the accounting standard can be done in one of the following ways:

· Linear method;

· Method of decreasing balance;

· The method of writing off the value by the sum of the number of years of useful life;

· Method of writing off the cost in proportion to the volume of products (works).

Note!

The method of calculating depreciation on fixed assets chosen by the organization during the entire period of its use is not subject to change.

The restoration of an object of fixed assets is carried out through repair, modernization or reconstruction.

The tax accounting of fixed assets is regulated by Chapter 25 of the Tax Code of the Russian Federation (hereinafter referred to as the Tax Code of the Russian Federation), which does not provide such a unified definition of fixed assets as the specified accounting standard PBU 6/01.

However, if we analyze the requirements put forward by Articles 256 and 257 of the Tax Code of the Russian Federation, it becomes clear that the general principles of accounting and tax accounting of fixed assets are practically the same. Therefore, in order to avoid a gap between the data of both accounts, an accountant of a production organization should, in all possible cases, use the same methods for assessing fixed assets, establishing useful lives, calculating depreciation, and the like, especially since some differences that exist in accounting are not difficult to overcome.

The Tax Code of the Russian Federation divides fixed assets into depreciable and non-depreciable. In addition, for tax accounting purposes, depreciable fixed assets are divided into two groups: those subject to depreciation and those not subject to depreciation (the list of fixed assets not subject to depreciation is given in paragraph 2 of Article 256 of the Tax Code of the Russian Federation).

Depreciable property, plant and equipment are those whose value is recovered through depreciation. Moreover, in contrast to accounting, Chapter 25 of the Tax Code of the Russian Federation introduces the cost criterion for classifying property as depreciable, which is 10,000 rubles.

Fixed assets worth up to 10,000 rubles. inclusively, they are not depreciable, and their cost is subject to a one-time inclusion in the composition of material costs at the time of commissioning (according to subparagraph 3 of paragraph 1 of article 254 of the Tax Code of the Russian Federation). Please note that this rule is required. Recall that in accounting, a similar procedure for writing off the value of a fixed asset to costs can be applied only if it is enshrined in the accounting policy. Therefore, in order to avoid differences, it is necessary to use the tax accounting rule in accounting.

The useful life of the depreciable property is determined by the taxpayer independently on the date of commissioning in accordance with the classification of fixed assets approved by the Decree of the Government of the Russian Federation dated January 1, 2002 No. 1 "On the classification of fixed assets included in depreciation groups". Moreover, as we have already noted, paragraph 1 of this Resolution indicates that this classification can also be used for accounting purposes.

This document contains the periods during which one or another fixed asset should be depreciated for profit tax purposes.

Fixed assets are accepted for tax accounting as well as in accounting at their original cost, the procedure for determining which is established by article 257 of the Tax Code of the Russian Federation:

"The initial cost of a fixed asset is determined as the amount of expenses for its acquisition (and if the fixed asset is received by the taxpayer free of charge, as the amount at which such property is valued in accordance with paragraph 8 of Article 250 of this Code), construction, manufacturing, delivery and bringing it to a state in which it is suitable for use, with the exception of the amounts of taxes subject to deduction or accounted for in the composition of expenses in accordance with this Code. "

That is, at first glance, the rules for the formation of the initial cost of fixed assets in accounting and tax accounting are the same. However, for a number of certain points, Chapter 25 of the Tax Code of the Russian Federation contains somewhat different rules in relation to fixed assets, leading to the emergence of irreparable differences between the data of accounting and tax accounting. For example, these are the rules for accounting for interest on borrowed funds raised for the acquisition of fixed assets.

Recall that in accounting, interest on borrowed funds raised for the acquisition of fixed assets, accrued before the object was accepted for accounting, should be attributed to its initial cost (paragraph 8 of PBU 6/01). In tax accounting, such interest is recognized as non-operating expenses (Article 265 of the Tax Code of the Russian Federation). In this regard, for an organization that uses borrowed funds to purchase fixed assets, the initial cost in accounting will almost always differ from the initial cost in tax accounting. The only exception is the case when the borrowed funds are not earmarked. In this case, the accrued interest in accounting will be included in operating expenses, which makes it possible to approximate the data of accounting and tax accounting.

Let's look at an example.

Example 3.

To acquire an industrial building, the furniture factory OOO Krasnoderevshchik took a target loan from the bank in the amount of 2,000,000 rubles at 24% per annum. The loan was received on April 10, 2005. The cost of the building is 2,000,000 rubles (excluding VAT). Payment for the building was made on April 12, 2005. The transfer of the real estate object under the acceptance certificate was made on April 15, 2005. The documents for state registration were submitted on May 12, 2005. The certificate of state registration was received on May 20, 2005. The costs associated with state registration amounted to 7,500 rubles.

The following entries must be made in the accounting records of Krasnoderevshchik LLC:

|

Correspondence of invoices |

Amount, rubles |

||||||

|

Debit |

Credit |

||||||

|

April 2005 |

|||||||

|

Received a targeted loan for the purchase of a property |

|||||||

|

Payment has been made for the property |

|||||||

|

The real estate object has been transferred according to the acceptance certificate |

|||||||

|

Interest accrued on the loan for April 24: (365: 100) x 2,000,000 x 21 |

|||||||

|

May 2005 |

|||||||

|

The expenses related to the state registration of the real estate object have been paid |

|||||||

|

After receiving documents on state registration, the real estate object is accepted for accounting as a fixed asset. |

|||||||

The initial cost of the fixed asset in the accounting records of OOO Krasnoderevshchik amounted to 2,035,116.43 rubles, since in accordance with clause 8 of PBU 6/01 it means the amount of the organization's actual costs for the acquisition of fixed assets. In our example, the initial cost was formed on the basis of the purchase price, state registration costs and interest on the loan accrued before the building was accepted for accounting in fixed assets.

For the purposes of tax accounting, interest on the loan is not included in the initial cost of the building; therefore, the initial cost of the building in the tax accounting records of OOO Krasnoderevshchik was 2,007,500 rubles.

End of the example.

In addition to interest on borrowed funds, expenses that are not included in the initial cost of fixed assets in tax accounting will be property insurance expenses, the sum differences, if the payment of fixed assets is made in rubles, and the price of the fixed assets sale and purchase agreement is tied to the currency equivalent ...

Do not forget that some expenses for the purpose of taxation of profits are accepted only within the limits of the norms, for example, business travel expenses (in terms of per diem).